I recently finished reading the Kindle version of Easy Money by Ben McKenzie and Jacob Silverman. Simultaneously, I also read Number Go Up from Zeke Faux, another blockchain-focused book that came out about two months after the publication of Easy Money. These would make the 10th and 11th blockchain-specific books I have reviewed. See the full list here.

Easy Money was not the worst blockchain-related book I have read, that award would go to Popping the Crypto Bubble. Easy Money had a lot of potential, in fact, several chapters had some pretty good prose and first-hand reporting.

But for some inexplicable reason – unlike most of the other blockchain books I have reviewed – the authors insert Ben McKenzie into the story for no apparent reason.

Previous books written by reporters might explain in first person how difficult it was to use a wallet or how difficult it was to explain mining to someone – but McKenzie finds a way to insert himself into every chapter even if he is irrelevant.1 And that takes a lot away from what could have been a powerful book.

For instance, Chapter 7 was probably the best written and interesting chapter of the book. The two authors flew down to El Salvador to investigate what kind of traction Bitcoin-based payments was having in the small Central American country. And as the authors describe the plight of one of the residents who is unlucky to live on land that was to be turned into an airport, they write:

Here was a famous Hollywood actor who wanted to film and interview him, to tell his story, yet no one in his own country could tell him when he would be kicked off his land or where he might go.

The reader is constantly reminded of how McKenzie was in several popular TV shows. In all but one other blockchain book I have reviewed few authors attempt to regularly remind people of who they are. The main exception is Fais Khan who wrote The Billionaire’s Folly, which was an insiders account of working at ConsenSys.

McKensie was not an insider. In his own words, he was stoned and out of work in late 2020, and came to the conclusion that he should pivot careers and write a book about crypto. Yet because he did not get really started until late 2021 – near the height of the recent bubble – it all comes across as Johnny-come-lately ambulance chasing self-serving plot filler to boost his PR so he can appear in the Netflix adaptation.2 It is both poor form and cringey.

Furthermore, the dual authors make a number of elementary mistakes. For instance on p. 36 they write: “In 2016, Tether was hacked. More than 100,000 Bitcoin (worth $71 million at the time) was stolen, and the company was in desperate straits.”

What they meant to write was that Bitfinex, the centralized exchange, was hacked. It was actually hacked twice in 2016, the second time 119,756 bitcoins were stolen.

Later, on p. 264 they write: “The other major player left standing was Tether. The stablecoin company, valued at $71 billion as of March 1, 2023, had miraculously survived while the industry around it bit the dust.”

This is not an accurate way of describing the company. The valuation of a bank – or in this case, a shadow bank – is usually determined by its book value of equity (BVE), not by how large its deposit base is. If we took its self-disclosed quarterly reports at face value, Tether LTD itself is worth several billion dollars. In contrast, the aggregate value of USDT spread across all chains, as of this writing, is around $86 billion. Academics such as Stephen Kelly, have publicly analyzed these claims, a future edition should include such remediations.

It is also worth pointing out that the book quickly glosses over any deep or detailed technical discussion and that is likely to help the reader move through the pages. Yet there is no glossary for further explanations and the Appendix consists of a single page copied from the SEC website regarding Ponzi schemes.

This is kind of strange considering even Diehl’s book at least paid some lip service towards the technical bits. To be fair though, unlike Diehl’s book, McKenzie and Silverman do not repeat the same refrain over and over again. But that should not be the bar. With the resources of a real publisher (Abrams), this should have been a top shelf book. But instead it is 1-star quality book and a hard pass.

As usual, all transcription errors are my own.

Chapter 1: Money and Lying

On page 1 the authors write:

These get-rich-quick speculative schemes were merely the latest iteration of casino capitalism. Political economist Susan Strange populated the term in the 1980s, but its roots stretch at least as far back as the 1930s.

This may seem pedantic but I am pretty certain the authors meant to write “popularized” and not “populated.”

On page 1 the authors write:

You may have noticed something about cryptocurrencies: They don’t do anything. Sure, you can trade them, betting that one will rise or fall, but they aren’t used for anything productive. Cryptos aren’t tied to anything of real value, unlike shares in a company or a commodities future. They’re computer code uncorrelated with any actual asset.

This requires nuance, something the book does not really have.

For instance, not every cryptocurrency is the same. Some, such as non-fungible tokens (NFTs), attempt to represent off-chain assets. A myriad of financial institutions and other large enterprises have attempted to tokenize a plethora of atoms, often in toy experiments that do not last a year or so. However there is an entire category of “real world assets” (RWA) that do in fact represent “real value.”3 We can argue about the particulars – should Paxos USD or PYUSD be allowed to exist? – but the authors cannot ignore the existence of tokenized assets identified by Centrifuge.

A better, a stronger argument they could have used involves “self-referential assets” — which many major cryptocurrencies are considered.

On page 1 they write:

In crypto, this comes from the fees charged by the exchanges, as well as the costs associated with validating the transactions. In Las Vegas, it’s called the rake, the amount the house takes from every pot. This means that, given enough time, the average gambler will lose. It’s how casinos keep the lights on.

I actually agree with one of their points here (regarding opportunity costs) but without evidence it is just another random opinion. A future edition could also cite the musings of Jack Bogle, the founder of Vanguard and creator of the index fund. He often characterized the excessive speculation that benefited financial intermediaries as the “croupier’s take.”

On page 2 they write:

When I first started paying attention to financial markets in the fall of 2020, I came to a similar conclusion, a troubling sense that graft and deceit had penetrated all aspects of the economy, operating with political and legal impunity. It made me want to scream in anger—and to make a wager of my own.

McKenzie is a couple of years older than me and it is hard to imagine how he thinks this helps his credibility.

How can you go your adult life – as someone with an economics degree – without paying attention to financial markets until three years ago? What were you doing in 2008 during the financial crisis? How did you miss the craziness of the ICO boom in 2017-2018 that John Oliver ridiculed?45

On p. 3 they write “crypto-currency” with a dash and then inexplicably use “cryptocurrency” without a dash later. And back and forth. The same happened with the word “block-chain.” Where was the proof reading?

On p. 3 they write:

A few thousand cryptos in 2020 grew to 20,000 two years later, and their purported value swelled in tandem, from some $300 billion in the summer of 2020 to $3 trillion by November 2021.

The authors use this 20,000 figure throughout the book. It comes from reference #4 for Chapter 1 which refers to CoinMarketCap (CMC) but in going to the website, there are currently 9,213 cryptocurrencies.6 For comparison, CoinGecko currently catalogues 10,812 coins. There probably have been significantly more than 10,000 coins or tokens created – many of which have died – but the author’s figure seems like an outlier.7

On p. 4 they write:

Narrative Economics was published in 2019, prior to both the current viral spread of cryptocurrency and the COVID-19 pandemic.

That seems like a weird tie-in especially since there was a mountain of PR for cryptocurrency projects during 2017-2018 in the U.S. For instance, between December 2017 to January 2018, you could turn on CNBC to hear some guest promoting a random coin they liked.8 More than likely, Narrative Economics was published before the viral spread of cryptocurrencies that the authors paid attention to.9

On p. 5 they write:

Two of its biggest drivers were financial deregulation and low interest rates—a decades-long, mostly bipartisan political effort to grow the financial sector combined with a policy intended to stimulate the economy in the wake of the first dot-com bubble.

This is partially true. A future edition should include a conversation around just how leveraged banks were, both foreign and domestic. This would have also been a good spot for the authors to discuss systemically important financial institutions (SIFIs) such as ‘too big to fail banks’ (TBTF) which even Diehl’s book paid lip service to once.

Why are SIFIs and TBTF banks worth discussing? Putting aside the ever present rent-seeking and moral hazard issues, the infrastructure that these organizations rely on often is highly centralized and dependent on a specific vendor thereby creating single points of trust and single points of failure. The book largely ignores legacy infrastructure operated by incumbents.

For example, a future edition could highlight one area the U.S. financial system (specific banks) could be improved: make banks public utilities.

On p. 7 they write:

Coordinating with other countries’ central banks, the US government offered $700 billion in bank bailouts and trillions in loan guarantees, managing to stem the worst of the contagion.

Probably worth telling the readers that this controversial bailout package, frequently referred to as TARP, failed to pass the initial House vote.

On p. 8 they write:

Public key encryption plays a vital role in modern life. For example, all https:// websites (nearly all the ones the average person uses) employ public key encryption. It does things like protect users’ credit card information from being stolen when making online purchases. Public key encryption has two useful properties: Anyone can verify the legitimacy of a transaction using publicly available information (the public key), but the people/parties conducting those transactions are able to keep their identities hidden (the private key).

While this is not a bad explanation, the authors should have used “public key cryptography” because that is usually how it is referred to. In fact, Bitcoin – like most cryptocurrencies – does not use any form of encryption.

On p. 9 they write:

This time-stamped, append-only ledger is the blockchain. In 1991, computer scientists Stuart Haber and W. Scott Stornetta, building off the work of cryptographer David Chaum, figured out a way to timestamp documents so they couldn’t be altered. Each “block” contains the cryptographic hash (a short, computable summary of all the data in it) of the prior block, linking the two and creating an irreversible record, a ledger composed of blocks of data that can be added to a chain (blockchain), but never subtracted from.

This is good. In fact, one of the problems with Diehl et al.’s book is that the trio completely whiffed on the Haber & Stornetta references in the original Bitcoin whitepaper. Worth pointing out that pages later, McKenzie and Silverman reuse this archaic blockchain as a strawman, hold your breath!

On p. 9 they write:

So far so good, but one issue remained: what’s known as the double spend problem. If you remove a centralized authority from the equation, how do you make sure people aren’t gaming the system by spending money that’s already been sent somewhere else? How do you secure the network against manipulation? “Satoshi” relied on what’s called a consensus algorithm.

Pedantically Bitcoin – and its progeny – use what is called Nakamoto consensus. For comparison, Diehl et al.‘s book briefly mentioned it in passing. A future version should incorporate that.

On p. 9 they write:

The network targets a new block every ten minutes or so, by dynamically adjusting the degree of difficulty required in the winning block; the more participants, the harder the process gets, and the more energy is required to guess the next block correctly. This is the proof of work behind Bitcoin: lots and lots of computers (“miners”) performing relatively simple mathematical calculations over and over again endlessly.

This is not really accurate:

(1) There are many proof-of-work based coins. Bitcoin (and some of its clones) have a readjustment period of 2,016 blocks, roughly two weeks. Adjustment does not take place every block as the authors write above.

(2) The resources consumed in a proof-of-work network like Bitcoin rises and falls directly proportional to the coin price. If number go up, then so too does the difficulty level and vice versa. They cite him later in Chapter 5 but it would be helpful to include analysis from Alex de Vries here as well.

What this means is that more energy is not necessarily required to guess the next block correctly. In fact, in its early years, Bitcoin could be solo mined on a normal laptop. Proof-of-work coins that never see much price appreciation can be solo mined by simple computers too.

There is another issue with their statement above: it does not explain the nuance, the difference between a Bitcoin mining pool (which is the block maker) and Bitcoin hashing farms (which generate the proofs-of-work). But more on that later.

On p. 9 they write:

After about an hour, participants in the network are convinced about history six blocks deep; they know that it is extremely unlikely anyone will rewrite that history.

This is not accurate. By social convention – not code – intermediaries such as coin exchanges will allow users to trade their newly deposited bitcoins between 3-6 block confirmations. Centralized exchanges like Coinbase, may require some coins such as Ethereum Classic to have hours of blocks built in order to protect against reorgs. But in both cases, this is social convention, not code.

On p. 9 they write:

As you may be able to tell, Satoshi’s vision is both immensely clever but also cumbersome, practically speaking. As more competitors enter, the hash rate increases and more energy is expended to agree upon a block of data that remains roughly the same size. This is what’s called a Red Queen’s race, a reference to Lewis Carroll’s Alice in Wonderland.

There are a couple of problems with this:

(1) During each transition from CPUs -> GPUs -> FPGAs -> ASICs, whoever was able to access to the newest generation of equipment first has had a material advantage from an energy usage perspective.10 For instance, four pages later the authors mention what Laszlo Hanyecz did – but fail to mention who he is and how he got his bitcoins. Note: Hanyecz was one of the first (if not the first) person to scale bitcoin mining with GPUs. His hashes per watt were likely lower than anyone else up until that point in 2010.

(2) I looked in the refences but do not see the authors point to any article that mention the Red Queens’ race. I myself referred to the Red Queen’s race multiple times in papers and articles between 2014-the present day.11 Would be interesting to see who it originated from (I believe I first saw it on a /r/bitcoin post in 2013); echoes of John Gilmore?

On p. 10 they write:

Ethereum also led to the introduction of NFTs, which are basically links to receipts for JPEGs stored on blockchains (shh, don’t tell that to anyone who owns one).

This is false. Both tokenization and non-fungible token projects existed several years before Ethereum turned on. For example:

It bears mentioning that even before Spells of Genesis was released on Counterparty (in 2015) several different colored coin projects attempted to tokenize off-chain assets. See my short presentation on this topic from last year.

In fact, if we are going to be really pedantic, perhaps the original idea behind “crypto art” (and NFTs) was inspired by Hal Finney in 1993?

On p. 10 they write:

The number of cryptos exploded around this time, rising tenfold in five years, from less than one hundred in 2013 to more than a thousand by 2017. There are now an estimated 20,000 cryptos, most of them small and insignificant, their ownership concentrated in the hands of a few “whales,” much like penny stocks.

There could be 20,000 coins and tokens, but as mentioned earlier, it is unclear where they arrived at that specific estimate since both CoinMarketCap and CoinGecko currently show around 10,000 each.

On p. 11 they write:

Remember, blockchain is at least thirty years old and barely used by businesses outside of the crypto industry. Since at least 2016, hundreds of enterprises have tried to incorporate it into their business models, only to later scrap it because it didn’t work any better than what they were already using. Ask yourself a simple question: If blockchain is so revolutionary, after thirty years, why is its primary use case gambling? Ironically enough, the more important technology is the one that predates it: public key encryption.

Nearly every sentences in this paragraph has an inaccuracy.

(1) Yes, the “blockchain is at least thirty years old” is really how McKenzie and Silverman are going to spin things. Even if we take their claim at face value the other problem is that not every blockchain is the same.

The Haber & Stornetta “chain” is limited in functionality. What is its throughput? How decentralized is it? Were the authors aware that this archaic chain places attestations once a week in The New York Times? That’s arguably not the best security property.

(2) Since there were hundreds of enterprises that have tried to incorporate a blockchain into their business, could the authors provide one example next time?

We are beginning to see a troubling pattern from the authors, lots of strawmen and few specifics.

They could be right, in fact, I even agree with part of their statement. But as Hitchens’s razor states: that which is asserted without evidence can be dismissed without evidence.

What kind of evidence could they have provided?

Above is a line chart illustrating Stack Overflow posts per quarter for three different ecosystems: Ethereum, Corda, and Hyperledger (Fabric). The latter two were primarily targeted at enterprises. R3, the major sponsor for Corda, recently announced layoffs impacting more than 20% of the company headcount. Does the decrease in Stack Overflow activity translate to less commercial activity? Maybe.

Since we are already doing their homework for them, here’s another example they could use in a future edition: in the process of writing this review Citi announced that it is offering a pilot service that turns customer deposits into digital tokens, for use use trade finance and cash management. Is this the type of blockchain project the authors think will ultimately be scrapped? Maybe it will, but next edition the authors could give specific examples.

(3) I actually kind of agree with their comment about how popular gambling-type of activities are within the various major chains.12 But strangely, the authors do not beef up their argument by providing any stats or charts.13 Stranger: while there are a handful of graphics in the book, there are zero blockchain-related charts, some of which could have helped strengthen their arguments. A quick googling found a bunch of crypto casino stats. Are the veracity of the numbers reliable? Sounds like something the authors could include next time.

On p. 11 they write:

The original story—that Bitcoin represents a response to the devastating failures of the traditional financial system—holds significant power because we all agree on its premise: Our current financial system sucks. But is the story of Bitcoin actually true? Does it do what it purports to do, create a peer-to-peer currency free of intermediaries? Was a trustless currency relying only on computer code even possible?

I have no affinity for Bitcoin but this is a strawman argument because it uses a retconned narrative from a number of Bitcoin maximalists. Satoshi herself explained that she started coding Bitcoin 18 months prior to the release of the whitepaper, which chronologically places its origin before the financial crisis of 2008-2009. I think the initial motivation was more aligned with securing (and funding) an online poker community, which the authors discuss later in the book.

On p. 11 they write:

Bitcoin may be the most popular digital currency, but it was not the first. In a 1982 paper, cryptographer David Chaum theorized the intellectual scaffolding of blockchain, upon which cryptocurrency would emerge some quarter of a century later.

They do not talk much about “blockchains” later in the book but it is worthy pointing out that in 2023 we typically use an article such as “a” or “the” in front the word blockchain. There was a period of time (mostly around 2016-2017) where consultant-types tried to push an articleless blockchain, but the grammar pendulum has shifted once more.

On p. 11 they write:

DigiCash was a legitimate project, without the conflicts of interest and other red flags surrounding many current crypto ventures. Unfortunately, it failed to take off and in the late 1990s the company declared bankruptcy before being sold.

Who died and made these authors king? By what standard was DigiCash “legitimate” or “illegitimate”? Maybe it was both or neither? But they provide no rubric, just dictum. According to legend, at one point Microsoft considered paying $75-$100 million to acquire DigiCash and integrate into Windows but Chaum wanted $2 per license sold. Also, in 2018 Chaum announced a new blockchain platform, Elixxir. Is this legitimate? It’s a public blockchain so obviously not?

On p. 11 they write about eGold:

It lasted until the mid-2000s before being shut down by the feds for violating money transmitter laws.

Throughout the book the authors describe activities from the FBI but this is the only time they lowercase feds.

On p. 13 they write:

PayPal and other payment services existed, but they were beholden to annoying gate-keepers like the law, national borders, banks, and terms of service agreements.

PayPal provided the MSB-centric model that a couple centralized pegged coin issuers have emulated.

While they make a lot of bluster over Tether LTD, this is the type of statement that impeaches the authors credibility: because neither seems to understand how certain fintechs have skirted U.S.-specific laws they cite in the book. This is nearly identical to Diehl et al. who approvingly namechecks PayPal a couple of times too, all while trying to dunk on “stablecoin” issuers. That is not consistent.

On p. 13 they write:

Bitcoin seemed like a solution, but at first no one outside the small Bit-coin network ascribed any worth to its tokens. In a story that has become memorialized in Bitcoin lore

Why is there a hyphen/dash in the 2nd Bitcoin but no hyphen/dash in the other two?

On p. 13 they write:

on March 22, 2010, 10,000 Bitcoins were used to pay for two pizzas, worth forty dollars

Without mentioning his name, or more importantly how he got 10,000 bitcoins, the authors are describing Laszlo Hanyecz. They do cite a relevant Forbes article but I think the readers would enjoy learning how disappointed Satoshi was when she first heard about GPU mining on the Bitcoin Talk forum.

On p. 13 they write:

Sure, the stuff was nearly worthless, but it was open to all, as early adopters could mine Bitcoin with their home computers without racking up enormous hardware and electricity costs.

This is accurate. But it conflicts with a number of their comments on page 9. A future edition should reconcile these conflicting statements.

On p. 13 they write:

Until it was shut down by US law enforcement in October 2013, the Silk Road was the most successful onboarding mechanism in Bitcoin’s history.

This might be true, but how did the authors determine or quantify “the most successful on boarding mechanism”? In looking at the citations and references, there are none. Maybe they are correct but a future edition probably should include a highly cited relevant paper: A Fistful of Bitcoins: Characterizing Payments Among Men with No Names by Meiklejohn et al.

On p. 13 they write:

If it didn’t work as a currency, perhaps a new story could be told. In the coming years, coiners started talking about Bitcoin as a potential store of value (despite its wild volatility) or as the basis of a new, parallel financial system, free of state control.

There are a couple of issues with this:

(1) They include the word “coiners” without providing any definition.14 “Coiners” appears nine times altogether in this book, yet not once do the authors explain what might mean. It is only by looking at the surrounding context that we can guess they have conjured up a word to describe “the outgroup.”

And here is where the story becomes even stranger. McKenize and Silverman arrived relatively late to the coin thunderdome. For some reason, they quickly fashioned themselves as “nocoiners” a term that readers of this blog understand was intended to be a slur. Yet these two market themselves with it as a badge of honor to The New York Times. Bananas.

Recall that the etymology of “nocoiner” arose in late 2017, coined by a trio of Bitcoin maximalists who used it as a slur. I was on the receiving end of coinbros lobbing the unaffectionate smear for years.15 The fact that McKenzie, Silverman and other prominent “anti-coiners” use it as a way to identify themselves – and their “in-group” – is baffling because it is the language of an intended oppressor. Do not take my word for it, read and listen to the presentations from those who concocted it.

If there is one take away from this book: do not willingly use the term “nocoiner” to describe yourself or use the term “coiner” to describe others. It is identity politics.

(2) The authors are somewhat correct: certain Bitcoin promoters, specifically a group that often refers to themselves as “Bitcoin maximalists” did in fact shift the narrative from disintermediated payments to a store-of-value.

Samuel Patterson went through everything Satoshi ever wrote. Unsurprisingly Satoshi discussed payments significantly more than a “store of value.”

I do not have a horse in this race, especially since I have no particular affinity for Bitcoin. But I do think the authors should have been more nuanced and specific about who was pushing specific narratives. 16

On p. 14 they write:

This was the beginning of DeFi (decentralized finance), in which tokens would be routed through complex, mostly automated protocols that added leverage and risk to the system—and a chance at huge rewards.

This is the introduction chapter but readers expecting more in-depth nuance will be disappointed because this is pretty much how they describe “DeFi.” It is not really accurate but let us wait a few more chapters to discuss why.

On p. 15 they write:

In late 2020, I came down with a serious case of FOMO. The entertainment business was on ice thanks to the pandemic, and I was bored and depressed. I saw a bunch of average Joes making money in the stock markets, so I dusted off my long-neglected degree in economics and started paying attention to them for the first time in my life.

Look, 2020 sucked for a lot of people. 17 But the statement above does not really help your credibility. Wouldn’t… you want to portray yourself as an expert?

On p. 19 they write:

Cryptocurrencies didn’t do any of these things well. You couldn’t buy stuff with them—the guys at my deli would look at me like I was nuts if I tried to pay for my bagel and coffee in Bitcoin. Advocates say this is a temporary problem; if more people would just buy Bitcoin, eventually it will become a currency you can actually use.

There are at least two issues with this:

(1) Readers have probably noticed the pattern wherein the authors conflate “cryptocurrencies” (broadly) with Bitcoin (specific). This is a strawman. Also, on social media the people who frequently push this particular narrative they are criticizing are often Lightning Network aficionados. Those are a subset of the Bitcoin-specific world.

(2) A lot of cryptocurrency / cryptoasset-related projects are not attempting to tackle payments or reinvent money. According to the book, the authors sample size for “industry events” I believe was just two? SXSW and Bitcoin Miami. That’s not exactly a robust sampling. Sure, you can conduct market research remotely but their unnuanced language has room for improvement.

On p. 19 they write:

The technology behind Bitcoin sucks. It doesn’t scale. Satoshi’s solution to the double spend problem was innovative, but also clunky. The more miners who entered the competition the more energy was used, but the blocks were the same. Bitcoin is able to handle only five to seven transactions a second; it can never go above that.

There are some good criticisms of Bitcoin out there but this rant is just bad, it sounds identical to Diehl et al.

(1) Bitcoin is just one implementation of a blockchain. The authors claimed earlier in this chapter that the “original” blockchain arose thirty years ago. But they never provide any metrics on how fast that one is/was. What is the throughput of the Haber & Stornetta “chain” versus Bitcoin 0.1 in 2009?

(2) The authors conflate the limitations of Bitcoin with every blockchain, and that is intellectually dishonest. There are several different Layer 1 (L1) chains – such as Avalanche – that clearly show the world is not limited to the throughput of Bitcoin. If anything, the omission of other chains shows a lack of market research and due diligence by the authors. Yea, sifting through claims is tiresome work, that’s my day job and often isn’t fun.

(3) Nakamoto consensus (proof-of-work) is not the only game in town when it comes to solving the “double-spend problem.” For just under a decade, different teams of researchers have successfully engineered and productionized proof-of-stake-based chains which overcome some of the limitations that proof-of-work-based chains had. The authors mention “proof of stake” a couple of times later on in passing but do a disservice to readers by effectively ignoring it.

(4) As mentioned a couple of times before: just because someone attempts to mine on a proof-of-work chain does not automatically mean extra resources are immediately required to mine additional blocks. For instance, if I started a new proof-of-work chain tomorrow, a fork of Bitcoin, then a variety of older USB-mining devices could easily generate hashes while consuming relatively little amounts of electricity. Energy (or resources in general) are typically only expended if the coin value goes up. Crab price action is often not attractive miners, especially those who own warehouse facilities filled with hashing equipment.

(5) In the references they cite one paper, On Scaling Decentralized Blockchains, which was presented in February 2016. A lot has happened in the past 7+ years. In fact, the paper primarily focuses on Bitcoin which again, is no the only blockchain in the world. Surely there are more relevant technical papers exploring the challenges and limitations of other chains?

On p. 19 they write:

Visa can process 24,000. To operate, Bitcoin uses an enormous amount of energy, the equivalent in 2021 of Argentina—the entire country. Visa and Mastercard use comparatively miniscule amounts of electricity to serve a customer base orders of magnitude greater. Bitcoin’s energy consumption is enormously wasteful, and poses a massive environmental problem for the supposedly cutting-edge technology (and really, for all of us).

This type of rant is similar to the kind you would find in Diehl et al. book, where there is a kernel of truth surrounded by apples-to-oranges comparisons.

I actually agree with their criticisms of (proof-of-work) energy consumption, and have written about it many times. But their other arguments above are incorrect in at least two ways:

(1) Visa and Mastercard are centralized entities operating centralized infrastructure. In the passage above, the authors endorse and defend rent-seeking incumbents. In the U.S., Visa and Mastercard operate a duopoly that is good only for their shareholders. For instance, following news that the Federal Reserve has proposed lowering the interchange (swipe) fee, the CEO of Mastercard slammed it.18li

The next edition of this book could include a conversation about the friction-filled payment infrastructure that allows private companies to extract rents on retail users in the U.S. For instance, five months ago a bi-partisan bill was introduced in both the House and Senate: “the Credit Card Competition Act, which would require large banks and other credit card issuers with over $100 billion in assets to offer at least two network choices to process and facilitate transactions, at least one of which must not be owned by Visa or Mastercard.”

(2) A better comparison would be between proof-of-work networks (like Bitcoin) and proof-of-stake networks such as Avalanche or Cosmos. The latter two do not require enormous amounts of energy to operate. By continually conflating Bitcoin with all blockchains as a whole, weakens their credibility.

On p. 19 they write:

So if cryptocurrencies weren’t currencies, then what were they? How do they actually work in the real world? Well, you put real money into them and hope to make real money off of them through no work of your own. Under American law, that’s an investment contract. More precisely, it’s a security.

The authors – neither of whom are lawyers – throw this hand grenade towards the end of Chapter 1 and do not even provide a citation in the reference section.19 Maybe they are right, but that which is asserted without evidence can be dismissed without evidence.

Also, anyone can create a (ERC-20) token and pair it with another token on a decentralized exchange, such as an automated market maker (AMM) like Uniswap.20 You can do it without raising external capital from anyone too. That’s precisely what Colin Platt did a few years ago.

On p. 20 they write:

There were now potentially 20,000 unregistered, unlicensed securities—more than all the publicly listed securities in the major US stock markets—for sale to the general public.

You would think they would provide specific examples of coins or tokens, and the facts-and-circumstances as to how they are unregistered and/or unlicensed securities. But they do not. Maybe they are right, but that which is asserted without evidence can be dismissed without evidence.

On p. 20 they write:

Worse, these unregistered, unlicensed securities were primarily traded on crypto exchanges, which often served multiple market functions and, therefore, had massive conflicts of interest.

The first part of the sentence can be correct, but they again do not provide any citation. I whole-heartily agree with the 2nd half of the sentence. I even gave a speech a few years ago, discussing these types of conflicts of interest.

On p. 20 they write:

And perhaps most disturbing, most of the volume in crypto ran through overseas exchanges. Rather than being registered in the United States, they were often run through shell corporations in the Caribbean, apparently to avoid falling under any particular regulatory jurisdiction.

This is a partially valid argument. Although they do not provide specific examples here, anecdotally it is likely that some centralized exchanges attempt to use regulatory arbitrage to avoid specific jurisdictions. But the next edition should provide a couple here (they do a little later).

One other quibble with this passage is that traditional financial institutions do precisely the same thing. They pioneered the playbook of lobbing for regulatory changes and structures in specific jurisdictions. For instance, the entire reinsurance industry is headquartered out of Bermuda.

On p. 21 they write:

When you buy a share of Apple, you are effectively a portion of the revenue stream, as well as the brand equity, market share, intellectual property—all of that. But cryptos don’t make stuff or do stuff. There are no goods or services produced. It’s air, pure securitized air.

This could have been a stronger argument if the authors used nuance. As mentioned earlier, there are “real world assets” (RWA) which tokenize off-chain wares. Instead of making a blanket statement, they should have honed in on the self-referential nature for most other cryptocurrencies. Also, the burden-of-proof is on them when they claim each and every cryptocurrency is a security.

On p. 21 they write about “Dave”:

We came up with a side bet of our own: I bet him dinner at the restaurant of his choosing that Bitcoin would be worth $10,000 a coin or less by the end of 2021. To my mind, it was easy money.

We never find out if Dave is a real person or not but that is unimportant. What is important is that prior to the publication of this book, McKenzie had an undisclosed financial interest: a large bet.21

As another book reviewer pointed out:

In a recent Guardian profile, the actor disclosed he lost as much as $250,000 trying to short the market. Allegedly he got the timing wrong. The article doesn’t share many details, so we can only speculate but this wager could undercut much of what McKenzie has been saying over the years. In other words, the self-declared paid liar is also a hypocrite.

Is McKenzie a liar? He definitely cherry picks but I’m not sure I would use liar to describe him yet. He is definitely inconsistent for not disclosing on social media that he was actively shorting cryptocurrencies.22 Later in the book he kind of defends this behavior by saying he does not invest in public companies so perhaps he justifies it all by claiming the coin projects are private? Again, we do not know exactly what the short(s) were so it is kind of just guesswork.

On p. 23 they write:

I decided to do something. I decided to get stoned.

When I was reading the book, I did an audible chuckle. It may be authentic, but why do the authors think this adds credibility to the story? Why should we take him seriously at this point? This is not the last time we hear about his marijuana usage.

On p. 24 they write:

I needed to do something other than drink to help me cope. Pot did the trick. While high, I stumbled upon an ingenious notion: I would write a book! It would be a book about crypto, fraud, gambling, and storytelling, as told by a storyteller who was himself gambling on the outcome. To my THC-inspired brain, it all made perfect sense. I had stumbled on something profoundly original! The next day, I woke up a bit groggy and realized the obvious: I don’t know how to write a book.

This is not even the silliest thing in the book. By now readers expecting a deep-dive into the nitty gritty should temper their hopes. Easy Money is basically a self-promotion book that takes a serious set of topics and superficially touches on each while giving the authors an excuse to play blockchain tourist. It is a disappointment to those of us who actually filled out whistleblower forms and sat down with prosecutors.

Chapter 2: What Could Possibly Go Wrong?

While every book has an origin story, for some reason the authors felt the backstory for this book was compelling enough to include in the actual book. While there are some amusing parts, most of it should have been left on the cutting board. It all comes across like Entourage wannabes. A good journalist needs a team but that team – and the journalist – do not have to become part of the story. Here they force themselves onto the reader and it is pages that could have otherwise been used to describe more of what happened in El Salvador. For instance, Zeke Faux – and other journalists – show you do not have to continuously insert yourself into the story line just because you have a hot take.

On p. 27 they write:

It was August 13, 2021, and I was perspiring more than I would have liked outside my local bar. It wasn’t the sweltering heat of that summer night making me nervous; it was the stupidity of what I was doing. You know how it goes, what had seemed sensible to propose via Twitter DM after some edibles seemed somewhat less so now. I had invited a journalist I’d never met to pitch him on writing a book I didn’t know how to write about events that hadn’t happened yet. What could possibly go wrong?

If you’re keeping score at home, this is the third time in as many pages that the author mentions he is consuming some form of marijuana. Sure it is just edibles, no big deal right? It is neither classy nor does it add credibility. If anything it reinforces stereotypes of the entertainment industry.

On p. 27 they write about McKenzie’s first interactions with Silverman:

I told him about my econ degree and my interest in fraud. I talked about my friend Dave, and about our little bet that a crypto crash was imminent, and that I felt I had a duty to warn others before it was too late. And then I told him I wanted to write a book about it all.

I genuinely appreciate his sincerity on wanting to warn others but the timing – and self-serving motivations – are ridiculous. Coin prices peak about two months after this meeting. The time to warn, and act, was arguably a couple years before hand. What were you doing in 2018-2019?23

On p. 26 they write:

I could summon my own superpowers as an econ dork and mid-level celebrity and spread the gospel of “crypto is bullshit.” I could call out the liars and thieves, write it all down, and put it out there for the people to see.

This is incredulous.

Pages ago the authors explained how McKenzie had ignored finance until the fall of 2020 and needed to dust off his economics degree. Was the Netflix version of this book going to show a montage of McKenzie pouring over the works of John Nash or Keynes’ General Theory and writing equations on a chalkboard that quickly turn him into an “econ dork?”

To his credit, McKenzie does look a bit like Russell Crowe, so that scene is a possibility.

More seriously: the fact that the authors literally state spread the gospel of “crypto is bullshit” undermines their credibility. How can you be objective while oozing so much self-righteousness? If you are going to self-deputize, shouldn’t you at least go through the motions of ascertaining the facts-and-circumstances like an actual prosecutor must?

On p. 28 they write:

I tried my best to be civil but firm toward my fellow celebrities, some of whom had made a lot more money and had much bigger bills than I did. I get it: Life’s a hustle. But let’s not be gross about it, or lack any discernment or critical thinking. There’s a bridge too far and crypto is past that.

We have no idea how much money the authors made from the book advance but we already saw McKenzie mention he had FOMO and was looking for work. The solution was that he hustled “crypto is bullshit” to anyone including reporters.

For example, last year in that same interview where he wore the “no-coiner” identity as a badge of honor he says:

Trolls still tell me to “have fun staying poor” and I have yet to react by saying “look at my bank account.” That is juvenile.24 And this is not the only time the authors humblebrag.

Chapter 3: Money Printer Go Brrr

This is could have been an interesting chapter, if the authors had spent time explaining to readers how the market structure of the coin world worked. For instance, they could have explained what pegged stablecoins were.25 Who were the major issuers. What market makers were. How centralized cryptocurrency exchanges typically fold together custody, trade execution, and clearing all in one. Instead, we are introduced to a cast of characters that do not seem fully integral to the story (e.g., they are not insiders).

On p. 31 they write:

For skeptics like Jacob and me, there was one corporation that reigned supreme when it came to our suspicions about the cryptocurrency industry: the “stablecoin” company Tether and its assorted entities such as the exchange Bitfinex.

Before diving into this, one thing that was a slight (grammatical) distraction was “Jacob and me” which is used 3 times altogether in the book, versus “Jacob and I” which is used 24 times. Again, not a big deal, just a little copyediting nitpick.

Anyways, much like “coiners,” the authors never define what “skeptics” are. Are they the same as “critics” – another vacuous word they frequently use? Strangely still, they commandeer a word that has been used to describe an assortment of people the past few years.

For instance, I have also been labeled a “realist,” “critic,” “skeptic,” “nocoiner” — oh and a “gadfly.” Terms I have rejected and the authors should have rejected too. For example, on June 30, 2015, CoinTelegraph described me as:

Several years later The Financial Times labeled me as “realist”:

Zeke Faux did not attempt to co-opt a term, his loss, right?

Sure we have “food critics” and “movie critics” but neither of these practitioners deny the existence – or potential utility – of the thing they are critiquing. Over the past 24 months the terms “critics” and “skeptics” seem to be used as a way to market newsletters, podcasts, and books. For instance, David Gerard and Molly White – people the authors namecheck in the Acknowledgements – have built careers out of the “nocoiner” identity – they are fully invested in it. And it shapes their coverage on this topic.

At a minimum can we all agree that fervently marketing oneself something contrarian sometimes devolves into tribalism?

On p. 31 they write:

Founded in 2014, Tether claims to be the first stablecoin ever created. (A stablecoin is a cryptocurrency pegged to an actual currency such as the US dollar.)

Three issues with this:

(1) The authors really should have used “USDT” to describe the token itself and Tether LTD to refer to the company that issues tether tokens. It gets confusing later on.

(2) In a future edition the authors should add a nuance around what a pegged and non-pegged stabilized coin are. For instance, while centrally issued stablecoins like USDT attempt to maintain a pegged value, others such as Rai drift a bit but are relatively stable (due to a controller system and CDPs). There is a small but growing category of assets that are stabilized relative to some external value, by definition they are not pegged-coins.

(3) Back in 2012-2014 during the heyday of “colored coin” projects, there were some toy experiments that attempted to tokenize (link) USD to a discrete amount of satoshi.26 On Counterparty, there was an actual product – Digital Tangible Gold – that tokenized gold held in custody by Morgan Stanley. For history buffs, Pierre Rochard, one of the maximalists who coined the term “nocoiner,” contacted Morgan Stanley directly who then closed the custody account.

On p. 31 they write:

And if you were making huge gains or moving money between jurisdictions, Tether helped avoid the imposition of regulated banks with their pesky reporting requirements.

As previously mentioned it is unclear if the authors are referring to tether (USDT) or Tether (the company). If it is the latter, according to the company they have implemented some KYC / AML requirements. It would be interesting to know how rigorous those were. Also a future edition could explain the difference between banked and bankless exchanges and how USDT acts as a type of shadow bank for latter as well.

On p. 31 they write:

On October 19, 2021, we published “Untethered” in Slate.

At this point I had already interacted with Silverman via Twitter, sending him mining-related links. They reached out to conduct an interview for the article above, here’s what they penned:

Those were indeed my words, but it does feel a bit like cherry picking for sensationalism. I pointed this out on Twitter too. I also provided a lot of other color that they did not use. Obviously it is their column but I don’t think it was a fair representation of the totality of my conversation.

On p. 31 they write:

We hadn’t cracked the company’s mysteries, but the piece, which built on past investigations by Bloomberg, the Financial Times, and writers like Cas Piancey, Bennett Tomlin, and Patrick McKenzie, was consistent with our proselytizing mission. We were here to ring alarm bells and make sure the lay public could hear them.

This is a little revisionist history and misses some important people such as J.P. Koning. Since the authors have done such a good job at self-promotion, let me give it a shot.

Back in 2017 I introduced “Bob” to reporters including Bloomberg and later the NYT. Bob later went on to speak with the CFTC (this is not to take credit for what became the CFTC lawsuit).27 The most popular post I wrote that year was Eight Things Cryptocurrency Enthusiasts Probably Won’t Tell You which identifies Bitfinex and Tether as the number one glossed over aspect of the ecosystem.

In December 2017, I was quoted in Bloomberg:

“Is there anything backing this?” said Tim Swanson, who does risk analysis for blockchain and cryptocurrency startups. Swanson, also director of research at Post Oaks Labs, said he fears problems with tether could hobble exchanges that trade it. “If these aren’t backed 1-to-1, then what is the contagion risk if one of these exchanges goes down?”

And I was far from the only person curious about Tether in 2017.

While a future edition does not need to cite me, they should at least expand the list of people who openly discussed the role Tether (USDT) played in the coin world beyond the three they mention above, starting with Koning. For bonafides, the oft-cited Money Flower Diagram from the Bank for International Settlements (BIS) specifically mentions Koning’s Fedcoin idea.

On p. 32 they write:

The second red flag for Tether was its size relative to its workforce. Twelve employees (maybe even fewer) are running a business that deals in tens of billions of dollars? Forget the absurdity and ask yourself why. If you were running a legitimate, huge business dealing in big-dollar transactions, wouldn’t you want, and need, more than a dozen people helping you run it?

This would not be a top three red flag for me. The authors are saying: managing that size of money should involve more than a dozen. But does it necessarily? What is the average size of a money manager or hedge fund? According to IBISWorld the average U.S. hedge fund has 10.7 employees.

Ah but Tether LTD is not a hedge fund, or at least should not be, right?

And this is how we arrive at what the top red flag should be and one that Rohan Grey forcefully argues thusly: a case against centrally issued pegged-USD issuers – such as Tether – should be rooted in first principles. Tether LTD intentionally operate as shadow banks and/or a shadow payment provider. Everything else – while perhaps important – is a knock-on of that.

This is why we should put aside conspiracy theories – if Tether LTD owns Evergrande commercial paper – because a first principles analysis would conclude that U.S. regulators should use the tools available to them to bring Tether LTD into compliance irrespective of what Tether LTD has as reserves. If that means Tether LTD is required to form a state or national bank, then that is one (unlikely) outcome.28

However a persistent problem in this book is that the authors spend more time discussing possible hypotheticals rather than what we can easily confirm. The CFTC and NYAG have already provided evidence that backs up the concerns academics such as Rohan Grey previously articulated. Strangely, while the authors namecheck Grey in the Acknowledgements, they do not cite any of his work. A future edition should also include a discussion on shadow banks that explores any similarities between PayPal and Tether LTD.

On p. 34 they write:

They hid that fact from the general public, only to have it revealed with the release of the Paradise Papers, a trove of confidential financial documents that were leaked to journalists in 2017.

It was Nathaniel Popper, then a reporter at The New York Times, who first connected overlapping ownership between Bitfinex and Tether LTD via the Paradise Papers. The reason I highlight this is because Jacob Silverman dunked on Popper on Twitter during the writing of the book. Then later deleted the tweets.29 Despite his stellar reporting on the topic, Popper is notably absent in the book including the reference section.

On p. 36 they write:

To pick one more bizarre factoid from an extensive list, their primary bank mentioned above, Deltec, was headquartered in the Bahamas and run by Jean Chalopin, the guy who co-created the Inspector Gadget cartoon series. If it wasn’t a giant scam, it was at least marvelously entertaining.

In November 2018, I got heckled on stage by a Tether promoter, Josh Olszewicz. Here is part of what he yelled at me from the audience:

It wasn’t even the first time I was harassed at a fintech event (John Carvalho stalked me at Consensus 2017).

Putting aside the colorful personalities this space attracts, I still do not understand the Inspector Gadget fascination. 30

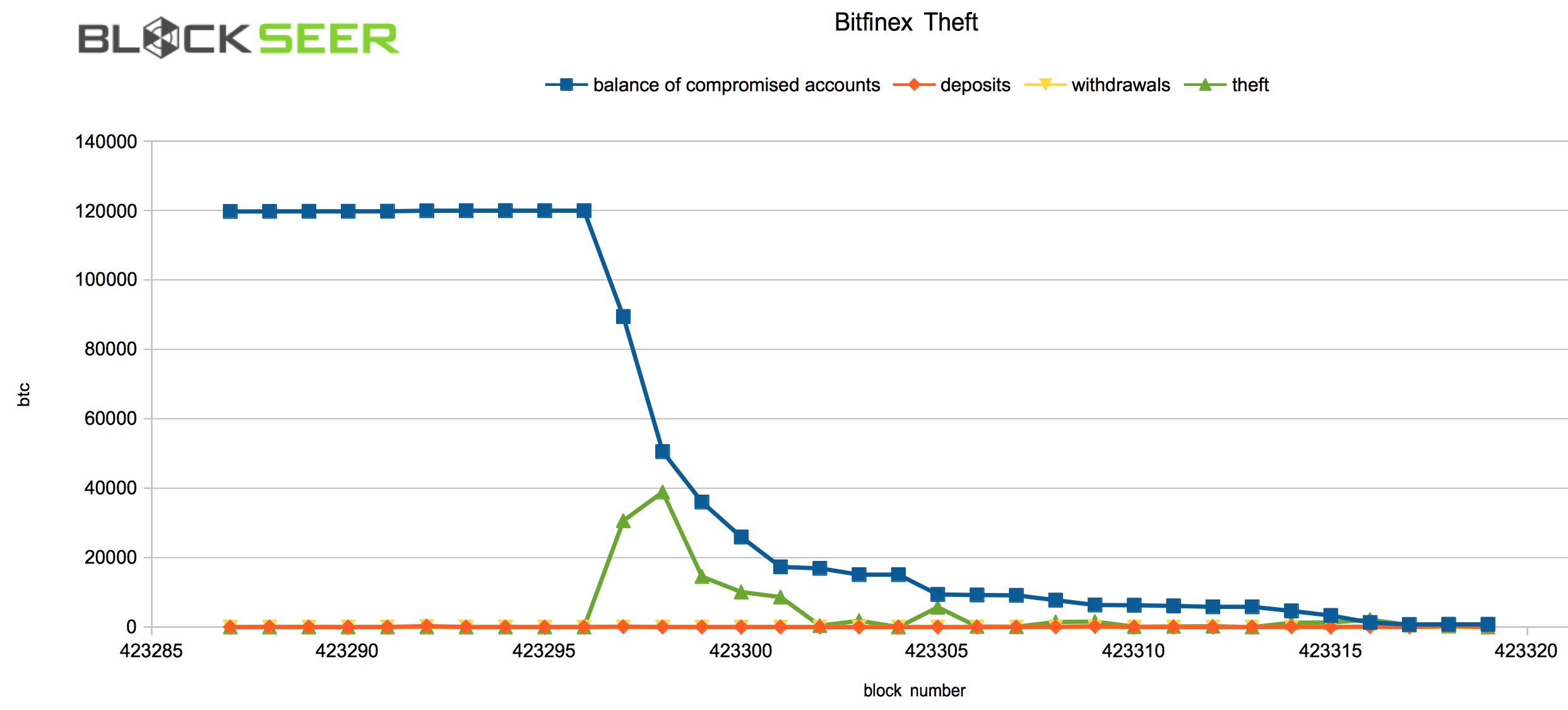

On p. 36 they write:

In 2016, Tether was hacked. More than 100,000 Bitcoin (worth $71 million at the time) was stolen, and the company was in desperate straits.

As mentioned at the beginning of this review, this is incorrect. In August 2016, Bitfinex – the cryptocurrency exchange – was hacked and 119,756 bitcoins were stolen.

On p. 36 they cite a paper: Is Bitcoin Really Un-Tethered? by John Griffin and Amin Shams.

But then they wrote something kind of strange in parenthesis:

(Griffin’s blockchain forensics firm has also had contracts with a number of government agencies, indicating that he is advising on crypto investigations.)

Why speculate on what Griffin’s analytics firm may or may not be working on? Surely you could just contact them and ask? It is called Integra FEC.

On p. 36 they write:

Wash trading is the practice of buying and selling an asset back and forth among accounts you control in order to give the appearance of demand for that asset. Crypto is perfectly suited for this sort of manipulation.

To strengthen their argument they could have cited the CFTC settlement with Coinbase before its direct listing two years ago. Its senior engineer, Charlie Lee (who was the creator of Litecoin), was accused of wash trading on the GDAX platform.

On p. 38 they write:

While Tether might have been a last resort for people in need, it carried with it massive costs. Trading in crypto often means incurring heavy fees, and it’s difficult to cash out into real dollars via legal means, pushing people into relationships with unsavory characters who are, at a minimum, not motivated by charity.

How much are those heavy fees?

On p. 38 they write:

In addition, the use of Tether can be seen to further undermine already weak currencies, contributing further to their downfall.

I should be in their small-tent camp, right?

For instance, on November 2, 2018 in an op-ed for FinTech Policy, I labeled Tether (USDT) a systemically important utility for the crypotcurrency world. On March 3, 2021 I gave a presentation to the Fed’s DLT monthly meeting and ended by saying they should look into pegged-coin issuers like Tether LTD.

The authors could improve their arguments by providing specific details because they miss the entire discussion from first principles: centralized pegged-coin issuers acting as shadow banks.

For instance, in their one sentence claim above, how does using Tether (USDT) undermine weak currencies? Which currencies? Is there a nation-state that has adopted USDT? Who knows, the authors do not provide those details.

On p. 38 they write:

I couldn’t believe what I was hearing. On the other end of the line was a male voice I only knew as belonging to a pseudonymous Twitter handle calling himself Bitfinex’ed. He had been on the Tether case for years. Bitfinex’ed had long suspected the company was a fraud, and had paid the price for his obsession with harassment, ridicule, and, he claimed, an attempt to buy him off. On crypto Twitter, some hailed him as a conspiratorial crank while many others, including people in the industry and in mainstream media, had learned to trust his tips.

There are a couple of issues with this:

(1) Bitfinex’ed real name has been in the public for a few years, all you have to do is a bit of googling. It is Spencer Macdonald. How did I find this out?31 Back when I wrote long newsletters he was on my private mailing list and sent me the link to a Steemit article of a guy who “doxxed” him because Macdonald had re-used the same catchphrases “Boom. Done.” under an alias Voogru on reddit.

While the Steemit article mentions his name it is not fully accurate either. At the time, some of Tether LTD’s supporters were pretty bananas online (just look at how one heckled me IRL). For instance, Stephen Palley helped provide legal assistance when there were issues with Macdonald’s Twitter account being locked. CoinDesk ran an article about it.

The other area where that Steemit article is incorrect relates to Jeff Bandman and the CFTC. The entire bottom quarter of that post is a guilt-by-association. Maybe Bandman is bff’s with both Palley and Macdonald, maybe they play golf and tennis together each weekend. There was no evidence presented that they are all in cahoots. Either way, ~2.5 years later we learned the results from the CFTCs subpoenas: that at certain periods of time Tether LTD did not have reserves they claimed backing the USDT (among other things) and some of the executives lied both publicly and privately about that.

(2) What tips did the authors assess were right and wrong?

For instance, Macdonald and I made a bet almost two years ago. And I won. But he blocked me months ago and never sent me the scotch. Sad days.

Maybe Macdonald and the group of “Tether Truthers” (USDTQ) are correct, maybe Tether LTD still operates as a fraud today.32 If readers are expecting some kind of “smoking gun” from reading this book, they will be disappointed. Bitfinexed – and some others in his circle – act as if they have some kind of secret knowledge.

When you ask them to simply reveal it, they post to more twitter threads.33 When you ask them to file whistleblower forms, they do not.

For comparison, Zeke Faux met with Bitfinex’ed in-person and wrote the following on p. 77:

When I asked for his sources or evidence, Andrew didn’t have anything new to provide. That was where I was supposed to come in.

[Andrew is one of the nom de plume of MacDonald/Bitfinex’ed]

Nothing secret was revealed in this book which is a disappointment. For instance, Bitfinex is an investor in Blockstream and USDT was directly issued onto Liquid (a quasi permissioned chain operated by Blockstream).34 At least two of the executives, Adam Back and Samson Mow, regularly promote and defend both Tether and the current president of El Salvador. Did they really own a Gulfstream IV?35 Nary a mention of Blockstream in the book.

In my view there are two distinct phases of Tether-related criticism with the divergence before and after the settlements with the CFTC and NYAG:

Phase 1 – concluded in early 2021 where the CFTC and NYAG both proved that Tether LTD did not operate in full reserve and some of the executives lied

Phase 2 – 2021 to the present day, post-settlement Tether Truthers claim that Tether LTD still does not operate and back USDT in full (reserve).

I stand by my previous criticism of Tether LTD and Bitfinex from phase 1.

But the onus is on the Tether Truthers to provide evidence that Tether LTD is still operating as a fraud and/or scam. Maybe it is, but what we typically see on Twitter is innuendo. Are both the CFTC and NYAG missing something? I posted this question on Twitter the other day and was called low IQ. Great feedback, I’ve been called much worse!36

On p. 38 the authors write:

Bitfinex’ed, whose real identity remained a mystery to us

The first search result for googling “Bitfinexed identity” is to a five year old article that links to the Steemit article.

On p. 38 they write:

Despite attempts to dox him—and a temporary Twitter suspension—Bitfinex’ed managed to maintain his anonymity, while developing a growing audience online. His fixation on Tether has bordered on obsession.

Again, the first search result for googling “Bitfinexed identity” is to a five year old article that links to the Steemit article.

On p. 38 they write:

Crypto partisans dismissed him as being salty because he hadn’t gotten in early enough on Bitcoin. But more sober observers pointed out the fact that Bitfinex’ed had been right about many of his claims. Some just took longer to prove.

That could be true, but which specific claims was he right about? Off the top of my head, based on direct communications with him I believe he had two correct predictions:

(1) That USDT was at times not fully backed

(2) That Tether LTD and Bitfinex shared common ownership

And while not a prediction per se, at the time he also transcribed ad hoc interviews that executives, such as Phil Potter, publicly gave on issues surrounding banking access. Speaking of which, did the authors try to reach out to Potter? Because Faux gets a direct quote from Potter regarding the origins of Tether.37

On p. 38 they write:

And few people had done more to educate journalists, critics, and the larger public about the perfidy lurking underneath crypto’s wildly anarchic market activity.

How do McKenzie and Silverman know this? They did not start covering this space until just under two years ago. Did they sit down and tabulate who educated who?

On p. 38 they write:

Bitfinex’ed was the angry, roiling conscience of crypto Twitter, always ready to swoop into a conversation and expose the dark underbelly of the latest industry spin. To some that made him a threat.

Macdonald did not and does not have a monopoly on “exposing the dark underbelly.” For example, did the authors contact ZachXBT?

On p. 42 they write:

SPACs, or Special Purpose Acquisition Companies, were often nothing more than blank checks issued to aggressively self-promoting “investment gurus” who would pocket a huge fee in exchange for gambling with their investors’ money.

This is a good point.38

On p. 43 they write:

My portfolio of short bets was, to put it generously, in shambles. I started with $250,000 that summer, by November it was down to $38,931. While I had bet on other frauds, the main culprit was simple: I had wagered too much on crypto’s collapse too soon, and blinded by my certainty, I nearly lost it all. By the time I got out of my initial crypto positions, they were almost worthless. What had been a lot of money was now very little. To be blunt, it was an unmitigated disaster—the kind of thing that provokes an uncomfortable conversation with your spouse.

We learn a few more details scattered around the book. As mentioned earlier, he began this bet with a friend “Dave” but we are never told its composition. Did McKenzie attempt to short some futures contracts on CME? Also, at least he is honest about his “blinded by my certainty” — something that other book authors on this topic failed to reflect on (such as Michael Casey’s dubiously title: “The Age of Cryptocurrency” reviewed 7 years ago).

On p. 43 they write:

The financial press was practically in lockstep about the inevitable crypto-fied future of money. Politicians, their pockets brimming with donations from industry moguls like Sam Bankman-Fried of FTX, were preaching the Bitcoin gospel. They were also openly contemplating passing industry-written legislation to further legalize these rigged casinos.

This is another decent point. But later in the book, we are only provided a cursory set of examples which we will discuss later. Also, the main quibble readers should have with the 2nd sentence is that the authors conflate “Bitcoin” with “crypto” as a whole. SBF may have been many things, but he did not frequently give off maximalist vibes.

On p. 44 they write:

Since in my analysis crypto was only speculation, it would fall like a rock once the Fed raised rates. Unfortunately for me, I had been just a bit early in making that call.

As my friend Colin Platt – the richest person in the world – is wont to point out: being early is effectively the same thing as being wrong. He says this from experience (with DPactum)!

On p. 45 they write:

In the interests of objectivity—and not wishing to be a participant in the kind of market manipulation I’ve denounced—I’ve never written about the companies I’ve shorted. You don’t have to trust me on this; you can look at my work. I’ve never written about publicly traded companies, only privately held ones. I’ve never traded or owned any cryptocurrency. My bet on crypto was simpler, and bigger than any one company: I thought the whole thing—all $3 trillion of it—was a speculative bubble. That part was obvious to me. The thing I couldn’t prove yet was that it was a bubble predicated on fraud. Hence, my journey with Jacob.

As mentioned above on p. 21, another book reviewer labeled McKenzie a liar and a hypocrite for failing to disclose this bet. The disclaimer above doesn’t really absolve the lack of disclosure: he has a vested interest in seeing the coin world go kaput.

I empathize with McKenzie.

For example, during the rapid rise in coin prices in December 2017, I was quoted as a “skeptic” in The Wall Street Journal:

That was published just days before the Bitcoin price peaked. Yet as certain as I was, I still did not short the market primarily because of counterparty risk and timing. Do I get book deal with Abrams now?

One last comparison, in Number Go Up, Zeke Faux describes a multi-million dollar offer he received to provide some purported Tether-related documents to a short seller. He turned it down, reasoning:

“This book is going to be called Jay Is Wrong and Zeke Is Right: The Cryptocurrency Story,” I said. “As a writer, you don’t want to be compromising in any way, you know? You don’t want to have ulterior motives.”

Unlike Faux it’s pretty clear from the book – and tweets – that at least one author has an ulterior motive: McKenzie discusses his short selling bet a number of times.

Overall this chapter made several interesting observations (such as the abuse around SPACs) but it seems like portions of the chapter could have been removed (e.g., most of the commentary around Bitfinex’ed) and instead re-used to discuss more of the celebrities like Matt Damon who acted as a public spokesperson for crypto-related companies.

Chapter 4: Community

A portion of this chapter hones in on McKenzie’s desire to have an entourage, a crew. It comes across as sappy and cringey and not something a made-it actor or journalist would strive for.39 As mentioned at the top, in no other book on this topic (that I have reviewed) have the writers explicitly stated as much because it should not be necessary.

In fact, because of the never ending drama-per-second the coin world generates, copy-paste Twitter accounts like Web3isGoingGreat, are able to rely on continuous streams of mainstream reportage on this topic to copy-paste from. McKenzie and Silverman did not need a crew of podcasters, and the next edition of the book probably should reclaim these pages to discuss what is going on in say, El Salvador, which was interesting and novel.

On p. 49 they write:

Bitcoin maximalists proudly boast that “Bitcoin has no marketing department,” which is technically true, but in practice dead wrong. Multibillion-dollar corporations—at least on paper—spent real dough to convince people to buy crypto. Sometimes the appeals were explicitly about Bitcoin, leveraging the brand awareness of the best-known cryptocurrency.

While we are never provided a full definition of what “Bitcoin maximalism” or who specifically makes that claim, I have heard this claim before from Andreas Antonopolous during his halcyon days. And while the authors do list off a series of A-list celebrities and entertainers who shilled something coin-related, it would be great to see specific tweets of endorsements in a second edition.

On p. 50 they write:

It also felt appropriate that I found myself on the opposite side of the proverbial line of scrimmage from the Hollywood consensus, but seemingly without a squad of my own. To counter the feelings of isolation and depression in my quest for truth in crypto, I needed to finally meet some fellow skeptics in the flesh. I needed a team of my own. Crypto-skeptic nerds assemble!

You do not need a squad to be a (investigative) reporter in this space.

Sure, building up a reliable rolodex of contacts is part-and-parcel to what reporters covering a beat will accrue over time, but journalists are encouraged not to get too close to sources otherwise you compromise your objectivity.

For instance:

I have not had a chance to read Michael Lewis’s new book, but according to his 60 Minutes interview, Lewis still has some affinity for SBF.

On p. 51 they write:

HODL is hold on for dear life, meaning that you should cling to your crypto no matter the price.

I have pointed this out in several other book reviews but the etymology, the genesis of “hodl” did not originate as an acronym or portmanteau. It came from a drunk poster on the BitcoinTalk forum, there are many articles discussing this. However, what the authors describe “hodl” to mean is correct.

On p. 53 they write:

Surveying the landscape in 2022, it was hard not to notice the myriad similarities between crypto and pyramid schemes. Both depended on recruiting new believers rather than buying anything with an actual use case.

This is an adequate comparison (for many cryptocurrencies).

I currently think a decent description of Bitcoin itself is how J.P. Koning categorizes it as a game akin to a decentralized chain letter:

On p. 54 they write:

Bitcoin ownership is highly concentrated in an extremely small number of whales who wield enormous power in the highly illiquid market. According to an October 2021 study conducted by finance professors Antoinette Schoar at the MIT Sloan School of Management and Igor Makarov at the London School of Economics, .01 percent of Bitcoin holders control 27 percent of all the coins in circulation. Some community.

Anecdotally this is probably true, for Bitcoin at least. Is it the case that every cryptocurrency / asset is the same way?

On p. 54 they write:

The eccentric community of crypto skeptics also fits in that category, and I was proud to call myself a member.

We are over 50 pages into the book and the authors still have not provided a succinct definition of what a “Coiner” or Skeptic” or “Maximalist” or “Critic” are. What are these tribes? What are their etymology?

On p. 56 they write:

many coiners really do feel that they are part of a like-minded community

What are coiners?

On p. 56 they write:

Practically everyone I spoke to at crypto conferences and other public events both admitted to being scammed and accepted it as if it was almost obligatory, a character-building exercise and bonding agent. Few spoke about stopping scammers in general.

This is a really good point, and I completely agree with the authors.

McKenzie’s experience reminded me of the meme from The Ballad of Buster Scruggs:

It is still unclear why this rugging behavior is perceived as a rite of passage and normalized.

On p. 57 they write:

In the case of the 20,000 cryptos other than Bitcoin, it should be simple to categorize them under the law. Most were securities made by real companies with real employees.

Maybe that is true, did the authors cite a securities lawyer? Did they quote a U.S. judge?

This is the same problem that occurred in Diehl et al., book: lots of opinions but few references. I am a certain there are U.S.-trained lawyers who share the same views as the authors, why not quote them here? For instance, later in the book they chat with John Reed Stark; this would have been a good spot to introduce him.

On p. 57 they write in parenthesis:

Ethereum also used proof of work to mine its cryptocurrency, until turning to proof of stake in September 2022. In proof of stake, owners of the crypto validate the blocks, making the system far less energy intensive, but incentivizing even more centralized ownership.

Two issues with this:

(1) As mentioned earlier, while there is some discussion of proof-of-work-based mining (the authors visit a hashing farm in Texas), the conversation or discussion around alternatives — such as proof-of-stake — are few and far between.

(2) Did the authors provide evidence that proof-of-stake systems are even more centralized? Maybe they are, but no references were provided. What can be asserted without evidence can also be dismissed without evidence.

This also reminds me of Matthew Green’s evergreen tweet:

On p. 57 they write:

What started as simple speculation and peer-to-peer exchange became a web of derivatives markets, DeFi protocols (a set of rules governing a particular asset, often using so-called smart contracts, run on blockchains), lending pools, and other newfangled features of digital finance.

What are derivatives markets? What are DeFi protocols? What are lending pools?

On p. 58 they write:

Under this arrangement, buying Dogecoin on a crypto exchange like Binance was indeed an act of trustlessness, but only in the sense that it was hard to trust any offshore crypto entity.

This is a strawman. Why? Because Binance is a centralized exchange, it is a trusted-third party. No one is arguing that Binance or other centralized exchanges are… decentralized.

On p. 58 they write:

“Not your keys, not your coins,” was the mantra thrown around by die-hard crypto fanatics, meaning you should keep your crypto in a “cold wallet” that didn’t touch an exchange—or even the internet. But that kind of advice did not reflect the reality of the markets. It defeated the primary purpose of money, which is to make buying and selling stuff convenient and fluid.

I mostly agree with their observation and have written about all of the “friction” that coin-related intermediaries often add. But there does need to be a nuance with private keys because various controllers in traditional finance also have key (recovery) management involving hardware wallets, cold wallets, an so forth. Traditional finance has incorporated the modern iteration; see Thales on slide 9.

On p. 58 they write:

Unfortunately, creating money that’s trustless is impossible in practice, for it goes against the very nature of money itself. Adopting it as a mission can only lead to disappointment.

There are a couple issues with this:

(1) This seems to be an a priori argument. By definition, a priori arguments are the opposite of empirical arguments. So no matter what evidence someone could provide, it seems like the authors have made up their mind.

(2) Not every cryptocurrency or cryptoasset project is attempting to reinvent money.

On p. 59 they write:

In the United States, the nation with the largest economy in the world—as well as the issuer of the world’s reserve currency since 1944, the US dollar—we often take this consensus for granted. Everyone wants dollars, especially in times of crisis.

What is a reserve currency?

There are several reasons why the U.S. is the issuer of the world’s reserve currency. While the authors do mention a couple of authors, experts such as professor Michael Pettis and Brad Setser, attribute the U.S. dollars current reserve status due largely to the (im)balance of trade. The U.S. runs large trade deficits. And mercantilist economies such as China are either unwilling or unable to shift to running large trade deficits. Until something dramatically changes, the U.S. dollar will continue to remain the key reserve currency.

On p. 59 they write:

In that sense, the stated goal of cryptocurrency—to create a trustless form of money—is literal nonsense. You cannot create a trustless form of money because money is trust, forged through social consensus. As Jacob Goldstein writes in Money: The True Story of a Made-Up Thing, “The thing that makes money money is trust.” Saying you want to create trustless money is like saying you want to create a governmentless government or a religionless religion. I think the words you are searching for are anarchy and cult. The bartender should cut you off and make sure you get a ride home.

This is a strawman. Not every cryptocurrency or cryptoasset project is attempting to become “money.”

There are a number of coin promoters who regularly echo comments similar to Zero Hedge, that the U.S. dollar is doomed. Maybe it is, and maybe that is who the authors are thinking about, but we are not provided specific names of people who make the argument that a specific cryptocurrency is going to become a “reserve currency” let alone “money.”

On p. 60 they write: