Last year a friend sent me a copy of “Popping the Crypto Bubble.” I read the first few chapters before life got in the way and recently re-discovered it while unpacking and finally finished reading it.

This is a book I should have liked, after all, for years I have been labeled as a “crypto critic” or as a “no-coiner” terms that I thought were inaccurate or even slurs.1

In fact, for several years I wrote a private newsletter that was circulated among many now prominent anti-coiners. So if there is someone who should have wanted this book to be great, it is me. But it is not. It is actually a bad book.

I have formally written eight book reviews for “blockchain-related” books and I would rank this at the bottom. Part of it is the poor editing which has been highlighted by at least one other commentor. For example, the bibliography section is out of sync and is missing an entire chapter.2

But the bulk of the feedback is that the chapters are sloppily assembled with a hodgepodge of polemical rants. The substance comes across as a broken record of anger and angst.

In addition, the book is typically associated with a singular author, Stephen Diehl, but there is no unified voice throughout the book. Instead, many passages read as though they were carved out in a Google Doc by one of his two co-authors (co-workers actually).

As a result, a reader will find themselves ploughing through some semi-technical explanation of a financial product only to hear Diehl’s voice wedge itself at the very end, claiming it was all a scam or fraud or both. It is tiring because it happens so often.

Before diving into the book, worth mentioning that unlike virtually every other book on this topic, the authors do not provide their background or motivation in any section, although the tone is clear as early as page 1.

For readers unfamiliar, the three co-authors worked together at a US-based company called Adjoint, a tech firm I was introduced to in July 2017 when it was involved in doing something with smart contracts which Diehl has removed from his LinkedIn bio.3 Adjoint announced “Uplink” a couple months after that call.

Obviously it is okay for people to change their minds. Some people do not like the local sports team when they move to a different state or province. Some people fall out of love for avocado toast. Some people like working on “the next generation of distributed ledgers.”

So what changed Diehl’s mind between 2017 and 2022? According to Diehl’s presentation in December 2017 he was all-in on blockchains; then in a group presentation in April 2018, the co-founders were still on-board the blockchain train. It is not clear from the book (perhaps he has said somewhere else?) but he leaves no doubt that he is not a fan of cryptocurrencies or blockchains or smart contracts or web3.

Below is a breakdown of issues with each chapter. Note: all transcription errors are my own.

Chapter 1: Introduction

In the second paragraph on p.1 the authors write:

The overarching idea of cryptocurrency is based on a complex set of myth-making built on a simple unifying aim: to reinvent money from first principles independent of current power structures.

Where is the citation or source to back up that claim? Perhaps some Bitcoin maximalists hold that core view as their raison d’être to “reinvent money” but if we were to say, use the title of popular conference panels, it isn’t actually as common in 2023 or probably even June 2022 when the book was published. However the onus is on Diehl et al., to provide evidence for the claim and it is not presented.

Grammar: in the same paragraph there is a glaring grammatical issue on the first page of the book. It was also highlighted by one Amazon review:

On the same page the authors write:

While a software is political, some software is more political than other.

Not only is there a missing “s” at the end, but it is not really clear what this means even with the following sentences related to the 2007-2009 Global Financial Crisis. Is Solitaire political? Is Excel political?

The concluding sentence of that same paragraph concludes:

The divisions over cryptocurrency are based on a philosophical question: Do you worry more about the abuse of centralized power, or about anarchy?

Again, no citation or anything to surmise why this is the philosophical question.

For instance, there seems to be a range of motivations for why a regulated financial institution operates a trading desk involved in the cryptocurrency world, or why that same organization might have a different business unit that builds a custodial product for their tokenization efforts. I have sat in meetings with these types of entities and I do not recall hearing anarchy mentioned, but maybe my sample size is too small or outdated.4

Chapter 2: The History of Crypto

On p. 3 the authors put in a pullquote:

Cryptocurrencies were intended as a peer-to-peer medium of payment but have since morphed into a product whose purpose is almost exclusively as a speculative investment.

Perhaps Bitcoin and some of its immediate clones were intended for payments (at least according to the original whitepaper) but again, no citation for the latter claim about speculative investment. Maybe that is true. Either way, later in the book the authors change their tune and say that cryptocurrencies are a reimaging of money. There is little consistency from beginning to end.

The first couple pages describing “the Cypherpunk Era” are okay but the authors slip up stating:

In the 21st century, most money is digital, represented as numerical values in databases holding balance sheets for bank deposits.

This may seem pedantic but the authors do not state what part of the world they are describing in the 21st century. If it is the U.S. then they probably mean to use “electronic” not “digital.” There are no digital dollars in circulation yet as the Federal Reserve has not issued a central bank digital currency (CBDC).

Instead, users are often left with siloed representations of non-fungible dollars “issued” by a menagerie of entities, typically intermediaries such as commercial banks. The e-Cash Act and STABLE Act were a couple of proposals to move in that direction, but as of this writing we do not currently have a “digital dollar” in the U.S.

On p. 5 the authors write:

To most consumers today, this is transparent, although it was first, in the early 2000s that, consumers became aware of the digitization of their money in the form of increasing online banking.

Who are these consumers, where are they based? If the authors are describing the U.S. a future edition of the book should be specific.

Continuing on p. 5 they write:

However, in the early days of e-commerce, there was still apprehension around receiving and making payments over the internet with credit cards. To fill this gap, PayPal emerged as a service to support online money transfers, which allowed consumers and businesses to transact with a single entity that would process and transmit payments between buyers and sellers without the need for direct-to-bank transfers.

On the one hand it is clear why PayPal was used as an illustration for this evolving time period, yet it should not be trotted out as a “success story.”

As highlighted by legal scholars such as Dan Awrey, PayPal has always operated as a “shadow bank” and “shadow payment” provider.5 Its management shoe horned the company into the bedrock of U.S. e-commerce all while dodging banking regulators calls for the erection of a state or national-chartered bank.

While some readers may be okay with that outcome, Diehl et. al., explicitly deride this specific type of behavior from pegged coin issuers (stablecoins). Incidentally, in the process of writing this review, PayPal announced the release of a pegged, centrally-issued stablecoin – PYUSD – on the Ethereum network. How does PayPal operate now? The same as it always has: which happens to be very similar to how centralized stablecoin issuers.

On p.7 they write:

The mechanism described in the bitcoin whitepaper proposed a novel solution for the double-spend problem, which did not require a central trust authority.

This part of the chapter is fairly straightforward and dry and lacks any of the hysterical commentary. Since there is no unified voice, perhaps it was written by one of the two fellow co-authors?

Either way, it is not explored or mentioned in this chapter (or anywhere else) but of the eight references in the Bitcoin whitepaper, three of them cite the works of Haber & Stornetta, whose digital signing concepts illustrate that there are indeed “useful” things that the blockchain world has contributed (see slides 22-24). Of course that would be contrary to the narrative this book is attempting to defend.

Worth mentioning that the writers typically use lower case b and e for both bitcoin and ethereum even when they are discussing the networks and protocols. This is a little confusing because conventionally, it is fairly common to use lowercase b to describe the unit-of-account, whereas uppercase B to describe the network or code.

For instance on p. 8 they write:

Moreover, the bitcoin algorithm took a particularly interesting approach to consensus by attempting to create a censorship-resistant network where no participants is privileged. The consensus process was eventually consistent and tied the addition of new transactions to the solution of a computational problem in which computers that participated in the consensus algorithm would need to spend a given amount of computational work to attempt to confirm the writes. This approach, known as proof of work created what is known as a random sortition operation in which a network participant would be selected randomly and probabilistically based on how much computational power (called hashrate) was performed to attempt consensus.

A couple of nitpicks:

(1) There is no singular “bitcoin algorithm.” Arguably the best explanation of the moving parts that Bitcoin uses is from Gwern Branwen: Bitcoin is Worse is Better. This is not the only time the authors incorrectly describe a bundle of technology.

(2) The authors should be clearer that “proof of work” itself is a concept that pre-dates Bitcoin by more than a decade (Dwork & Naor 1993). Over the past five years, more of the technical-inclined papers on this topic typically refer to the way proof-of-work is used in Bitcoin as Nakamoto Consensus. The authors mention Nakamoto Consensus a few chapters later however they are strangely very thrifty when it comes to footnotes or citations so a second edition should include this nuance.

On p. 8 they write:

Therefore the bitcoin architecture created a computational game mechanic in which the computers in this network (called miners) competed to perform consensus actions and successfully confirming a block of transactions gave a fixed reward to the first “player” to commit a set transactions.

This is not quite right. A phenomenon called “orphaning” (similar to uncles in Ethereum) occurs when more than one miner simultaneously solves (discovers) a block. At some point one of the branches is orphaned (pruned) when other miners build on one but not the other tree.

This is part of the reason why a hardcoded 100 blocks (roughly ~17 hours) is required before a miner can issue themselves a block reward (e.g., the coinbase transaction has a block maturity time box).

A typo occurs on the last sentence of that paragraph:

The critical ideas encoded in the protocol are the predetermined release schedule, fixed supply, and support for those protocol changes that have support off a majority of participants.

This has a typo: off –> of

On p. 8 the authors write:

One of the core algorithms used in most blockchains is a hash function.

While reading this it was:

(1) unclear why they used ‘algorithm’ and;

(2) which blockchain does not use a hash function?

On p. 9 they discuss difficulty adjustments:

This mechanism allows the difficulty of bitcoin mining to be artificially adjusted proportionally to the rewards.

It is not quite clear what “artificial” means here. In Bitcoin, the supply schedule for the issuance of new bitcoins halves roughly every four years (actually less than four years but we will discuss that later).

Those with commit access could theoretically modify the fixed rewards / supply schedule, and miners could update their node software to increase or decrease that amount. But none of this action is artificial, so why use that word?

We could argue that chronologically early miners received a disproportionally higher amount of rewards relative to the frequent empty blocks they built and processed for the first ~5 years. Is that fair? Probably not. Is it artificial? Probably not.

On p.9 they discuss censorship resistance:

The censorship resistance of this algorithm was the critical improvement over existing eCash systems which previously had a single legal point of failure, in that the central register or central node would have to be stored in a single server that could be targeted by governments and law enforcement. In this trustless peer-to-peer (P2P) model–the same mechanism that powered Napster and BitTorrent–all computers participated in the network, and removing any one node would not degrade the availability of the whole network. Just as previous P2P networks routed around intellectual property laws, bitcoin routed around money transmitter laws.

There are a few issues with this:

(1) Which algorithm are the authors referring to as an “algorithm,” the entire Bitcoin codebase circa 2009?

(2) Napster was quasi-centralized, it provided an index of files and that is why it was a relatively easy target for lawsuits by the music industry (RIAA) and law enforcement.

(3) The authors have a habit of wading into legal and regulatory territory without providing much in the way of definitions or what jurisdictions they are describing.

For instance, in the last sentence they are probably referring to the U.S. In the U.S., each individual state has laws and regulations around money service businesses (MSB), of which money transmission (MTL) is a subset of. Some states do not. At the federal level some entities are required to register with FinCEN which enforces the Bank Secrecy Act (BSA). A second edition should include specific jurisdictions to strengthen the authors arguments.

(4) This may be perceived as pedantic, in section 1 of the original Bitcoin whitepaper it describes the motivation of building a network for participants to engage in online commerce without having to rely on financial institutions. Conventionally this is more of a stab at know-your-customer (KYC) collection gathering requirements.6

On p.10 they write about how Bitcoin was first marketed, stating:

This new era marks a rapid expansion of a cottage industry of startups and early adopters who would build exchanges, mining equipment, and market network to proselytize the virtues of this new technology. The culture around the extreme volatility of the asset created a series of memes within the subculture of HODL (a portmanteau of the term “holding,” standing for “hold on for dear life”), which encourages investors to hold the asset regardless of price movement.

Couple of issues:

(1) It is clear later in the book that the authors have a gripe about how blockchains are proselytized. I deeply sympathize with their disdain towards shilling. I violently agree with them in some parts. But, like in the rest of the book, they miss the opportunity to provide the reader with specific examples.

(2) I have pointed this out in several other book reviews but the etymology, the genesis of “hodl” did not originate as an acronym or portmanteau. It came from a drunk poster on the BitcoinTalk forum, there are many articles discussing this. However, what the authors describe “hodl” to mean is correct.

On p.11 they start a new section on the “grifter era,” stating:

In addition to bitcoin, a series of similar technologies based on the same ideas emerged in the 2011-2013 era. The first movers were Litecoin, Namecoin, Peercoin, and a parody token known as Dogecoin based on an internet meme.

Several issues with this:

(1) Why did the authors use uppercase for four cryptocurrencies instead of lowercase?

(2) A second edition should probably arrange the first three by chronology or alphabetized. For instance, Namecoin was an evolution of BitDNS (a project that was spun up just as Satoshi stopped formally contributing to Bitcoin). It was launched in April 2011 and due to its utility usually is not placed in the same category as Litecoin or Dogecoin.

In the same paragraph they note that:

As of August 2018, the number of launched cryptocurrency projects exceeded 1600.

It is unclear why the authors chose that specific time frame. For instance, according to CoinGecko, they have identified 10,052 coins as of this writing. The infrequently updated “Deadcoins” database lists 1729 entries as of January 2023.

The next sentence is a little quizzical:

In 2015 a significant extension to the bitcoin model called the ethereum blockchain was launched with the aim to build a “world computer” in which programmable logic could be expressed on the blockchain instead of only simple asset transfers.

It is only eleven pages into the book but we still have not been provided a clear definition of an “algorithm” versus a “model” versus a “protocol.”

Ethereum (which the authors do not capitalize either) is significantly different than Bitcoin so to call it an extension is a bit of a stretch.

Also, Bitcoin uses a transaction model called unspent transaction outputs (UTXOs) whereas Ethereum uses a different model called Accounts. The former is unable to actually transfer assets per se, hence the creation of “colored coin” schemes starting in 2012 to enable other assets to be created (nearly all of the original “colored coin” efforts have disappeared and heterogenous assets that use the Bitcoin blockchain are currently conductible via the Ordinals protocol).7

Two sentences later the authors change the capitalization again:

In addition to fully visible transaction models of previous tokens, chains such as Monero and Zcash would incorporate privacy-enhancing features into the design, allowing participants to have blinded transactions that would obscure the endpoint details for illicit transactions with no public audit record.

A second edition needs to explain why the authors flip capitalization around. Is it only uppercased if the chain is mentioned just once?

Later in the book the authors do go on to describe some of the privacy and confidentiality approaches but only with the context of criminogenic behavior. It could be helpful for readers to have some citations of relevant papers or articles since the topic intersects with securing accounts, assets, and transfers in traditional finance.8

The next paragraph jarringly switches gears to proof-of-work mining (without mentioning PoW):

Early entrepreneurs realized that they could gain an advantage over traditional server farms if they built faster and more specialized hardware to compute these hashes. These entrepreneurs began to build ASICs (Application Specific Integrated Circuit), custom hardware circuits that could do the computations required for the bitcoin network more efficiently than traditional CPUs offered by companies like Intel and AMD.

For some reason this section omits two intermediate steps between CPU mining and ASIC mining. These would be GPU mining and FPGA mining. More importantly it misses the opportunity of pointing out that Satoshi herself was surprised and sullen when she learned that miners had figured out how to scale GPU mining the way ArtForz and Laszlo Hanyecz revealed.

A few sentences later they dive into mining pools:

These mining pools became a centralized and very lucrative business for early investors. An example is, the Chinese company BitMain, which began to centralize most of the computational resources, resulting in 70% of all bitcoin mining being concentrated in mainland China by 2019.

The authors skip a few years and neglect to mention key figures in the creation of commercialized ASICs such as Yifu Guo. Nor do they mention, in dollars or some other figure, how lucrative these pools were. Or which the first public ones were (Slush and Eligius were among the first).

This section also conflates mining hardware (used in farms) with pools which provide the block building itself for an aggregation of mining farms. Lastly, the capitalization of BitMain is incorrect (the company markets the hardware in either all caps – BITMAIN – or Bitmain).

On p. 12 they write:

The underutilization of coal-fired power production and Chinese capital restrictions on renminbi outflows offered a unique opportunity for enterprising Chinese citizens to move capital outside of the mainland beyond government controls. In 2018 the Chinese government officially declared cryptocurrency minig an undesirable activity. The same year, Bloomberg reported $50 billion of capital flight from the Chinese state using the Tether cryptocurrency.

This is not the correct chronology. Because the authors do not provide many citations it is unclear what they were referring to in 2018. A quick googling found a possible related article but the actual real big ban took place in two separate actions in May and September 2021. As their book was published in mid-2022, the authors could have used more recent figures here.

Note: later in Chapter 25 they do reference a more up-to-date story. They also not explain the specific legal and regulatory woes that miners faced in China which led them to move hardware overseas in the second half of 2021.

In addition, the authors only mention energy generation in passing but neglect to mention a key culprit for why Bitcoin (and other PoW-based coins) flocked to specific regions of China: subsidized electricity from hydroelectric dams due to overcapacity / overproduction of dams. This has been widely documented by others.9

Some of the miners literally packed up their machines onto trains after the rainy season was over and decamped for provinces in the north such as Xinjiang and Inner Mongolia, where coal-fired plants powered their wares for the remainder of the dry season. A crazy phenomenon and one the authors should consider adding in the next edition.

On p. 12 they write:

The Grifter Era period also saw the introduction of stablecoins such as Tether, aiming to be a stable cryptoasset with its price allegedly pegged to the US dollar and theoretically backed by a reserve of other assets. This is followed by a 2019 period of market volatility and market consolidation of cryptocurrencies, during which many unfounded ideas fell off and left a handful of 20 projects which would dominated trading volume and developer mindshare.

In this section the authors never really define what time the “Grifter Era” takes place. Based on the actual words they wrote up until this point we have years: 2011-2013, 2015, 2017, 2018, and 2019. Yet they specifically mention a “stable cryptoasset with its price allegedly pegged to the US dollar” which sounds like a “stablecoin” such as Tether (USDT). But Tether was actually launched as Realcoin in 2014.

Also, the authors do not mention any of the “20 projects” which dominated volume and mindshare. Seems like a curious omission. Does that include Binance and Cosmos then?

The chapter comes to an abrupt end, with the final paragraph:

In 2021 China outright banned all domestic banks and payment companies from touching cryptoassets and banned all mining pools in the country. At the same time, the United States continued to be hit by an onslaught of cyberterrorism and ransomware attacks that began to attack core national infrastructure and the country’s energy grids.

What is the reader supposed to take away from this chapters concluding remark? Later in the book the authors dive into ransomware but readers are not provided any citations or sources for where we can learn more about these specific cyberattacks.

For example, prior to being blocked by him on Twitter, I briefly corresponded with Diehl regarding ransomware. I even agreed (and still agree) with some of his points he has made on the specific topic. Yet here he misses the opportunity to connect liquidity (and banked-trading venues) with ransomware payouts. The next edition to clarify the current non sequitur.

Chapter 3 Historical Market Manias

This is one of their stronger chapters. It succinctly discusses the history of past manias and subsequent crashes including the South Sea Bubble, the Mississippi Bubble, the Railway Mania, Wildcat banking, the 1929 stock market collapse, Albanian pyramid schemes, Enron, and others.

While most of the prose is in a unified voice, at the tail end of the Wildcat section on p. 26 they write:

The wildcat banking era is an important lesson to learn from the past, given the recent fringe efforts to return to a digital variant of private money with stablecoins and cryptoassets.

It is followed by three citations all related to the topic at hand. Yet the authors fail to distinguish – as they fail to distinguish later in the section on stablecoins – that in the U.S. all commercial banks issue the equivalent of private money and credit.

In fact, it is the expansion of this credit (and leverage) by private banks and other lending institutions that often leads to booms and busts in the modern era. During this time frame both M1 and M2 aggregates – publicly money – basically grew linearly apart from the recent COVID-era emergency responses.

This distinction is important because to be consistent, the authors should recognize that in the U.S. credit expansion from non-banks and certain fintechs like PayPal, fall under the umbrella of “shadow banking” and “shadow payments” which predates the creation of Tether (USDT) and other centralized pegged coins by decades.

To be consistent, the authors need to update their priors and at a minimum reconcile for the audience what they prescribe all “shadow banking” and “shadow payments” should be required (or not) to do. Singling out “private money” without recognizing the very important nuance that most money and credit retail users interact with is private, is disingenuous.

While talking about the history of Beanie Babies, on p. 33 they write:

Buyers of Beanie Babies could never find the whole collection in one store, and the artificially limited supply meant it always appeared that the products were selling out. By limiting the distribution channels, creating the toys as part of a broader collection and simultaneously creating a variable artificial scarcity within the collection, the company bootstrapped a collectible item seemingly based on a small children’s toy which had very little intrinsic value unto itself–Not unlike the crypto market for non-fungible tokens (NFTs) today.

This is not necessarily a bad example but there are two more germane examples with respect to collectible NFTs:

(1) In the U.S., baseball card production is a licensed activity based on I.P. that Major League Baseball (MLB) has a monopoly on.10 The manufacturing arrangement effectively states who can and cannot produce the likeness of players, coaches, teams, logos, etc. on memorabilia.

Over the past several decades, collectible card manufacturers have remained relatively static yet these manufacturers (such as Topps and Fleer) created a glut of cards in the lates ’80s and early ’90s.11

Coincidentally, in the process of writing this review, MLB sued Upper Deck, “accusing it of trademark infringement for using its logos on trading cards without permission.”

(2) Getty Images. While they do have some non-commercial, royalty free stock galleries, Getty acquires the I.P. of images and uses an army of lawyers to sue anyone who violates or infringes on those rights. They attempt to artificially restrict the usage of easily reproducible imagery. 12

On p. 24 the discuss the Dot-com bubble of 1995-2001, stating:

The most recent bubble in living memory was is the dot-com bubble in the 1990s.

Two issues with this sentence:

(1) Grammar or typo with “was is”

(2) The very next page they discuss the subprime mortgage crisis which seems to be chronologically at ends with “most recent bubble” for the dot-com bubble. Which is the most recent?

On the final sentence of p. 24 they write:

Shortly after that, the use of the web for private commercial applications exploded. The era saw the rise of Google, eBay, PayPal, and Amazon coupled a vast Cambrian explosion of both technologies and new business models.

While all four of these technically co-existed during the time frame stated, only two of them went public before the end of 2001, the timeframe they gave.

Also, it is unclear why these Big Tech companies repeatedly receive a free pass throughout the section and the whole book. Apart from one subsection later on Occupy Wall Street and a small passage in the Conclusion, one consistency throughout the book is that the authors seem to be okay with the status quo and incumbency of both legacy financial institutions and Big Tech companies.

This seems at odds with the view of holding entities such as pegged-coin issuers accountable since cloud providers are largely unaccountable systemic utilities.

For instance, academics such as Lee Reiners have argued that cloud providers – such as AWS and Google Computer – should be regulated under Dodd-Frank Title VIII. Likewise another scholar, Vili Lehdonvirta, has argued that these cloud empires are as powerful as states yet unaccountable.

Both Reiners and Lehdonvirta are typically categorized (incorrectly?) as anti-coiners yet both of them provide a much more even handed treatment of systemic risks, such as large commercial banks, than the authors of Popping the Crypto Bubble.

On p. 37 they discuss the subprime mortgage crisis of 2003-2008, writing:

In the decade of real estate euphoria, the amount of mortgage-derived credit increased from $900 billion to $62 trillion.

That seems like a pretty big change over time, but there is no citation for readers to learn more. A second edition should provide one.

On p. 39 they describe the venture capital bubble of 2010-present, discussing WeWork and Uber blitzscaling, writing:

While these companies did achieve scale, they became mired in controversy and scandals as a direct results of their predatory and unsustainable business model. Although both WeWork and Uber went public, neither company was able to become profitable and is now trading at fractions of their inflated private valuations.

In mid-2022, when the book was published, part of that closing statement was untrue. WeWork pulled its IPO in 2019 and merged with a SPAC for a direct listing in October 2021.13

The authors missed the opportunity to dunk on SPACs which screwed over retail investors.14

On p. 41 the authors wrote about the Crypto Bubble 2016-present, a lot of which I agreed with. However one passage quickly falls into a rant, on p. 42 they write:

The simple undoing of this idea of a new financial system is that there is no economy in crypto; because it can never function as a currency. Nothing is priced in crypto. No commerce is done in crypto. No developed economy recognizes crypto as legal tender or collects taxes on it. The price of crypto simply oscillates randomly, subject to constant market manipulation and public sentiments of greed and fear, detached from any activity other than speculation. Crypto is a pure casino investment wrapped in grandiose delusions. As an investment, it is almost definitionally a bubble because crypto tokens have no fundamentals, no income, and correspond to no underlying economic activity.

A second edition could reword and cut out half of the rant and turn it into a much stronger statement all without using broad sweeping a priori cudgels.

For instance, saying “never” implies the authors know the future. But they, like the readers, cannot know the future of every cryptocurrency or blockchain to come. We need to use the facts-and-circumstances, an evidence-based approach, to determine which cryptocurrency (or token) currently has legs and which ones do not. Saying they all cannot is sloppy and lazy polemics. It is soothsaying.

Another area for improvement: in 2014 Yanis Varoufakis may have been the first economist to articulate – in long form – that a cryptocurrency like bitcoin (with an inelastic supply) will unlikely to be part of a circular flow of income. The authors could add that reference to make their argument stronger, after all, they are no stranger to Varoufakis who they cite in the next chapter.

They could also make the distinction between an anarchic cryptocurrency such as bitcoin or litecoin, which have inelastic supplies versus Dai or Rai, which are only minted when collateral is deposited into a contract. This would take an additional explanation of dynamic supply via collateralized debt positions (CDP) but would help inform the reader that there is another world beyond fixed supply coins such as bitcoin and its antecedents.

Another example they could use to buff up their argument is to provide references of jurisdictions that did attempt to accept cryptocurrencies as a form of payment for taxes, but then later stopped the effort. Ohio is one example of this occurrence.

Chapter 4 Economic Problems

The first few pages of this chapter start off strong. I even found myself nodding in agreement when the pointed out on p. 46 the euphemism some coin promoters use “cryptoassets” in lieu of “cryptocurrencies” to make the former more palatable. We highlighted that in the book review of an equally bad book, Cryptoassets by Burniske and Tatar.

But then it begins to go off the rails, again, starting on p. 52 they write:

In addition, without any nation-state recognizing cryptocurrencies as its sole legal tender, there is no demand for the currency to pay one’s taxes. The demand for cryptocurrency is only based on either criminality or speculation.

The book is full of these opinions stated as facts.

Again, if there is one person who wants to agree with Diehl et. al., it is me. I have written a slew of posts and papers, most of which are linked to on this site, which have attempted to dive into these very topics. But they are not doing themselves any favors by being so stingy on citations or explaining how they arrived at only two categories: criminality or speculation.

And this hurts their credibility because their claims could be stronger by simply googling or asking experts if they know of a citation they could add. Right now, their bold confidence comes across identically as coin promoters who claim – without evidence – the central banks are going to collapse in the face of Bitcoin’s choo-choo-train.

To both groups of people we can respond with Hitchen’s razor: what can be asserted without evidence can also be dismissed without evidence. And unfortunately for Diehl et. al., a large portion of the book could simply be dismissed due to a lack of evidence (or citations).

While discussing deflationary assets, they write on p. 52:

The US dollar has the deepest and most liquid debt markets mainly because the dollar has a relatively predictable inflation rate on a long time scale, and its monetary parameters remain predictable up to the scale of decades. Thus the risk of servicing loans is readily quantifiable, and banks can build entire portfolios of loans to their communities out of their reserves.

A future version should explain that specifically the authors (likely) mean the market for U.S. Treasury bonds, not dollars themselves.

On p. 53 they write:

Unlike in the fiat system, where the market conditions for debt products organically determine the supply of money in circulation relative to demand, a cryptocurrency must determine both supply and demand prescribed in unchangeable computer code. This would be like if the United States Federal Reserve decided what the monetary policy of the United States would be from their armchair in 1973 and into the future, regardless of any future market conditions, pandemics, or recessions.

This is a bit of a strawman and lacks needed nuance.

(1) In the U.S. the majority of money and credit expansion (and contraction) comes from private, commercial banks and other lending institutions, not just the Federal Reserve.

(2) The authors criticism is valid with respect to coins with fixed supplies that are purposefully attempting to replicate “money” but not every cryptocurrency or token is attempting to do that. In fact, as mentioned above, both Dai and Rai are dynamically issued based on collateral deposited, there is no fixed supply of either.

(3) There seems to always be debates around “unchangeable computer code” but most of this ideological debate has been sidestepped by issuing new smart contracts with upgrades (or downgrades or sidegrades).

Either way, the authors could strengthen at least one of their arguments by referencing David Andolfatto’s 2015 presentation (at the time, Andolfatto was a vice president at the St. Louis Federal Reserve).

On p. 55 they write:

A positive-sum game is a term that refers to situations in which the total of gains and losses across all participants is greater than zero. Conversely, a negative-sum game is a game where the gains and losses across all participants sum is less than zero, and played iteratively with increasing participants, the number of losers increases monotonically. Since investing in bitcoin is a closed system, the possible realized returns can only be paid out from funds paid in by other players buying in.

Even though I largely agree with what they wrote here (and throughout much of the chapter), the authors introduce a new concept (a ‘closed system’) without defining what that is. And then they move on to the next thing to rail against.

It is frustrating because they could have explained to readers how, in proof-of-work networks such as Bitcoin, value leaks from the ecosystem: to state owned energy grids and semiconductor companies who typically do not reinvest the value (capital) back into the network.

Occasionally you will hear about a mining operator sponsoring a Bitcoin Core developer or helping with a lightning implementation, but by and large, the block rewards in Bitcoin are value that is extracted from the network by non-participants, or dead players.15 The authors do so somewhat later, but this would be a good place to drop a foreshadow towards that section, or at the very least define what a “closed system” is.

On p. 56 the authors inexplicably alternate between writing “a cryptoasset” and “crypto assets” within one paragraph.

Another example of a rant that takes away from the story they have built up through the chapter, on p.56 they write:

Crypto assets are completely non-productive assets; they have no source of income and cannot generate a yield from any underlying economic activity. The only money paid out to investors is from other investors; thus, investing in cryptoasssets is a zero-sum-game from first principles. If one investor bought low and sold high, another investor bought high and sold low, with the payouts across al market participants sum to zero. Crypto assets are a closed loop of real money, which can change hands, but no more money is available than was put in. Just as a game of libertarian musical chairs in which nothing of value is created, participants run around in a circle trying to screw each other before the music stops. This model goes by the name of a greater fool asset in which the only purpose of an investment is simply sell it off to a greater fool than one’s self at a price for more than one paid for it.

The voice of this author does not flow with the voices of the other authors. It sounds a lot like a long tweet and should be excised due to is repetitiveness. We get it, you hate cryptocurrencies / cryptoassets. It was clear the first dozen times you said it.

Another issue with this particular rant is that it inappropriately uses the term “first principles” when they probably should have used something like axiomatically. Or “by definition” which they have previously used. In addition, and more importantly, it is empirically incorrect.

There are blockchain projects, such as Onyx from JP Morgan that serve as a counterfactual to the a priori argument laid out above. A future edition either needs to reconcile with the fact that there are non-self-referential blockchain projects alive and in production, or excise the rants altogether.

On p. 58 they write:

Many economists and policymakers have likened cryptoassets to either Ponzi schemes or pyramid schemes, given the predatory nature of investing in cryptoassets. Crypto assets are not a Ponzi scheme in the traditional legal definition. Nevertheless, they bear all the same payout and economic structure of one except for the minor differentiation of a central operator to make explicit promises of returns. Some people have come up with all manner of other proposed terms of art for what negative-sum crypto investments might be called:

- Decentralized Ponzi scheme

- Headless Ponzi scheme

- Open Ponzi scheme

- Nakamoto scheme

- Snowball scheme

- Neo-Ponzi scheme

It would be nice if the authors came to consensus on whether it was spelled “crypto assets” or “cryptoassets.” Also, it is unclear who came up with the descriptive names above, however, it is likely that Preston Byrne should be credited with “Nakamoto Scheme.”

I currently think a decent description of Bitcoin itself is how J.P. Koning categorizes it as a game akin to a decentralized chain letter:16d

Overall this chapter sounds a bit too much like a rehashed version of BitCon from Jeffrey Robinson. It could easily be improved by removing the repetitious everything-is-a-fraud refrain and adding relevant references.

Chapter 5 Technical Problems

This chapter is tied with Exchanges for probably being the weakest in the whole book. Part of the problem is the authors conflate scaling limitations that Bitcoin specifically has, with the rest of the blockchain world. There is no nuance, they make a number of inaccurate statements, and the chapter itself is assembled in a haphazard fashion.

For instance, on p. 59 they write:

The fundamental technical shortcomings of cryptocurrency stem from four major categories: scalability, privacy, security, recentralization, and incompatibility with existing infrastructure and legal structures.

That is at least five categories. Yet the book subsections include four: scalability, privacy, security, and compliance. There is no specific section on ‘recentralization’ as most of it is mentioned within scalability.

Continuing, on p. 59 they write:

In computer science scalability refers to a class of engineering problems regarding if a specific system can handles the load of users required of it when many users require it to function simultaneously. However regarding this problem, the technological program of bitcoin carries the specific seed of its own destruction by virtues of being tied to a political ideology. This ideology opposes any technical centralization, and this single fact limits the technical avenues the technology could pursue in scaling.

The entire chapter should be re-titled “Technical limitations of Bitcoin” because currently it is filled with strawmen. It appears that the authors have spent almost no time with blockchains beyond Bitcoin and Ethereum. Blockchain engineers and architects are well aware of these limitations and some have launched faster, more scalable “layer 1” blockchains in responses.

Note: these are not endorsements. Some examples include Algorand, Avalanche, Cosmos, Near, Polkadot, and Solana. All of these existed prior to the publication of their book.

Others have built “layer 2” rollups that sit-atop a layer 1 blockchain; these L2s are often significantly faster than the L1 they reside on top of. This includes Arbitrum, Base, Optimism, and zkSync. Even though both optimistic rollups and zk-rollups concepts existed prior to the publication of this book, yet they get barely a passing mention on page 63.

Continuing on p. 60 they write:

The bitcoin scalability problem arises from the consensus model it uses to confirm blocks of pending transactions. In the consensus model, the batches of committed transactions are limited in size and frequency, and tied to a proof of work model in which miners must perform bulk computations to confirm and commit the block to the global chain. The protocol constrains a bitcoin block to be no more than 1MB in size and a single block is committed only every 10 minutes. For comparison, the size of doing an average 3-minute song encoded in the MP3 format is roughly 3.5 MB. Doing the arithmetic on the throughput results in the shockingly low figure that the bitcoin network is only able to do 3-7 transactions per second. By comparison the Visa payment network can handles 65,000 transactions per second.

Working backwards, even though I agree with their point – and have even used Visa as an example – once again the authors do not provide any citations for anything above. There is no reason to be stingy across 247 pages.

But the bigger issue is that the authors fail to see how even forks and variants of Bitcoin itself – such as Bitcoin Cash – have successfully increased the block size to 32 MB, so it is possible to do it. With faster block times and a move over to proof-of-stake, block throughput on a future iteration of Bitcoin could be considerably faster than it is today.17

The problem that the authors almost identified is that between 2015-2017 prominent Bitcoin maximalists purged the Bitcoin Core community of “bigger block” views which then ossified Bitcoin development. Even so, the authors should have included the fact that SegWit and Taproot – both of which were locked in prior to the publication of this book – effectively allow for larger block sizes (to more than 2 MB).

On p. 61 they write:

An appropriate comparison would be the Visa credit card network, whose self-reported figures are 3,526 transactions per second. Most credit card transactions can be confirmed in less than a minute, and the network handles $11 trillion of exchange yearly. Credit cards and contactless payments are examples of a success story for digital finance that have become a transparent part of everyday life that most of us take for granted. The comparison between bitcoin and Visa is not perfect, as Visa can achieve this level of transaction throughput by centralizing transaction handling through its own servers that has taken thirty years of building services to handle this kind of load. The slow part of transaction handling is always compliance, ensuring parties are solvent, and detecting patterns of fraudulent activity. However, for the advocates proposing that bitcoin can handle retail transactions loads on a global scale, this is the definitive benchmark that must be reached for technical parity.

There a singular citation provided, but nothing from Visa itself. But the biggest problem with this passage is that it defends rent-seeking incumbents. In the U.S., Visa and Mastercard operate a duopoly that is good for their shareholders.

The next edition of this book needs to include an honest and frank conversation about the friction-filled payment infrastructure that allows private companies to extract rents on retail users in the U.S. For instance, two months ago a bi-partisan bill was introduced in both the House and Senate: “the Credit Card Competition Act, which would require large banks and other credit card issuers with over $100 billion in assets to offer at least two network choices to process and facilitate transactions, at least one of which must not be owned by Visa or Mastercard.”

Perhaps the bill goes nowhere, but the grievances it highlights are relevant for this book. For example, the E.U. capped interchange fees in 2015. Should Americans be granted lower fees as well?

Note: we are fortunate that public infrastructure upgrades, such as FedNow, will lower the costs to users across the country, however that is not intended as a point-of-sale or even retail-facing infrastructure (FedNow is an upgrade to the back-end). Plus its adoption may be slow.

This conversation could also discuss how commercial banks historically suffer from vendor lock-in from core banking software providers (such as FIS, Fiserv, Jack Henry), a cost that is eventually passed down to users as well.18

Also, it is worth pointing out that despite the authors celebratory mood towards Visa and Mastercard, according to the Bank of Canada many merchants do not actually like them:

Lastly, the only people who are still claiming that “bitcoin can handle retail transactions loads on a global scale” are Bitcoin maximalists. While very vocal on social media, fortunately they represent a small minority of the fintech world.

Yet the authors repeatedly build strawmen arguments to counter the maximalist viewpoint without (1) identifying an specific examples; (2) without acknowledging that there is more to the blockchain universe than an orange memecoin that is ossified.

On p. 61 they write:

The scalability issues of the bitcoin protocol are universally recognized, and there have been many proposed solutions that alter the protocol itself. Bitcoin development is a collaboration between three spheres of influence: the exchanges who onboard users and issue the bulk of transactions, the core developers who maintain the official clients and define the protocol in software, and the miners who purchase the physical hardware and mine blocks. The economic incentives of all of these groups are different, and a change to the protocol would shift the profit centers for each of the groups. For example, while the exchanges would be interested in larger block sizes (i.e., more transactions), the miners (who prioritize fee-per-byte) would have to purchase new hardware and receive less in mining rewards for more computational work and thus incur significant electricity cost. This stalemate of incentives has led to mass technical sclerosis of the base protocol and a situation in which core developers are afraid of major changes to the protocol for fear of upsetting the economic order they are profiting from.

There are plenty of good arguments to be made about challenges and issues surrounding Bitcoin, this is not one of them.

For starters, there is no citation for “bulk of transactions.” In the past, some centralized exchanges have attempted to bulk release transactions on-chain, however the authors do not give us any idea what percentage as of mid-2022.19

Chain analytics companies such as Elliptic and Chainalysis likely have some idea, it is unclear if anyone reached out to discuss it with them.20

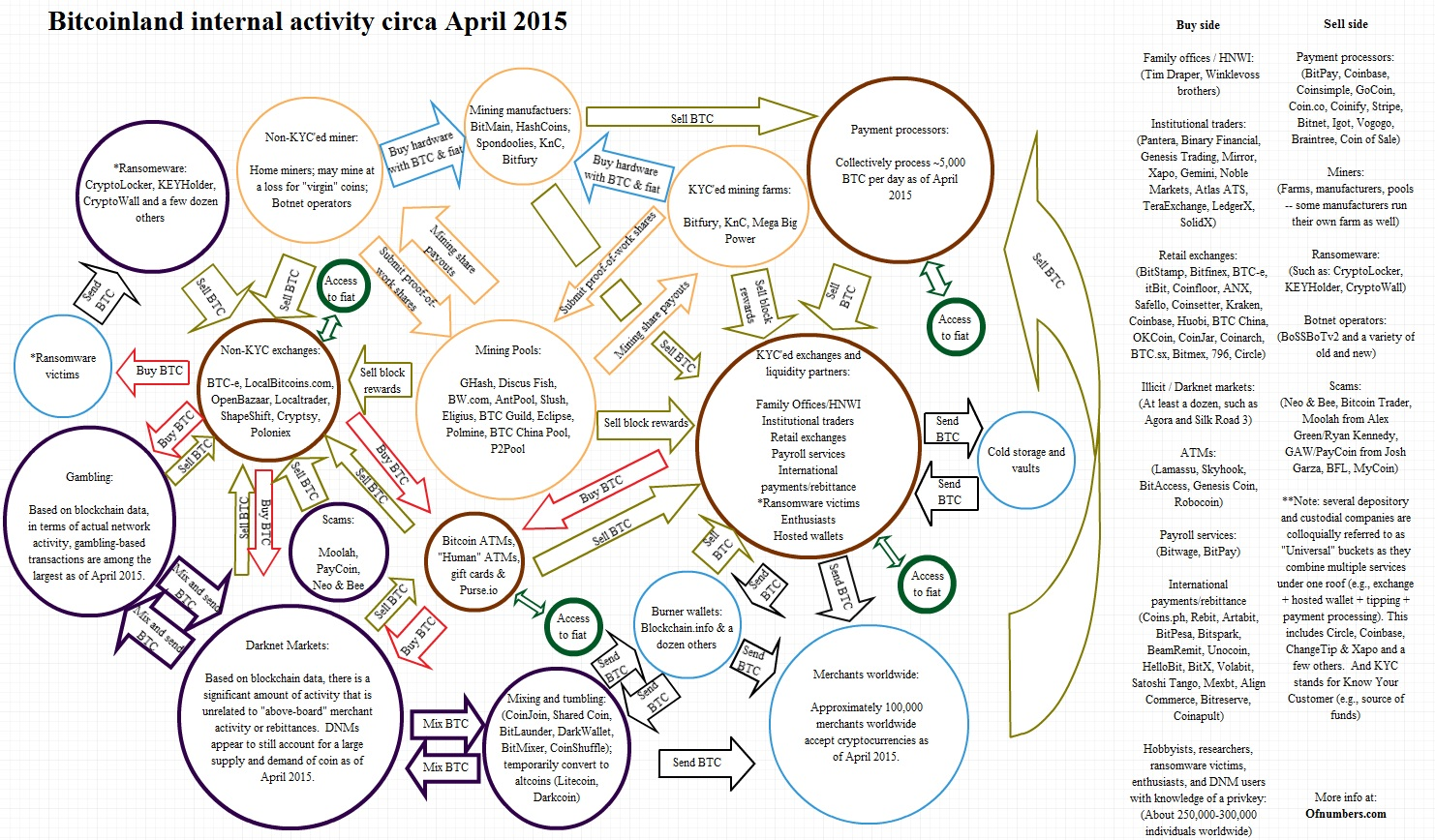

Strangely the authors do not use a single chart or image throughout the book which is somewhat weird considering how many visuals could help their arguments.

For instance, above is a line chart from Bitinfo Charts showing the daily on-chain transaction usage of Bitcoin over the past three years. The black vertical line is the date the book was published. We can see that up until this past spring, on-chain transaction volume fluctuated roughly between 250,000 and 350,000 transactions per day.

The recent uptick in late April this year is due to the popularity of Ordinals, a new NFT-focused protocol that uses Taproot (an “upgrade” implemented about two years ago).

Furthermore, and most importantly: an increased block size does not force miners to purchase new hardware and receive less mining rewards and higher electricity costs. This is not even an argument that “small block” proponents such as Luke-Jr have made.21 It is just plain wrong.

Recall that “mining blocks” for proof-of-work networks has split the “mining” job into two separate organizational efforts: (1) mining farms, which operate hashing equipment; (2) mining pools, which aggregate the work generated by mining farms, into a block.

Larger block sizes do not create any new difficulty or work for mining farms, the entities who have to deal with changing electrical costs. Rather, block makers (mining pools) have to spend an extra few seconds validating and sorting transactions.

This is why the “small(er) block” argument was fundamentally wrong and why other blockchains, especially proof-of-stake based ones, have successfully increased block sizes and reduced block intervals. Mining farms typically only purchase new hardware when their current gear is no longer profitable to mine with, a larger block size is not one of those reasons.

Also, it is unclear which developers the authors spoke with but usually most developers that earn a salary or “profit” off of Bitcoin development are those that work at a company that operates mining equipment, such as Blockstream.

On p. 62 they discuss the overhyped lightning network, writing:

The lightning network itself introduces a whole new set of attack vectors for double spends and frauds as outlined in many cybersecurity papers such as the Flood and Loot attack. This attack effectively allows attackers to make specific bulk attacks on state channels to drain users’ funds. The lightning network is an experimental and untested approach to scaling, with progress on this scaling approach having stagnated since 2018. According to self-reported lightning network statistics, less than 0.001% of circulating bitcoin were being managed by the network, and transactions volume has remained relatively flat after 2019. No merchants operate with the lightning network for payments and as of today it is nothing more than a prototype.

I tend to agree with the authors views that lightning is mostly vaporware. Yet there are probably more accurate arguments than theirs. For starters, lightning is not “untested.” It is has been live and in the wild for years.

Second, according to Bitcoin Visuals, both nodes and channels were increasing during the first half of 2022 when this book was published. Specifically it is the network capacity and capacity per channel that have stagnated or declined (something the authors could mention). However, one counter-point that a lightning promoter could rightly make is that a small amount of bitcoin (sats) could in theory be used in a high velocity (high turnover) manner.

For instance, even though the velocity of M2 has declined over the past several decades yet we would not consider the U.S. economy as having declined over the same period of time. However we do not know what the velocity of sats is on lightning at this time. Perhaps it is negligible.

And lastly, I too am tired of the lightning promoters who used to say “it is only 18 month away.” Either way, the authors could use some other data and charts to back-up their thesis.

For example, the line chart (above) is from The Block which shows the capacity of lightning measured in USD and BTC over the past three years. The vertical green line is approximately when the book was published. As we can see, while the amount of BTC has increased about 20% since the book was written, as measured in real money (USD), the value locked-up on lightning has not really changed much in the past couple of years.

For comparison, above is a line chart from DeFi Llama. It shows the total value locked up (TVL) on Ethereum for the past five years measured in USD. The vertical dashed line is the date the book was published.

You can visibly see how the collapse of Terra (LUNA and UST) six weeks prior had immediate knock-on effects, sending the coin world into a bear market (as measured in USD).

On p. 63 they write:

Outside of the bitcoin network, there are similar problems in other cryptocurrencies. The bitcoin meme of technical indirection through Layer 2 solutions have been translated to other systems and their development philosophies. This perspective views the base protocol as being only a settlement layer for larger bulk transfers between parties, and those smaller individual payments should be handled by secondary systems with different transaction throughputs and consistency guarantees. The ethereum network has taken a different set of economic incentives in its initial design. At the time of writing, this network is still only capable of roughly 15 transactions per second. There is a proposed drastic protocol upgrade to this network known as ethereum 2.0 which includes a fundamental shift in the consensus algorithm. This project has been in development for five years and has consistently failed to meet all its launch deadlines, and it remains unclear when or if this new network will launch. Since this new network would alter the economics of mining the protocol, it is unclear if there will be community consensus between miners and developers that the protocol will go live or whether they will see the same economic stalemate and sclerosis that the bitcoin ecosystem observes. The ethereum 2.0 upgrade is unlikely to ever complete because of the broken incentives related to its development and roll-out.

Even in mid-2022 when this book was published, this fortune telling was a big L. Why? Because in December 2020 the proof-of-stake mechanism for Ethereum was successfully launched. It was called the Beacon Chain. Two months after the book was published, “The Merge” successfully occurred in which the proof-of-work function (and mining) were completely shut off.

Now you might be thinking that it is unfair to ding the authors and give them a loss on this prediction. But prior to The Merge, there were already about a half a dozen public Ethereum testnets that successfully transitioned from PoW to PoS. In either case, the authors should at the very least hedged their strong language.

It is worth pointing out that one of the anti-coiners that Stephen Diehl has endorsed (and cited) is Hilary Allen, who used the Financial Times to push a similar set of inaccurate predictions regarding Ethereum around the same time frame. This non-empirical, a priori approach does not help the credibility of their arguments. Reconsider citing them.22

For instance, on p. 63 they write:

The broader cryptocurrency community has seen a zoo of alternative proposed scaling solutions, these proposals going by the technical names such as sidechains, sharding, DAG networks, zero-knowledge rollups and a variety of proprietary solutions which make miraculous transaction throughput claims. However the tested Nakamoto consensus remains the dominant technology. At the time of writing, there is little empirical evidence for the viability of new scaling solutions as evidenced by live deployments with active users. Central to the cryptocurrency ideology is a belief that this technical problem must be tractable, and for many users, it is a matter of faith that a future decentralized network can scale to Visa levels while maintaining censorship resistance and avoiding centralization.

There are a few issues with this including the fact that the authors lump a bunch of technical names together without providing any context. This is a disservice to the reader who should google them to understand the nuances of say, sharding and zero-knowledge rollups.

Secondly, the authors introduce “Nakamoto consensus” for the first time without providing any context or definitions. Recall that pages ago this was noted as term that is conventionally used in long-form writing. It is good that they are aware of the term, but it is unfortunate that it came this far into the book and without any context.

Lastly, not every single cryptocurrency project or even blockchain effort is explicitly targeting “Visa levels.” Some blockchains that can process a few hundred transactions per second (TPS) are not trying to be a universal settlement layer. This is a strawman argument.

In addition, not that it should matter but Visa itself has both invested in blockchain-related companies for at least seven years and has partnered with other blockchain-related projects and even conjured up a way to pay for ETH gas fees with credit cards.23 Blockchains can be used for more than just money and payments, the authors should hedge their a priori mantra in the next edition.

For what it is worth, I am also skeptical that some of the L2s that have been announced for Ethereum will see a large amount of active users anytime soon. But it is disingenuous to throw the baby out with the bath water like the authors routinely do.

For instance, L2Beat is a frequently updated site that illustrates the total value locked (TVL) across more than two dozen L2s. It is worth keeping an eye on because TVL is one piece of evidence to back up a claim.

On p. 64 they write:

However, the inescapable technical reality is that every possible consensus algorithm used to synchronize the public ledger between participants are all deeply flawed on one of several dimensions: they are either centralized and plutocratic, wasteful, or an extraneous complexity added purely for regulatory avoidance.

This false dichotomy could easily be turned on the authors: guess who also operates centralized ledgers? Too big to fail banks. Are the participants also plutocratic and wasteful? This is not really the place to turn the tables on the authors but it is clear, one-third into the book, they have it out for public chains due to an ideology that regularly provides incumbents a free pass.

Why is that? It is possible to be both critical of cryptocurrency zealotry and also systemically important financial institutions (SIFIs). It is not one or the other. Why carry water for High Street banks? Let us not cherry pick favorites.

On p. 64 they write:

A consensus system that maps wasted computation energy to a financial return, both in electronic waste and through carbon emissions from burning fossil fuels to run mining data centers, is Proof of Work. Proof of work coins such as bitcoin is an environment disaster that burns entire states’ worth of energy and is already escalating climate change, vast amounts of e-waste, and disruption to silicon supply chains (see Environmental Problems). The economies of scale of running mining operations also inevitably result in centralized mining pools which results in a contradiction that leads to recentralization.

I agree with the authors, and have written so elsewhere.

However, a nitpick, the centralization of mining pools arose due to variance in mining rewards, and are not related to running mining farms. Pooling hashrate helps smooth out payouts much like pooling lottery tickets does in an office lottery pool.

On p. 64 they write:

The alternate consensus model proof of stake is less energy-intensive; however its staking model is necessarily deflationary; it is not decentralized, and thus results in inevitably plutocratic governance which makes the entire structure have a nearly identical payout structure to that of a pyramid scheme that enriches the already wealthy. This results in a contradiction that again leads to recentralization, which undermines the alleged aim of a decentralized project. The externalities of the proof of stake system at scale would exacerbate inequality and encourage extraction from and defrauding of small shareholders.

What is the source for everyone one of those claims? It is unclear.

The authors do provide a single reference from David Rosenthal attached to the final sentence of the paragraph. Rosenthal’s post primarily focuses on maximal extractable value (MEV) which is not a topic that comes up in this chapter or anywhere in the book.

It is possible that the authors were referring to Ethereum for some of their arguments.

For the sake of brevity, let us assume the authors are 100% correct about Ethereum having all of the failing listed above. But Ethereum was not the only public chain using proof-of-stake in mid-2022. Which of say, the top 20 PoS networks was decentralized? The authors do not even provide a metric for readers to measure or understand what is or is not decentralized.

For instance, the authors could have created a table that provides how many validators and/or validating pools per chain, or the distribution of tokens, of the percentage of token supply that is staked, and so forth.24

How are readers supposed to get on board and agree with the authors when the authors spend every other page ranting rather than providing coherent, evidence-based arguments?

On p. 64 they write:

Any Paxos derivative, PBFT, or proof of authority systems are based on a quorum of pre-chosen validators. In this setup, even if they are permissionless in accepting public transactions, the validation an ordering of these transactions is inherently centralized by a small pool of privileged actors and thus likewise involves recentralization. Any other theoretical proposed system that is not quorum-based and requires no consumption of time/space/hardware/stake resources would be vulnerable to Sybil attacks which would be unsuitable for the security model of a permissionless network.

The only reference the authors provide a single link regarding Sybil attacks to a presentation from David Rosenthal.

What is Paxos? What is PBFT? What is proof of authority? Once again the authors throw these acronyms and terms at the audience without even briefly describing them anywhere. What is proof of time or proof of space? Readers can clearly google after the fact, and find things on Chia or Bram Cohen, but why did the authors not feel compelled to provide any context?

The final sentence itself can be chucked out the window due to Hitchen’s razor: that which can be asserted without evidence, can be dismissed without evidence. This book has not created credibility for the authors, rather, just the opposite.

On p. 64 they conclude:

The fundamental reality is that cryptocurrency currently does not scale and cannot adapt itself to fit the existing realities of how the world transacts. The technology can never scale securely without becoming a centralized system that undermines its very existence.

One of the citations is to an article about how almost no one uses bitcoin for commerce – a comment I tend to agree with. The other reference is to another presentation from David Rosenthal. Even if Rosenthal endorsed their views it is still an a priori claim.

And more importantly: the onus is on the party making the positive claim. Their strident language “never scale securely” leaves no wiggle room and is tantamount to fortune telling.

On p. 66 they have dived into the privacy section, writing about Bitcoin:

This features means that while accounts are anonymous, the global transaction data can be used to infer specific properties about when, with whom, and in what amounts an address is transacting.

This is not quite true for other chains. A user (or organization) can run a node or a bunch of nodes scattered around the global and may be able to infer some information. But once the activity goes off-chain, into a custodian like a centralized exchange, then inferences become guesses without direct access.

On p. 66 they write:

The tracking and tracing of bitcoin involved in criminal activities has emerged as a standard practice in law enforcement and emerging companies such as ChainAnalysis have been able to deduce quite a bit of implied information simply from public information. Unlike with bank accounts, law enforcement does not require a subpoena of public information for an ongoing investigation. Notoriously many users of darknet services such as the Silk Road were caught because of a misunderstanding about the transparency of the bitcoin ledger used by these actors.

Couple of issues:

(1) Spelling: ChainAnalysis should be corrected to read Chainalysis

(2) While the authors are probably correct, the last sentence needs a citation or reference. For instance, a highly cited relevant paper is: A Fistful of Bitcoins: Characterizing Payments Among Men with No Names by Meiklejohn et al.

On p. 67 they discuss traditional banking, writing:

When a wire transfer is issued by a company whose corporate account is at HSBC in London to Morgan Stanley in New York City, the metadata contained within that transaction could contain commercially sensitive information. For example, if a British company is sending large amounts of funds to a newly created American division, it may indicate the intent for the company to expand into the American market. There are cases where the constellation of transactions between known entities could be used to deduce confidential information about the parties. However, this fact poses an existential question about the efficacy of cryptocurrency networks as an international payment system if pseudonymous accounts leak information.

Perhaps Flashboys is a little out-of-date but it could be worth mentioning the role high-frequency trading firms play(ed) in this scenario. This type of scenario exists in the cryptocurrency world too, as analytics firms provide granular on-chain data to trading firms (and sometimes the trading firms themselves build a boutique set of tools).25

On p. 69 they write about security:

In addition, these exchanges are some of the most targeted entities on the planet for hackers. In 2019, twelve major exchanges were hacked and the equivalent of $292 million was stolen in these attacks. Over time and in conjunction with bubble economics, these events have only increased in severity and frequency.

This could be true but where is the citation for the final sentence? Do the authors mean to also include decentralized exchanges (such as automated market makers) as well as bridges?

On p. 69 they write:

While some best practices can mitigate this risk, the fundamental design of bitcoin-style systems is that the end-user is responsible for their own keys and wallets by safeguarding their cryptographic secrets. This can be done through several strategies. So-called cold wallets are wallet key stored in physical objects such as paper and not connected to electronic devices.

Couple of questions:

(1) What is a “bitcoin-style system”? Do the authors mean blockchains in general or forks of Bitcoin or UTXO-based blockchains?

(2) Why do they say “so-called”? Private key management has been an ongoing area of trial-and-error since at least the invention of public key cryptography by Martin Hellman, Ralph Merkle, and Whitfield Diffie.

On p. 70 they write:

There are many news stories of ransom, kidnapping, and murder of crypto asset holders who attempted to safeguard their wallets personally.

Any chance they could refer to or cite one of them in a future edition?

On p. 70 they conclude with:

Of course, the natural solution to this would simply be that most users should not be their own bank; instead, they should use a “cryptobank” which holds their funds and provides them access. However, this is ultimately just recreating the same centralized authority system which cryptocurrency advocates attempted to replace. Providing cryptocurrency security for the masses either introduces more social problems that thee technology has no answer to or results in a recentralization that undermines its own idological goals. After all, we already have centralized banks and existing payment systems that work just fine.

While I agree with the first part of this passage, that a considerable amount of effort and resources has recreated the same sorts of centralized organizations but with less accountability and recourse, there are at least three problems with their patronizing tone:

(1) Typo “thee” should be “the”

(2) What jurisdictions are they writing about?

(3) Most importantly: the authors explicitly defend incumbents and legacy organization. They are defending a financial cartel without presenting any reasons to do so.

For example, because of implicit bail out expectations in the U.S., commercial banks are able to rent-seek off of society, as do private payment systems via usurious fees. While the authors pay some lip service in a section on “Occupy Wall Street” and in the “Conclusion” at the very end, it bears mentioning that executives and board directors at too big to fail (TBTF) institutions were not held directly accountable after massive bailouts in 2008-2009.

In point of fact, systemically important financial institutions (SIFIs) have become more concentrated since Dodd-Frank was passed in 2010. In the U.S., the deregulation of “midcap” regional banks in 2018, partially led to the subsequent collapse of several high profile commercial banks eight months ago, including Silicon Valley bank, Silvergate bank, and Signature bank. All of which required FDIC assistance to wind down.

Clearing houses (CCPs) are larger than ever and their systemic importance creates an implicit government bailout expectation which results in an ongoing moral hazard situation.26

In the U.S., not only are retail users stuck with a duopoly that extract rents but users are expected to regularly provide third parties with personally identifiable information (PII) to improve the user experience of sending funds in real time via fintech apps (like Venmo). This includes, normalizing man-in-the-middle (MITM) attacks through apps like Plaid, which integrate with retail banks.

I personally do not think most cryptocurrency projects or efforts solve any of these issues, but there is no reason to carry water for the status quo like the authors repeatedly do. Again, it is possible to critique both the world of blockchains as well as traditional finance. They are not mutually exclusive.

On p. 70 they start discussing compliance, writing:

The movement, storage, and handling of money are regulated, and most countries have laws on the international movement of funds. Showing up at an airport in Berlin with undeclared cash above €10,000 will and one in quite a bit of trouble.

What kind of trouble? Jailtime? No one knows because the authors drop that warning in the middle of a paragraph and go along.

On p. 72 they discuss cross-border payments and international money transfers, stating:

The inability to move money from a country is ultimately one of domestic internal infrastructure development and external international relations, rather than technical limitations Moreover, the proposed use case for cryptocurrency as a mode of international remittances is fundamentally limited because of a lack of a coherent compliance story. Even if we were to use cryptocurrency as a hypothetical international settlement medium, this system has not removed financial institutions from the equation. The system’s entry and exit points would have to perform the same checks of outgoing and incoming money flow required by many international agreements.

In general this is accurate and I even agree with the thrust of their argument. However it still lacks nuance because they do not specify which cryptocurrencies they are discussing.

For instance, SaveOnSend has chronicled the rise and fall of “rebittance” companies (Bitcoin-focused remittance providers) for years. And the graveyard for such startups is deep and wide.27

But the nuance the authors should make is that there is a clear distinction between Bitcoin (with a fixed supply) and a pegged stablecoin such as Dai or LUSD (from Liquity) which are dynamically minted, there is no fixed supply. Whether Dai or LUSD are used for international payments is something they could discuss, maybe neither are?

The passage also lacks any specifics or citations. A future edition could discuss the costs and frictions associated with correspondent banking and SWIFT’s decision to deploy gpi as a reaction to blockchain euphoria.28

Lastly, and perhaps importantly, it does not include discussions around real world asset-linked peggedcoins such as USDC and USDT.

Without detracting too much from the book itself, it is worth pointing out that the idea of commercial banks directly issuing “stablecoins” has been a topic of discussion since at least 2015.

At R3, some banks that participated in Project Argent later joined IBM’s now defunct endeavor called World Wire which used Stellar. One of the challenges that frequently surfaced during these experiments and deployments involved the legality of granting interest to token holders.

This is still a touch-and-go hot potato as we can see with the roll out of the European Union’s Markets in Crypto-Assets (MiCA).29 A second edition could also discuss this possibility in the CBDC section later on.

And since the authors seem very focused on the U.S., they might want to discuss the recent supervisory actions from the Federal Reserve regarding how domestic banks can transact with pegged stablecoins. But enough of doing their homework for them.

On p. 73 they conclude, stating:

Of course, like all cryptocurrency arguments, the counterargument is ideological: compliance is a non-issue because nation-states should not exist and should not have capital controls. This ideological goal is inexorably embedded in the design of cryptocurrency, making it an unscalable and untenable technology for any real-world application where sanctions, laws, and compliance are an inescapable part of doing business in financial services.

The sole citation is to a decent paper from Brian Hanley, about Bitcoin and just Bitcoin. The authors once again created a strawman and used it to broadly smear all cryptocurrency-related projects, even those unrelated to Bitcoin. This is lazy.

While I agree with some of their conclusions, an empirical-based investigation for arguing their position would be to tediously dissect the issues and challenges of other blockchains too. Look at the facts-and-circumstances for each, just like public prosecutors do.

Chapter 6: Valuation Problems

On p. 76 they discuss asset classification, writing: