A friend of mine sent me a copy of The Truth Machine which was published in February 2018. Its co-authors are Michael Casey and Paul Vigna, who also previously co-wrote The Age of Cryptocurrency a few years ago.

I had a chance to read it and like my other reviews, underlined a number of passages that could be enhanced, modified, or even removed in future editions.

Overall: I do not recommend the first edition. For comparison, here are several other reviews.

This book seemed overly political with an Occupy Wall Street tone that doesn’t mesh well with what at times is a highly technical topic.

I think a fundamental challenge for anyone trying to write book-length content on this topic is that as of 2018, there really aren’t many measurable ‘success’ stories – aside from speculation and illicit activities – so you end up having to fill a couple hundred pages based on hypotheticals that you (as an author) probably don’t have the best optics in.

Also, I am a villain in the book. Can’t wait? Scroll down to Chapter 6 and also view these specific tweets for what that means.

Note: all transcription errors are my own. See my other book reviews on this topic.

Preface

on p. x they write:

The second impact is the book you are reading. In The Age of Cryptocurrency, we focused primarily on a single application of Bitcoin’s core technology, on its potential to upend currency and payments.

Would encourage readers to peruse my previous review of their previous book. I don’t think they made the case, empirically, that Bitcoin will upend either currency or payments. Bitcoin itself will likely exist in some form or fashion, but “upending” seems like a stretch at this time.

On p. xi they write in a footnote:

We mostly avoid the construct of “blockchain” as a non-countable noun.

This is good. And they were consistent throughout the book too.

Introduction

They spent several pages discussing ways to use a blockchain for humanitarian purposes (and later have a whole chapter on it), however, it is unclear why a blockchain alone is the solution when there are likely other additional ways to help refugees.

For instance, on p. 3 they write:

Just as the blockchain-distributed ledger is used to assure bitcoin users that others aren’t “double-spending” their currency holdings – in other words, to prevent what would otherwise be rampant digital counterfeiting – the Azraq blockchain pilot ensures that people aren’t double-spending their food entitlements.

But why can’t these food entitlements be digitized and use something like SNAP cards? Sure you can technically use a blockchain to track this kind of thing, but you could also use existing on-premise or cloud solutions too, right? Can centralized or non-blockchain solutions fundamentally not provide an adequate solution?

On p. 4 they write:

Under this new pilot, all that’s needed to institute a payment with a food merchant is a scan of a refugee’s iris. In effect, the eye becomes a kind of digital wallet, obviating the need for cash, vouchers, debit cards, or smartphones, which reduces the danger of theft (You may have some privacy concerns related to that iris scan – we’ll get to that below.) For the WFP, making these transfers digital results in millions of dollars in saved fees as they cut out middlemen such as money transmitter and the bankers that formerly processed the overall payments system.

Get used to the “bankers” comments because this book is filled with a dozen of them. Intermediaries such as MSBs and banks do take cuts, however they don’t really dive into the fee structure. This is important because lots of “cryptocurrency”-focused startups have tried to use cryptocurrencies to supposedly disrupt remittances and most basically failed because there are a lot of unseen costs that aren’t taken into account for.

Another unseen cost that this book really didn’t dive into was: the fee to miners that users must pay to get included into a block. They mention it in passing but typically hand-waved it saying something like Lightning would lower those costs. That’s not really a good line of reasoning at this stage in development, but we’ll look at it again later.

On p. 6 they write:

That’s an especially appealing idea for many underdeveloped countries as it would enable their economies to function more like those of developed countries – low-income homeowners could get mortgages, for example; street vendors could get insurance. It could give billions of people their first opening into the economic opportunities that the rest of us take for granted.

That sounds amazing, who wouldn’t want that? Unfortunately this is a pretty superficial bit of speculation. For example, how do street vendors get insurance just because of the invention of a blockchain? That is never answered in the book.

On p. 7 they write:

The problem is that these fee-charging institutions, which act as gatekeepers, dictating who can and cannot engage in commercial interactions, add cost and friction to our economic activities.

Sure, this is true and there are efforts to reduce and remove this intermediation. The book also ignores that every cryptocurrency right now also charges some kind of fee to miners and/or stakers. And with nearly all coins, in order to obtain it, a user typically must buy it through a trusted third party (an exchange) who will also charge a markup fee… often simultaneously requiring you to go through some kind of KYC / AML process (or at least connect to a bank that does).

Thus if fee-charging gatekeepers are considered a problem in the traditional world, perhaps this can be modified in the next edition because these type of gatekeepers exist throughout the coin world too.

On p. 8 they list a bunch of use-cases, some of which they go into additional detail later in the book. But even then the details are pretty vague and superficial, recommend updating this in the next edition with more concrete examples.

On p. 9 they write:

Silicon Valley’s anti-establishment coders hadn’t reckoned with the challenge of trust and how society traditionally turns to centralized institutions to deal with that.

There may have been a time in which the majority of coders in the Bay area were “anti-establishment” but from the nearly 5 years of living out here, I don’t think that is necessarily the case across the board. Recommend providing a citation for that in the future.

On p. 10 they write:

R3 CEV, a New York-based technology developer, for one, raised $107 million from more than a hundred of the world’s biggest financial institutions and tech companies to develop a proprietary distributed ledger technology. Inspired by blockchains but eschewing that lable, R3’s Corda platform is built to comply with banks’ business and regulatory models while streamlining trillions of dollars in daily interbank securities transfers.

This whole paragraph should be updated (later in Chapter 6 as well):

- The Series A funding included over 40 investors, not 100+.

- The ‘community’ version of Corda is open sourced and available on github, so anyone can download, use, and modify it. There is also a Corda Enterprise version that requires a license and is proprietary.

- While initially eschewing the term “blockchain,” Corda is now actively marketed as a “blockchain” and even uses the handle @cordablockchain on Twitter, on podcast advertisements, and in public presentations.1

- I am unaware of any current publicly announced project that involves streamlining trillions of dollars in daily interbank securities transfers. Citation?

On p. 10 they briefly mention the Hyperledger Project. Recommend tweaking it because of its own evolution over the years.

For example, here is my early contribution: what is the difference between Hyperledger and Hyperledger.

On p. 11 they write:

While it’s quite possible that many ICOs will fall afoul of securities regulations and that a bursting of this bubble will burn innocent investors, there’s something refreshingly democratic about this boom. Hordes of retail investors are entering into early stage investment rounds typically reserved for venture capitalists and other professional.

This paragraph aged horribly since the book was published in February.

All of the signs were there: we knew even last year that many, if not all, ICOs involved overpromising features and not disclosing much of anything to investors. As a result, virtually every week and month in 2018 we have learned just how much fraud and outright scams took place under the guise and pretext of the “democratization of fund raising.”

For instance, one study published this summer found that about 80% of the ICOs in 2017 were “identified scams.” Another study from EY found that about 1/3 of all ICOs in 2017 have lost “substantially all value” and most trade below their listing price.

Future versions of this book should remove this paragraph and also look into where all of that money went, especially since there wasn’t – arguably – a single cryptocurrency application with a real user base that arose from that funding method (yet).

On p. 11 they write:

Not to be outdone, Bitcoin, the grandaddy of the cryptocurrency world, has continued to reveal strengths — and this has been reflected in its price.

This is an asinine metric. How exactly does price reflect strength? They never really explain that yet repeat roughly the same type of explanation in other places in this book.

Interestingly, both bitcoin’s price and on-chain transaction volume have dramatically fallen since this book was first published. Does that mean that Bitcoin weakened somehow?

On p. 12 they write:

Such results give credence to crypto-asset analysts Chris Burniske and Jack Tatar’s description of bitcoin as “the most exciting alternative investment of the 21st century.”

Firstly, the Burniske and Tatar book was poorly written and wrong in many places: see my review

Secondly, bitcoin is a volatile investment that is arguably driven by a Keynesian beauty contest, not for the reasons that either book describes (e.g., not because of remittance activity).

On p. 12 they write:

The blockchain achieves this with a special algorithm embedded into a common piece of software run by all the computers in the network.

To be clear: neither PoW nor PoS are consensus protocols which is implied elsewhere on page 12.

On p. 12 they write:

Once new ledger entries are introduced, special cryptographic protections make it virtually impossible to go back and change them.

This is not really true. For coins like Bitcoin, it is proof-of-work that makes it resource intensive to do a block reorganization. Given enough hashrate, participants can and do fork the network. We have seen it occur many times this year alone. There is no cryptography in Bitcoin or Ethereum that prevents this reorg from happening because PoW is separate from block validation.2

On p. 13 they write:

Essentially, it should let people share more. And with the positive, multiplier effects that this kind of open sharing has on networks of economic activity, more engagement should in turn create more business opportunities.

These statement should be backed up with supporting evidence in the next edition because as it stands right now, this sounds more like a long-term goal or vision statement than something that currently exists today in the cryptocurrency world.

On p. 13 they mention “disintermediation” but throughout the book, many of the cryptocurrency-related companies they explore are new intermediaries. This is not a consistent narrative.

On p. 14 they write:

If I can trust another person’s claims – about their educational credentials, for example, or their assets, or their professional reputation – because they’ve been objectively verified by a decentralized system, then I can go into direct business with them.

This is a non sequitur. Garbage in, garbage out (GIGO) — in fact, the authors make that point later on in the book in Chapter 7.

On p. 15 they write:

Blockchains are a social technology, a new blueprint for how to govern communities, whether we’re talking about frightened refugees in a desolate Jordanian output or an interbank market in which the world’s biggest financial institutions exchange trillions of dollars daily.

This is vague and lacks nuance because there is no consensus on what a blockchain is today. Many different organizations and companies define it differently (see the Corda example above).

Either way, what does it mean to call a blockchain “social technology”? Databases are also being used by refugee camp organizers and financial infrastructure providers… are databases “social technology” too?

Chapter 1

On p. 17 they write:

Its blockchain promised a new way around processes that had become at best controlled by middlemen who insisted on taking their cut of every transaction, and at worst the cause of some man-made economic disasters.

This is true and problematic and unfortunately Bitcoin itself doesn’t solve that because it also has middlemen that take a cut of every transaction in the form of a fee to miners. Future editions should add more nuance such as the “moral hazard” of bailing out SIFIs and TBTF and separate that from payment processors… which technically speaking is what most cryptocurrencies strive to be (a network to pay unidentified participants).

On p. 18 they write:

Problems arise when communities view them with absolute faith, especially when the ledger is under control of self-interested actors who can manipulate them. This is what happened in 2008 when insufficient scrutiny of Lehman Brother’s and other’s actions left society exposed and contributed to the financial crisis.

This seems to be a bit revisionist history. This seems to conflate two separate things: the type of assets that Lehman owned and stated on its books… and the integrity of the ledgers themselves. Are the authors claiming that Lehman Brother’s ledgers were being maliciously modified and manipulated? If so, what citation do they have?

Also a couple pages ago, the authors wrote that blockchains were social technology… but we know that from Deadcoins.com that they can die and anything relying on them can be impacted.

Either way, in this chapter the authors don’t really explain how something Bitcoin itself would have prevented Lehman’s collapse. See also my new article on this topic.

On p. 19 they write:

A decentralized network of computers, one that no single entity controlled, would thus supplant the banks and other centralized ledger-keepers that Nakamoto identified as “trusted third parties.”

Fun fact: the word “ledger” does not appear in the Bitcoin white paper or other initial emails or posts by Nakamoto.

Secondly, perhaps an industry wide or commonly used blockchain of some kind does eventually displace and remove the role some banks have in maintaining certain ledgers, but their statement, as it is currently worded, seems a lot like of speculation (projection?).

We know this because throughout the book it is pretty clear they do not like banks, and that is fine, but future editions need to back up these types of opinions with evidence that banks are no longer maintaining a specific ledger because of a blockchain.

On p. 20 they write:

With Bitcoin’s network of independent computers verifying everything collectively, transactions could now be instituted peer to peer, that is, from person to person. That’s a big change from our convoluted credit and debit card payment systems, for example, which routes transactions through a long sequence of intermediaries – at least two banks, one or two payment processors, a card network manager (such as Visa or Mastercard), and a variety of other institutions, depending on where the transaction take place.

If we look back too 2009, this is factually correct of Bitcoin at a high level.3 The nuance that is missing is that today in 2018, the majority of bitcoin transactions route through a third party, some kind of intermediary like a deposit-taking exchange or custodial wallet.4 There are still folks who prefer to use Bitcoin as a P2P network, but according to Chainalysis, last year more than 80% of transactions went through a third party.5

On p. 20 they write:

Whereas you might think that money is being instantly transferred when you swipe your card at a clothing store, in reality the whole process takes several days for the funds to make all those hops and finally settle in the storeowner’s account, a delay that create risks and costs. With Bitcoin, the idea is that your transaction should take only ten to sixty minutes to fully clear (not withstanding some current capacity bottlenecks that Bitcoin developers are working tor resolve). You don’t have to rely on all those separate, trusted third parties to process it on your behalf.

This is mostly incorrect and there is also a false comparison.

In the first sentence they gloss over how credit card payment systems confirm and approve transactions in a matter of seconds.6 Instead they focus on settlement finality: when the actual cash is delivered to the merchant… which can take up to 30+ days depending on the system and jurisdiction.

The second half they glowingly say how much faster bitcoin is… but all they do is describe the “seen” activity with a cryptocurrency: the “six block” confirmations everyone is advised to wait before transferring coins again. This part does not mention that there is no settlement finality in Bitcoin, at most you get probabilistic finality (because there is always chance there may be a fork / reorg).

In addition, with cryptocurrencies like Bitcoin you are only transferring the coins. The cash leg on either side of the transaction still must transfer through the same intermediated system they describe above. We will discuss this further below when discussing remittances.

On p. 20 they write:

It does so in a way that makes it virtually impossible for anyone to change the historical record once it has been accepted.

For proof-of-work chains this is untrue in theory and empirically. In the next edition this should be modified to “resource intensive” or “economically expensive.”

On p. 20 they write:

The result is something remarkable: a record-keeping method that brings us to a commonly accepted version of the truth that’s more reliable than any truth we’ve ever seen. We’re calling the blockchain a Truth Machine, and its applications go far beyond just money.

It is not a “truth machine” because garbage in, garbage out.

In addition, while they do discuss some historical stone tablets, they don’t really provide a metric for how quantitatively more (or less) precise a blockchain is versus other methods of recording and witnessing information. Might be worth adding a comparison table in the next edition.

On p. 21 they write:

A lion of Wall Street, the firm was revealed to be little more than a debt-ravaged shell kept alive only by shady accounting – in other words, the bank was manipulating its ledgers. Sometimes, that manipulation involved moving debt off the books come reporting season. Other times, it involved assigning arbitrarily high values to “hard-to-value” assets – when the great selloff came, the shocking reality hit home: the assets had no value.

The crash of 2008 revealed most of what we know about Wall Street’s confidence game at that time. It entailed a vast manipulation of ledgers.

This was going well until that last sentence. Blockchains do not solve the garbage in, garbage out problem. If the CFO or accountant or book keeper or internal counsel puts numbers into blocks that do not accurately reflect or represent what the “real value” actually is, blockchains do not fix that. Bitcoin does not fix that.

Inappropriate oversight, rubber stamp valuations, inaccurate risk models… these are off-chain issues that afflicted Lehman and other banks. Note: they continue making this connection on pages 24, 28, and elsewhere but again, they do not detail how a blockchain of some kind would have explicitly prevented the collapse of Lehman other other investment banks.

See also: Systemically important cryptocurrency networks

On p. 22 they write:

The real problem was never really about liquidity, or a breakdown of the market. It was a failure of trust. When that trust was broken, the impact on society – including on our political culture – was devastating.

How about all of the above? Pinning it on just one thing seems a little dismissive of the multitude of other interconnecting problems / culprits.

On p. 22 they write:

By various measures, the U.S. economy has recovered – at the time of writing, unemployment was near record lows and the Dow Jones Industrial Average was at record highs. But those gains are not evenly distributed; wage growth at the top is six times what it is for those in the middle, and even more compared to those at the bottom.

If the goal of the authors is to rectify wealth inequalities then there are probably better comparisons than using cryptocurrencies.

Why? Because – while it is hard to full quantify, it appears that on cursory examination most (if not all) cryptocurrencies including Bitcoin have Gini coefficients that trends towards 1 (perfectly unequal).

On p. 23 they write about disinformation in the US and elsewhere. And discuss how trust is a “vital social resource” and then mention hyperinflation in Venezuela. These are all worthy topics to discuss, but it is not really clear how any of these real or perceived problems are somehow solved because of a blockchain, especially when Venezuela is used as the example. The next edition should make this more clear.

On p. 29 they write:

On October 31, 2008, whil the world was drowning in the financial crisis, a little-noticed “white paper” was released by somebody using the pen name “Satoshi Nakamoto,” and describing something called “Bitcoin,” an electronic version of cash that didn’t need state backing. At the heart of Nakamoto’s electronic cash was a public ledger that could be viewed by anybody but was virtually impossible to alter.

One pedantic note: it wasn’t broadly marketed beyond a niche mailing list on purpose… a future edition might want to change ” a little-noticed” because it doesn’t seem like the goal by Nakamoto was to get Techcrunch or Slashdot to cover it (even though eventually they both did).

Also, it is not virtually impossible to alter.7 As shown by links above, proof-of-work networks can and do get forked which may include a block reorganization. There is nothing that technically prevents this from happening.

See also: Interview with Ray Dillinger

On p. 31 they write:

Szabo, Grigg, and others pioneered an approach with the potential to create a record of history that cannot be changed – a record that someone like Madoff, or Lehman’s bankers, could not have meddled with.

I still think that the authors are being a little too liberal with what a blockchain can do. What Madoff did and Lehman did were different from one another too.

Either way, a blockchain would not have prevented data – representing fraudulent claims – from being inserted into blocks. Theoretically a blockchain may have allowed auditors to detect tampering of blocks, but if the information in the blocks are “garbage” then it is kind of besides the point.

On p. 32 they write:

Consider that Bitcoin is now the most powerful computing network in the world, one whose combined “hashing” rate as of August 2017 enabled all its computers to collectively pore through 7 million trillion different number guesses per second.

[…]

Let the record show that period of time is 36,264 trillion trillion times longer than the current best-estimate age of the universe. Bitcoin’s cryptography is pretty secure.

This should be scrapped for several reasons.

The authors conflate the cryptography used by digital signatures with generating proofs-of-work.8 There are not the same thing. Digital signatures are considered “immutable” for the reasons they describe in the second part, not because of the hashes that are generated in the first.9

Another problem is that the activity in the first part — the hash generation process — is not an apples-to-apples comparison with other general computing efforts. Bitcoin mining is a narrowly specific activity and consequently ASICs have been built and deployed to generate these hashes. The single-use machines used to generate these hashes cannot even verify transactions or construct blocks. In contrast, CPUs and GPUs can process a much wider selection of general purpose applications… including serialize transactions and produce blocks.

For example: it would be like comparing a Falcon 9 rocket launch vehicle with a Toyota Prius. Sure they are nominally both “modes of transportation” but built for entirely different purposes and uses.

An additional point is that again, proof-of-work chains can and have been forked over the years. Bitcoin is not special or unique or impervious to forks either (here’s a history of the times Bitcoin has forked). And there are other ways to create forks, beyond the singular Maginot Line attack that the authors describe on this page.10

On p. 33 they write:

Whether the solution requires these extreme privacy measures or not, the broad model of a new ledger system that we laid out above – distributed, cryptographically secure, public yet private – may be just what’s needed to restore people’s confidence in society’s record-keeping systems. And to encourage people to re-engage in economic exchange and risk-taking.

This comes across as speculation and projecting. We will see later that the authors have a dim view of anything that is not a public blockchain. Why is this specific layout the best?

Either way, future versions should include a citation for how people’s confidence level increase because of the use of some kind of blockchain. At this time, I am unaware of any such survey.

On p. 34 they quote Tomicah Tilleman from the Global Blockchain Business Council, a lobbying organization:

Blockchain has the potential to push back against that erosion and it has the potential to create a new dynamic in which everyone can come to agree on a core set of facts but also ensure the privacy of facts that should not be in the public domain.

This seems like a non sequitur. How does a blockchain itself push back on anything directly? Just replace the word “blockchain” with “database” and see if it makes sense.

Furthermore, as we have empirically observed, there are fractures and special interest groups within each of these little coin ecosystems. Each has their own desired roadmap and in some cases, they cannot agree with one another about facts such as the impact larger block sizes may have on node operators.

On p. 35 they write:

If it can foster consensus in the way it has been shown to with Bitcon, it’s best understood as a Truth Machine.

This is a non sequitur. Just because Nakamoto consensus exists does not mean it that blockchains are machines of truth. They can replicate falsehoods if the blocks are filled with the incorrect information.

Chapter 2

On p. 38 they write:

Consider how Facebook’s secret algorithm choose the news to suit your ideological bent, creating echo chambers of like-minded angry or delighted readers who are ripe to consume and share dubious information that confirms their pre-existing political biases.

There are some really valid points in this first part of the chapter. As it relates to cryptocurrencies, a second edition should also include the astroturfing and censoring of alternative views that take place on cryptocurency-related subreddits which in turn prevent people from learning about alternative implementations.

We saw this front-and-center in 2015 with the block size debate in which moderators of /r/bitcoin (specifically, theymos and BashCo) banned any discussion from one camp, those that wanted to discuss ways of increasing the block size via a hardfork (e.g., Bitcoin XT, Bitcoin Classic).

This wasn’t the first or last time that cryptocurrency-related topics on social media have resulted in the creation of echo chambers.

On p. 43 they write:

The potential power of this concept starts with the example of Bitcoin. Even though that particular blockchain may not provide the ultimate solution in this use case, it’s worth recalling that without any of the classic, centrally deployed cybersecurity tools such as firewalls, and with a tempting “bounty” of more than $160 billion in market cap value at the time we went to print, Bitcoin’s core ledger has thus far proven to be unhackable.

There is a lot to unpack here but I think a future edition should explain in more detail how Bitcoin is a type of cybersecurity tool. Do they mean that because the information is replicated to thousands of nodes around the world, it is more resilient or redundant?

Either way, saying that “Bitcoin’s core ledger” is “unhackable” is a trope that should be removed from the next edition as well.

Why? Because when speaking about BTC or BCH or any variant of Bitcoin, there is only one “ledger” per chain… the word ‘core’ is superfluous. And as described above, the word “unhackable” should be changed to “resource intensive to fork” or something along those lines. “Unhackable” is anarchronistic because what the authors are probably trying to describe is malicious network partitions… and not something from a ’90s film like The Net.

Continuing on p. 43 they write:

Based on the ledger’s own standards for integrity, Bitcoin’s nine-year experience of survival provides pretty solid proof of the resiliency of its core mechanism for providing decentralized trust between users. It suggest that one of the most important non-currency applications of Bitcoin’s blockchain could be security itself.

This last sentence makes no sense and they do not expand on it in the book. What is the security they are talking about? And how is that particularly helpful to “non-currency applications of Bitcoin’s blockchain”? Do they mean piggy-backing like colored coins try to do?

On p. 44 they write:

The public ledger contains no identifying information about the system’s users. Even more important, no one owns or controls that ledger.

Well technically speaking, miners via mining pools control the chain. They can and do upgrade / downgrade / sidegrade the software. And they can (and do) fork and reorg a chain. Is that defined as “control”? Unclear but we’ll probably see some court cases if real large loses take place due to forks.

On p. 44 they write:

As such there is no central vector of attack.

In theory, yes. In practice though, many chains are highly centralized: both in terms of block creation and in terms of development. Thus in theory it is possible to compromise and successfully “attack” a blockchain under the right circumstances. Could be worth rephrasing this in the next edition.

On p. 44 they write:

As we’ll discuss further in the book, there are varying degrees of security in different blockchain designs, including those known as “private” or “permissioned” blockchains, which rely on central authorities to approve participants. In contrast, Bitcoin is based on a decentralized model that eschews approvals and instead banks on the participants caring enough about their money in the system to protect it.

This is a bit of a strawman because there are different types of “permissioned” blockchains designed for different purposes… they’re not all alike. In general, the main commonality is that the validators are known via a legal identity. How these networks are setup or run does not necessarily need to rely on a centralized authority, that would be a single point of trust (and failure). But we’ll discuss this later below.

On p. 44 they write:

On stage at the time, Adam Ludwin, the CEO of blockchain / distributed ledger services company Chain Inc., took advantage of the results to call out Wall Street firms for failing to see how this technology offers a different paradigm. Ludwin, whose clients include household names like Visa and Nasdaq, said he could understand why people saw a continued market for cybersecurity services, since his audience was full of people paid to worry about data breaches constantly. But their answers suggested they didn’t understand that the blockchain offered a solution. Unlike other system-design software, for which cybersecurity is an add-on, this technology “incorporates security by design,” he said.

It is unclear from the comments above exactly how a blockchain solves problems in the world of cybersecurity. Maybe it does. If so, then it should be explored in more detail than what is provided in this area of the book.

As an aside, I’m not sure how credible Ludwin’s comments on this matter are because of the multiple pivots that his companies have done over the past five years.11

On p. 45 they write:

A more radical solution is to embrace open, “permissionless” blockchains like Bitcoin and Ethereum, where there’s no central authority keeping track of who’s using the network.

This is very much a prescriptive pitch and not a descriptive analysis. Recommend changing some of the language in the next edition. Also, they should define what “open” means because there basically every mining pool doxxes themselves.

Furthermore, some exchanges that attempt to enforce their terms-of-service around KYC / AML / CTF do try to keep track of who is doing what on the network via tools from Chainalysis, Blockseer, Elliptic and others. Violating the ToS may result in account closures. Thus, ironically, the largest “permissioned” platforms are actually those on the edges of all cryptocurrencies.

See: What is Permissioned-on-Permissionless

On p. 45 they write:

It’s not about building a firewall up around a centralized pool of valuable data controlled by a trusted third party; rather the focus is on pushing control over information out to the edges of the network, to the people themselves, and on limiting the amount of identifying information that’s communicated publicly. Importantly, it’s also about making it prohibitively expensive for someone to try to steal valuable information.

This sounds all well and good, definitely noble goals. However in the cryptocurrency world, many exchanges and custodial wallets have been compromised and the victims have had very little recourse. Despite the fact that everyone is continually told not to store their private keys (coins) with an intermediary, Chainalysis found that in 2017 more than 80% of all transactions involved a third-party service.

On p. 45 they write:

Bitcoin’s core ledger has never been successfully attacked.

They should define what they mean by “attacked” because it has forked a number of times in its history. And a huge civil war took place resulting in multiple groups waging off-chain social media campaigns to promote their positions, resulting in one discrete group divorcing and another discrete group trying to prevent them from divorcing. Since there is only de facto and not de jure governance, who attacked who? Who were the victims?

On p. 45 they write:

Now, it will undoubtedly be a major challenge to get the institutions that until now have been entrusted with securing our data systems to let go and defer security to some decentralized network in which there is no identifiable authority to sue if something goes wrong. But doing so might just be the most important step they can take to improve data security. It will require them to think about security not as a function of superior encryption and other external protections, but in terms of economics, of making attacks so expensive that they’re not worth the effort.

This seems a bit repetitive with the previous couple of page, recommend slimming this down in the next edition. Also, there are several class action lawsuits underway (e.g., Ripple, Tezos) which do in fact attempt to identify specific individuals and corporations as being “authorities.” The Nano lawsuit also attempted to sue “core developers.”

On p. 46 they write:

A hacker could go after each device, try to steal the private key that’s used to initiate transactions on the decentralized network, and, if they’re lucky, get away with a few thousand dollars in bitcoin. But it’s far less lucrative and far more time-consuming than going after the rich target of a central server.

The ironic part of this is that generally speaking, the private keys controlling millions of bitcoins are being housed in trusted third parties / intermediaries right now. In some cases these are stored on a centralized server. In other cases, the cold wallet managed by hosting providers such as Xapo (which is rumored to secure $10 billion of bitcoin) does geographically split the keys apart into bunkers. Yet at some point those handling the mutli-sig do come together in order to move the coins to a hot wallet.12

On p. 47 they write:

It seems clear to us that the digital economy would benefit greatly from embracing the distributed trust architecture allowed by blockchains – whether it’s simply the data backups that a distributed system offers, or the more radical of an open system that’s protected by a high cost-to-payout ratio.

What does this mean? Are they saying to add proof-of-work to all types of distributed systems? It is only useful in the Bitcoin context in order to make it expensive to Sybil attack the network… because participants were originally unknown. Does that same problem exist in other environments that they are thinking of? More clarity should be added in the next edition.

On p. 48 they write:

The idea, one that’s also being pursued in different forms by startups such as Gem of Los Angeles and Blockchain Health of San Francisco, is that the patient has control over who sees their records.

This is one of the difficulties in writing a long-form book on this general topic right now: projects and companies frequently pivot.

For instance, a couple months after the book was published, Gem announced its “Universal Token Wallet,” a product which currently dominates its front page and social media accounts of the company. There have been no health care-related announcements from the company in over a year.

Similarly, Blockchain Health no longer exists. Its CEO left and joined Chia as a co-founder and the COO has joined the Neighborly team.

On p. 50 they write:

It was a jury-rigged solution that meant that the banking system, the centralized ledger-keeping solution with which society had solved the double-spend problem for five hundred years, would be awkwardly bolted onto the ostensibly decentralized Internet as its core trust infrastructure.

I think there are some legitimate complaints to made towards how online commerce evolved and currently exists but this seems a tad petty. As backwards as financial institutions are (rightly and wrongly) portrayed, it’s not like their decision makers sat around in the early ’90s trying to figure out how to make integrating the Web an awkward process.

On p. 50 they write:

Under this model, the banks charged merchants an interchange fee of around 3 percent to cover their anti-fraud costs, adding a hidden tax to the digital economy we all pay in the form of higher prices.

Again, like their statement above: there are some very legitimate gripes to be had regarding the existing oligopolistic payment systems, but this specific gripe is kind of petty.

Fraud exists and as a result someone has to pay for it. In the cryptocurrency world, there is no recourse because it is caveat emptor. In the world of courts and legal recourse, fees are levied to cover customer service including fraud and insurance. It may be possible to build a payment system in which there is legal recourse and simultaneously no oligopolistic rent seeking but this is not explored in the book. Also, for some reason the fee to miners is not brought up in this section, yet it is a real fee users must pay… yet they do not receive customer service as part of it.

Lastly, the Federal Reserve (and other central banks) monitor historical interchange fees. Not all users are charged the ~3% as mentioned in the book.

For instance (see below): Average Debit Card Interchange Fee by Payment Card Network

Source: Statista

On pages 52 and 53 they write uncritically about Marc Andresseen and VCs who have invested in Bitcoin and cryptocurrencies.

a16z, the venture firm co-founded by Andresseen, arguably has a few areas that may be conflicts-of-interest with the various coin-related projects it has invested in and/or promoted the past several years (e.g., investing in coins which are listed on an exchange they also are an investor and board member of such as 0x). Those ties are not scrutinized in a chapter that attempts to create a black and white narrative: that the legacy players are centralized rent-seekers and the VCs are not. When we know empirically that some VCs, including a16z, have invested in what they believe will become monopolies of some kind.

On page 54 and 55 they write about “Code is not law,” a topic that I have likewise publicly presented on.

Specifically they state:

One risk is that regulators, confused by all these outside-the-box concepts, will overreact to some bad news – potentially triggered by large-scale investors losses if and when the ICO bubble bursts and exposes a host of scams. The fear is that a new set of draconian catchall measures would suck the life out of innovation in this space or drive it offshore or underground. To be sure, institutions like the Washington-based Coin Center and the Digital Chamber of Commerce are doing their best to keep officials aware of the importance of keeping their respective jurisdictions competitive in what is now a global race to lead the world in financial technology.

This is word for word what coin lobbyists have been pitching to policy makers around the world for years. Both Coin Center and Digital Chamber of Commerce lobby on behalf of their sponsors and donors to prevent certain oversight on the cryptocurrency market.13 An entire book could probably be written about how specific people within coin lobbying organizations have attempted to white wash and spin the narrative around illicit usage, using carefully worded talking points. And they have been effective because these authors do not question the motivations and agenda these special interest groups have.

Either way, Bitcoin and many other cryptocurrencies were born in the “underground” and even “offshore.” It is unclear what the authors are trying to excuse because if anything, regulators and law enforcement have arguably been very light handed in the US and most regions abroad.

If anything, once a foreign registered ICO or coin is created, often the parent company and/or foundation opens an office to recruit developers in San Francisco, New York, and other US cities. I know this because all the multiple “blockchain” events I have attended overseas the past two years in which organizers explain their strategy. The next edition of this book could explore this phenomenon.

On p. 57 they write:

By The DAO founders’ own terms, the attacker had done nothing wrong, in other words. He or she had simply exploited one of its features.

Excellent point that should be explored in further detail in the next edition. For instance, in Bitcoin there have been multiple CVEs which if exploited (at least one was) could have resulted in changes in the money supply. Is that a feature or a bug?

And the most recent one, found in pre-0.16.3, was partially downplayed and hidden to prevent others from knowing the extent of potential damage that could have been done.

On p. 59 they write:

The dependence on a trusted middleman, some cryptocurrency purists would argue, overly compromises a blockchain’s security function, rending it unreliable. For that reason, some of them say, a blockchain is inappropriate for many non-currency applications. We, however, view it as a trade-off and believe there’s still plenty of value in recording ownership rights and transfers to digitally represented real-world assets in blockchains.

I think this whole section should be reworded to describe:

- what types of blockchains they had in mind?

- how the legal hooks into certain blockchains behave versus anarchic chains?

- being more precise with the term purist… do they mean maximalists or do they mean someone who points out that most proposed use-cases are chainwashing?

On pages 59 and 60 they write:

Permissioned blockchains – those which require some authorized entity to approve the computers that validate the blockchain – by definition more prone to gatekeeping controls, and therefore to the emergence monopoly or oligopoly powers, than the persmissionless ideal that Bitcoin represents. (We say “ideal” because, as we’ll discuss in the next chapter, there are also concerns that aspects of Bitcoin’s software program have encouraged an unwelcome concentration of ownership – flaws that developers are working to overcome.)

It would be beneficial in the next edition to at least walk through two different “permissioned blockchains” so the reader can get an idea of how validators become validators in these chains. By not including them, each platform is painted in the same light.

And because they are still comparing it with Bitcoin (which was designed for a completely different type of use-case than ‘permissioned chains’ are), keep in mind that the way mining (block making) is done in 2018 is very different than when it was first proposed in the 2008 paper. Back then, mining included a machine that did two things: validated blocks and also generate proofs-of-work. Today, those two functions are completely separate and because of the relatively fierce competition at generating hashes, there are real exit and entry costs to the market.

In many cases, this means that both the mining pool operators and hash generators end up connecting their real world government-issued identities with their on-chain activity (e.g., block validation). It may be a stretch to say that there is an outright monopoly in mining today, but there is a definite trend towards oligopoly in manufacturing, block producing, and hash generation the past several years. This is not explored beyond a superficial level in the book.

On p. 60 they write:

Until law changes, banks would face insurmountable legal and regulatory opposition, for example, to using a system like Bitcoin that relies on an algorithm randomly assigning responsibility at different stages of the bookkeeping process to different, unidentifiable computers around the world.

This is another asinine comment because they don’t explicitly say which laws they would like changed. The authors make it sound like the PFMIs are holding the world back when the opposite is completely true. These principals and best practices arose over time because of the systemic impact important financial market infrastructures could have on society as a whole.

Proof-of-work chains, the ones that are continually promoted in this book, have no ability to prevent forks, by design. Anarchic chains like Bitcoin and Ethereum can only provide probabilistic finality. Yet commercial best practices and courts around the world demands definitive settlement finality. Why should commerce be captured by pseudonymous, unaccountable validators maintained in jurisdictions in which legal recourse is difficult if not impossible?

On p. 60 they continue:

But that doesn’t mean that other companies don’t have a clear interest in reviewing how these permissioned networks are set up. Would a distributed ledger system that’s controlled by a consortium of the world’s biggest banking institutions be incentivized to act in the interest of the general public it serves? One can imagine the dangers of a “too-big-to-fail blockchain” massive institutions could once again hold us hostage to bailouts because of failures in the combined accounting system.

This has been one of Michael Casey’s talking points for the past three years. I was even on a panel with him in January 2016 in which he called R3 a “cartelchain,” months before Corda even existed. His justified disdain towards traditional financial institutions — and those involved with technology being developed in the “permissioned” world — pops up throughout this book. I do think there are some valid critiques of consortia and permissioned chains and even Corda, but those aren’t presented in this edition of the book.

He does make two valid observations here as well: regulated commerce should have oversight. That is one of the reasons why many of the organizations developing “permissioned blockchains” have plans to or already have created separate legal entities to be regulated as some type of FMI.

The other point is that we should attempt to move away from recreating TBTF and SIFI scenarios. Unfortunately in some cases, “permissioned chains” are being pitched as re-enabler of that very scenario. In contrast, dFMI is a model that attempts to move away from these highly intermediated infrastructures. See also my new article on SICNs.

On p. 60 they write:

Either way, it’s incumbent upon us to ensure that the control over the blockchains of the future is sufficiently representative of broad-based interests and needs so that they don’t just become vehicles for collusion and oligpolistic power by the old guard of finance.

The ironic part of this statement is — while well-intended — because of economies of scale there is an oligopoly or even monopoly in most PoW-mined coins. It is unclear how or why that would change in the future. In addition, with the entrance of Bakkt, ErisX, Fidelity and other large traditional financial organizations (e.g., the old guard) into the cryptocurrency world, it is hard to see how “permissionless ecosystems” can prevent them from participating.

On p. 61 they write:

As we stated in The Age of Cryptocurrency, Bitcoin was merely the first crack at using a distributed computing and decentralized ledger-keeping system to resolve the age-old problem of trust and achieve this open, low-cost architecture for intermediary-free global transactions.

But as the authors have stated elsewhere: proof-of-work chains are inherently costly. If they were cheap to maintain then they would be cheap to fork and reorg. You cannot simultaneously have a cheap (“efficient”) and secure PoW network… that’s a contradiction.

See:

- How much electricity is consumed by Bitcoin, Bitcoin Cash, Ethereum, Litecoin, and Monero?

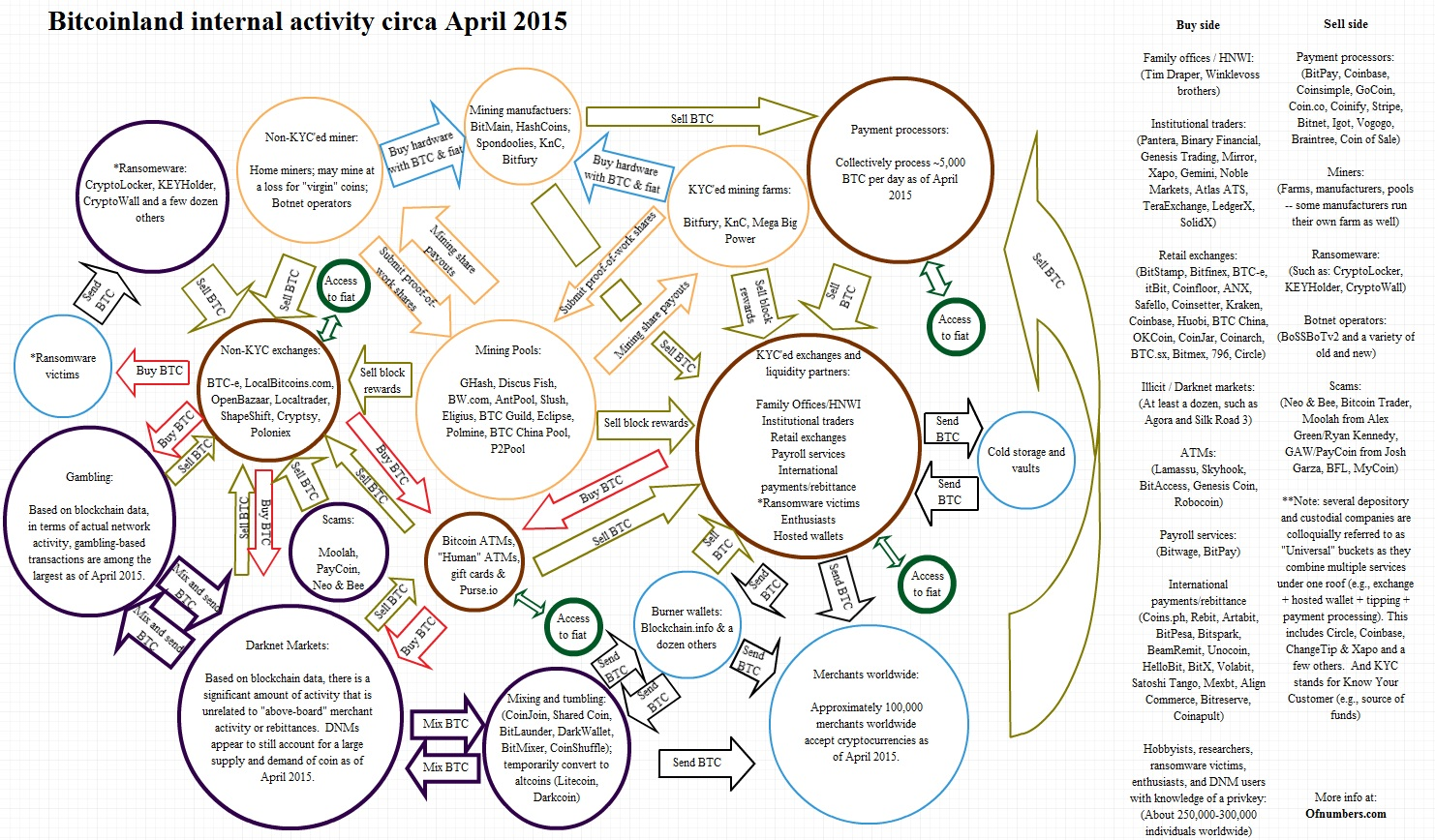

- The myth of a cheaper Bitcoin network: a note about transaction processing, currency conversion and Bitcoinland

Chapter 3

On pages 64 and 65 they provide a definition of a blockchain. I think this could be more helpful more earlier on in the book for newer audiences.

A few other citations readers may be interested in:

- While not a “blockchain” based on the definition of the authors, it could be worth referencing the ongoing work of Haber and Stornetta, see: The World’s Oldest Blockchain Has Been Hiding in the New York Times Since 1995

- Another detailed history covering the background of the pieces used by Satoshi can be found in Gwern Branwen’s article: Bitcoin-is-worse-is-better

- Arvind Narayanan and Jeremy Clark authored a good paper covering Bitcoin’s Academic Pedigree

On p. 66 they write:

That way, no authorizing entity could block, retract, or decide what gest entered into the ledger, making it censorship resistant.

Could be worth referencing Eligius, a pool run by Luke-Jr. that would not allow Satoshi Dice transactions because its owners religious views.14

On p. 67 they write:

These computers are known as “miners,” because in seeking to win the ten-minute payout, they engage in a kind of computational treasure hunt for digital gold.

I understand the need to make simple analogies but the digital gold one isn’t quite right because gold does not have an inflexible supply whereas bitcoin does. I’ve pointed this out in other book reviews and it bears repeating because of how the narrative of e-cash to HODLing has changed over the last few years.1516

Readers may be interested of a few real life examples of perfectly inelastic supplies.

On p. 67 they write:

Proof of work is expensive, because it chews up both electricity and processing power. That means that if a miner wants to seize majority control of the consensus system by adding more computing power, they would have to spend a lot of money doing so.

This is correct. Yet six pages earlier they say it is a “low-cost” infrastructure. Needs to be a little more consistent in this book. Either PoW is resource intensive or it is not, it cannot be both.

On p. 68 they write:

Over time, bitcoin mining has evolved into an industrial undertaking, with gigantic mining “farms” now dominating the network. Might those big players collude and undermine the ledger by combining resources? Perhaps, but there are also overwhelming disincentives for doing so. Among other considerations, a successful attack would significantly undermine the value of all the bitcoins the attacking miner owns. Either way, no one has managed to attack Bitcoin’s ledger in nine years. That unbroken record continues to reinforce belief in Bitcoin’s cost-and-incentive security system.

It’s worth pointing out that there are ways to fork Bitcoin beyond the singular Maginot Line attack. As mentioned above, Bitcoin and many other coins have forked; see this history. Hundreds of coins have died due to lack of interest by miners and developers.

It could also be argued that between 2015-2017, Bitcoin underwent a social, off-chain attack by multiple different groups attempting to exert their own influence and ideology onto the ecosystem. The end result was a permanent fracture, a divorce which the principal participants still lob social media bombs at one another. There isn’t enough room to discuss it here, but the astroturfing actions by specific people and companies in order to influence others is worth looking into as well. And it worked.

On p. 71 they write:

The caveat, of course, is that if bad actors do control more than 50 percent of the computing power they can produce the longest chain and so incorporate fraudulent transactions, which other miners will unwittingly treat as legitimate. Still, as we’ve explained, achieving that level of computing power is prohibitively expensive. It’s this combination of math and money that keeps Bitcoin secure.

I probably would change some of the wording because with proof-of-work chains (and basically any cryptocurrency), there are no terms of service or end user license agreement or SLA. At most there is only de facto governance and certainly not de jure.

What does that mean? It means that we really can’t say who the “bad actors” are since there is no service agreement. Barring an administrator, who is the legitimate authority in the anarchic world of cryptocurrencies? The original pitch was: if miners want to choose to build on another tree or fork, it’s their decision to do so… they don’t need anyone’s permission to validate blocks and attempt to update the chain as they want to. The next edition should explicitly say who or what is an attacker or what a fraudulent transaction is… these are points I’ve raised in other posts and book reviews.

Also, the authors mention that computational resources involved in PoW are “prohibitively expensive” here. So again, to be consistent they likely should remove “low-cost” in other places.

On p. 71 and 72 they write:

In solving the double-spend problem, Bitcoin did something else important: it magically created the concept of a “digital asset.” Previously, anything digital was too easily replicated to be regarded as a distinct piece of property, which is why digital products such as music and movies are typically sold with licensing and access rights rather than ownership. By making it impossible to replicate something of value – in this case bitcoins – Bitcoin broke this conventional wisdom. It created digital scarcity.

No it did not. This whole passage is wrong. As we have seen with forks and clones, there really is no such thing as this DRM-for-money narrative. This should be removed in the next edition.

Scarcity effectively means rivalrous, yet anyone can copy and clone any of these anarchic chains. PoW might make it relatively expensive to do a block reorg on one specific chain, but it does not really prevent someone from doing what they want with an identically cloned chain.

For instance, here is a list of 44 Bitcoin forked tokens that arose between August 2017 and May 2018. In light of the Bitcoin and Bitcoin Cash divorce, lobbying exchanges to recognize ticker symbols is also worth looking into in a future edition.

On p. 73 they write:

Many startups that were trying to build a business on top of Bitcoin, such as wallet providers and exchanges, were frustrated by an inability to process their customers’ transactions in a timely manner. “I’ve become a trusted third party,” complained Wences Casares, CEO of bitcoin wallet and custodial service Xapo. Casares was referring to the fact that too many of his firms’ transactions with its customers had to be processed “off-chain” on faith that Xapo would later settle the transaction on the Bitcoin blockchain.

This is one of the most honest statements in the book. The entire cryptocurrency ecosystem is now dominated by intermediaries.

Interestingly, Xapo moved its main office from Palo Alto to Switzerland days after Ripple was fined by FinCEN for violating the BSA. Was this just a coincidence?

On p. 73 they wrote:

Making blocks bigger would require more memory, which would make it even more expensive to operate a miner, critics pointed out. That could drive other prospective miners away, and leave Bitcoin mining even more concentrated among a few centralized players, raising the existential threat of collusion to undermine the ledger.

This wasn’t really the argument being made by the “small blockers.” Rather, it was disk space (not memory) that was — at the time — perceived as a limitation for retail (home) users in the long run. Yet it has been a moot point for both Bitcoin and Bitcoin Cash as the price per gigabyte for a hard drive continues to decline over time… and because in the past year, on-chain transactions on both chains have fallen from their peak in December 2017.

In practice, the “miners” that that authors refer to are the roughly 15 to 20 or so mining pools that in a given day, create the blocks that others build on. Nearly all of them maintain these nodes at a cloud provider. So there is already a lot of trust that takes place (e.g., AWS and Alibaba are trusted third parties). Because of economies of scale, spinning up a node (computer) in AWS is relatively inexpensive.

It really isn’t discussed much in the book, but the main argument throughout the 2nd half of 2017 was about UASF — a populist message which basically said miners (mining pools) didn’t really matter. Followers of this philosophy emphasized the need to run a node at home. For instance, if a UASF supporter based in rural Florida is attempting to run a node from his home, there could be a stark difference between the uptime and bandwidth capacity he has at home versus what AWS provides.

On p. 74 they write:

Without a tally of who’s who and who owns what, there was no way to gauge what the majority of the Bitcoin community, composed of users, businesses, investors, developers, and miners, wanted. And so, it all devolved into shouting matches on social media.

I wrote about this phenomenon in Appendix A in a paper published in November 2015. And what eventually happened was a series of off-chain Sybil attacks by several different tribes, but especially by promoters of UASF who spun up hundreds — thousands of nodes — and acted as if those mattered.

Future editions should also include a discussion on what took place at the Hong Kong roundtable, New York agreement, and other multilateral governance-related talks prior to the Bitcoin Cash fork.

On p. 74 they write:

A hard-fork-based software change thus poses a do-or-die decision for users on whether to upgrade or not. That’s bad enough for, say, word processing software, but for a currency it’s downright problematic. A bitcoin based on the old version could not be transferred to someone running software that support the new version. Two Bitcoins. Two versions of the truth.

The authors actually accidentally proved my earlier point: that public chains, specifically, proof-of-work chains, cannot prevent duplication or forks. Proof-of-work only makes it resource intensive to do double-spend on one specific chain.

This is one of the reasons why regulated financial organizations likely will continue to not issue long lifecycle instruments directly onto an anarchic chain like Bitcoin: because by design, PoW chains are forkable.

Also, future editions may want to modify this language because there are some counterarguments from folks like Vitalik Buterin that state: because hard forks are opt-in and thus lead to cleaner long-term outcomes (e.g., less technical debt).

On p. 75 they write a lot about Lightning Network, stating:

So, there are no miners’ fees to pay and no limit on how many transaction can be done at any time. The smart contracts prevent users from defrauding each other while the Bitcoin blockchain is used solely as a settlement layer, recording new balance transactions whenever a channel is opened or closed. It persists as the ultimate source of proof, a guarantee that all the “off-chain” Lightning transactions are legitimate.

What is not discussed in this edition is that:

- Lightning has been massively hyped with still relatively subdued traction

- Lightning is a separate network – it is not Bitcoin – and thus must be protected and secured through other non-mining means

- Lightning arguably distorts the potential transition to a fee-based Bitcoin network in much the same way that intermediaries like Coinbase do. That is to say, users are paying intermediaries the fees instead of miners thus prolonging the time that miners rely on block rewards (as a subsidy) instead of user fees.

Also, it bears mentioning that Bitcoin cannot in its current form act as a legal “settlement layer” as it cannot provide definitive settlement finality as outlined in the PFMIs (principle #8).

On p. 75 they write:

The SegWit/Lightning combination was in their minds the responsible way to make changes. They had a duty, they believed, to avoid big, disruptive codebase alterations and instead wanted to encourage innovators to develop applications that would augment the powers of the limited foundational code. It’s a classic, security-minded approach to protocol development: keep the core system at the bottom layer of the system simple, robust, and hard to change – some of the words “deliberately dumb” – and thus force innovation “up the stack” to the “application layer.” When it works you get the best of both worlds: security and innovation.

The authors should revise this because this is just repeating the talking points of specific Core developers, especially the last line.

Empirically it is possible to create a secure and “innovative” platform… and do so with multiple implementations of a specification. We see that in other cryptocurrencies and blockchain-related development efforts including Ethereum. The Bitcoin Core participants do not have a monopoly on what is or is not “security minded” and several of them are vocally opposed to supporting multiple implementations, in part, because of the politics around who controls the BIP process.

In fact, it could be argued that by insisting on the SegWit/Lightning approach, they caused a disruption because in point of fact, the amount of code that needed to be changed to increase the block size is arguably less than what was needed to build, verify, and release SegWit.

It’s not worth wading deep into these waters in this review, but the next edition of this book should be more even handed towards this schism.

On p. 76 they write:

But a group of miners with real clout was having none of it. Led by a Chinese company that both mined bitcoin and produced some of the most widely used mining equipment, this group was adamantly opposed to SegWit and Lightning. It’s not entirely clear what upset Jihan Wu, CEO of Bitmain, but after lining up with early Bitcoin investor and prominent libertarian Roger Ver, he launched a series of lobbying efforts to promote bigger blocks. One theory was that Bitmain worried that an “off-chain” Lightning solution would siphon away transaction fees that should be rightly going to miners; another was that because such payment channel transactions weren’t traceable as on-chain transactions, Chinese miners were worried that their government might shut them down. Bitmain’s reputation suffered a blow when revelations emerged that its popular Ant-miner mining rigs were being shipped to third-party miners with a “backdoor” that allowed the manufacturer-cum-miner to shut its opponents’ equipment down. Conspiracy theories abounded: Bitmain was planning to subvert SegWit. The company denied this and vowed to disable the feature. But trust was destroyed.

There is a lot of revisionism here.

But to start with, in the process of writing this review I reached out and contacted both Roger Ver and separately an advisor at Bitmain. Both told me that neither of the authors of this book had reached out to them for any comment. Why would the authors freely quote Bitcoin Core / SegWit developers to get their side of this debate but not reach out to speak with two prominent individuals from the other side to get their specific views? The next edition should either include these views and/or heavily revise this section of the book.

There are a few other problems with this passage.

Multiple different groups were actively lobbying and petitioning various influential figures (such as exchange operators) during this time period, not just Jihan and Roger. For instance, as mentioned above, the Hong Kong roundtable and New York agreement were two such examples. Conversely, SegWit and UASF was heavily promoted and lobbied by executives and affiliates at Blockstream and a handful of other organizations.

Regarding this “backdoor,” let’s rewind the clock and look at the overt / covert tempest in a teapot.

Last April Bitmain was alleged by Greg Maxwell (and the Antbleed campaign) of having maybe kinda sorta engaged in something called covert mining via Asicboost. Jimmy Song and others looked into it and said that there was no evidence covert was happening. At the time, some of the vocal self-identified “small block” supporters backing UASF, used this as evidence that Bitmain was a malicious Byzantine actor that must be purged from Bitcoinland. At the time, Greg proposed changing the PoW function in Bitcoin in order to prevent covert Asicboost from working.

In its defense, Bitmain stated that while Asicboost had been integrated into the mining equipment, it was never activated… partly because of the uncertain international IP / patent claims surrounding Asicboost. Recently, they announced a firmware upgrade that miners could activate overt Asicboost… a few days after another organization did (called “braiins”).

So why revisit this?

Two months ago Sia released code which specifically blocked mining equipment from Bitmain and Innosilicon. How and why this action is perceived as being fair or non-political is very confusing… they are definitely picking favorites (their own hardware). Certainly can’t claim to be sufficiently decentralized, right?

Yet in this section of the book, they don’t really touch on how key participants within the tribes and factions, represented at the time. Peruse both lists and look at all of the individuals at the roundtable that claim to represent “Bitcoin Core” in the governance process versus (the non-existent) reps from other implementations.

Even though the divorce is considered over, the tribes still fling mud at one another.

For example, one of the signatories of the HK roundtable, Adam Back, is still heckling Bitmain for supposedly not being involved in the BIP process. Wasn’t participation supposed to be “voluntary” and “permissionless”? Adam is also now fine with “overt” Asicboost today but wasn’t okay with it 18 months ago. What changed? Why was it supposedly bad for Bitmain to potentially use it back then but now it’s kosher because “braiins” (Slush) is doing it? That seems like favoritism.

Either way, the book passage above needs to be rewritten to include views from other camps and also to remove the still unproven conspiracy theories.

On p. 76 they write:

Meanwhile, original bitcoin went on a tear, rallying by more than 50 percent to a new high above $4,400 over a two-week period. The comparative performance of the pair suggested that small-block BTC and the SegWit reformers had won.

The next edition should change the wording because this comes across one-sided.

While an imperfect comparison, a more likely explanation is that of a Keynesian beauty contest. Most unsophisticated retail investors had heard of Bitcoin and hadn’t heard of Bitcoin Cash. Bitcoin (BTC) has brand recognition while Bitcoin Cash and the dozens of other Bitcoin-named forks and clones, did not.

Based on anecdotes, most coin speculators do not seem to care about the technical specifications of the coins they buy and typically keep the coins stored on an intermediary (such as an exchange) with the view that they can sell the coins later to someone else (e.g., “a greater fool“).

On p. 77 they write:

Bitcoin had gone through a ridiculous circus, one that many outsiders naturally assumed would hurt its reputation and undermine its support. Who wants such an ungovernable currency? Yet here was the original bitcoin surging to new heights and registering a staggering 650 percent gain in less than twelve months.

The problem with cherry picking price action dates is that, as seen in the passage above, it may not age well.17

For example, during the write-up of this review, the price of bitcoin declined from where it was a year ago (from over $10,000 then down to around $4,000). What does that mean? We can all guess what happened during this most recent bubble, but to act like non-tech savvy retail buyers bought bitcoin (BTC) because of SegWit is a non sequitur. No one but the tribalists in the civil war really cared.

On p. 77 they write:

Why? Well, for one, Bitcoin had proven itself resilient. Despite its civil war, its blockchain ledger remained intact. And, while it’s hard to see how the acrimony and bitterness was an advantage, the fact that it had proven so difficult to alter the code, to introduce a change to its monetary system, was seen by many as an important test of Bitcoin’s immutability.

There are a few issues here.

What do the authors mean by the “blockchain ledger remained intact”? I don’t think it was ever a question over whether or not copies of the Bitcoin blockchain (and/or forks thereof) would somehow be deleted. Might want to reword this in the future.

Segwit2x / Bitcoin Cash proponents were not trying to introduce a change to Bitcoin’s monetary system. The supply schedule of bitcoins would have stayed the same. The main issue was: a permanent block size increase from 1 MB to at least 2 MB. That proposal, if enacted, would not have changed the money supply.

What do the authors mean by “Bitcoin’s immutability”? The digital signatures are not being reversed or changed and that is what provides transactions the characteristic of “immutability.”

It is likely that the authors believe that a “hard fork” means that Bitcoin is not immutable. That seems to conflate “immutability” of a digital signature with finality (meaning irreversibility). By design, no proof-of-work coin can guarantee finality or irreversibility.

Also, Bitcoin had more than a dozen forks prior to the block size civil war.

On p. 77 and 78 they write:

Solid censorship resistance was, after all, a defining selling point for Bitcoin, the reason why some see the digital currency becoming a world reserve asset to replace the outdated, mutable, fiat-currency systems that still run the world. In fact, it could be argued that this failure to compromise and move forward, seen by outsiders as Bitcoin’s biggest flaw, might actually be its biggest feature. Like the simple, unchanging codebase of TCP/IP, the gridlocked politics of the Bitcoin protocol were imposing secure rigidity on the system and forcing innovation up the stack.

This is not what “censorship resistance” means in the context of Bitcoin. Censorship resistance is narrow and specific to what operators of miners could do. Specifically, the game theory behind Nakamoto Consensus is that it would be costly (resource intensive) for a malicious (Byzantine) actor to try and attempt to permanently censor transactions due to the amount of hashrate (proof-of-work) a Byzantine actor would need to control (e.g., more than 50%).

In contrast, what the authors described in this book was off-chain censorship, such as lobbying by various special interest groups at events, flamewars on Twitter, removing alternative views and voices on reddit, and via several other forms.

The “world reserve asset” is a loaded phrase that should be clarified in the next edition because the passage above comes across a bit like an Occupy Wall Street speech. It needs more of an explanation beyond the colorful one sentence it was given. Furthermore, as I predicted last year, cryptocurrencies continue to rely on the unit-of-account of “fiat systems” and shows no signs of letting up in this new era of “stablecoins.”

The authors definitely need to remove the part that says “unchanging codebase of TCP/IP” because this is not true. TCP/IP is a suite of protocol standards and its constituent implementations continue to evolve over time. There is no single monolithic codebase that lies unchanged since 1974 which is basically the takeaway from the passage above.18

In fact, several governing bodies such as IFTF and IAB continue to issue RFCs in order to help improve the quality-of-service of what we call the internet. It is also worth pointing out that their analogy is flawed for other reasons discussed in: Intranets and the Internet. In addition, the next version of HTTP won’t be using TCP.

As far as whether innovation will move “up the stack” remains to be seen but this seems to be an argument that the ends justify the means. If that is the case, that appears to open up a can of worms beyond the space for this review.

On p. 78 there is a typo: “BTH” instead of “BCH”

On p. 78 they write:

That’s what BTC, the original Bitcoin, promises with its depth of talent at Core and elsewhere. BTH can’t access such rich inventiveness because the community of money-focused bitcoin miners can’t attract the same kinds of passionate developers.

Strongly recommend removing this passage because it comes across as a one-sided marketing message rather than a balanced or neutral explanation using metrics. For instance, how active are the various code repositories for Bitcoin Core, Unlimited, and others? The next edition should attempt to measure how to measure “depth.”

For example, Bitmain has invested $50 million into a new fund focused on Bitcoin Cash called “Permissionless Ventures.” 2-3 years from now, what are the outcomes of that portfolio?

On p. 78 they write about permissioned blockchains:

Under these arrangements, some authority, such as a consortium of banks, choose which entities get to participate in the validation process. It is, in many respects, a step backward from Nakamoto’s achievement, since it makes the users of that permissioned system dependent once again, on the say-so of some trusted third party.

This is a common refrain throughout the book: that the true innovation was Bitcoin.

But it’s an apples-to-oranges comparison. Both worlds can and will co-exist because they were designed for different operating environments. Bitcoin cannot provide the same finality guarantees that “permissioned chains” attempt to do… because it was designed to be forkable. That’s not necessarily a flaw because Satoshi wasn’t trying to create a solution to a problem banks had. It’s okay to be different.

On p. 79 they write:

Most importantly, permissioned blockchains are more scalable than Bitcoin’s, at least for now, since their governance doesn’t depend upon the agreement of thousands of unidentified actors around the world; their members can simply agree to increase computing power whenever processing needs rise.

This doesn’t make sense at all. “Permissioned chains” in the broadest sense, do not use proof-of-work. As a result, there is no computational arms race. Not once have I been in a governance-related meeting involving banks in which they thought the solution to a governance-related issue was increasing or decreasing computational power. It is a non sequitur and should be removed in the next edition.

Also, there are plenty of governance issues involving “permissioned chains” — but those are typically tangential to the technical challenges and limitations around scaling a blockchain.

On p. 79 they write:

To us, permissionless systems pose the greatest opportunity. While there may well be great value in developing permissioned blockchains as an interim step toward a more open system, we believe permissionlessness and open access are ideals that we should strive for – notwithstanding the challenges exposed by Bitcoin’s “civil war.”

The authors repeat this statement in a couple other areas in the book and it doesn’t really make sense. Why? Because it is possible for both operating environments to co-exist. It doesn’t have to be us versus them. This is a false dichotomy.