[Note: this memo was written for the IIEL Issue Brief Series for Seminar on Sustainable De-Fi]

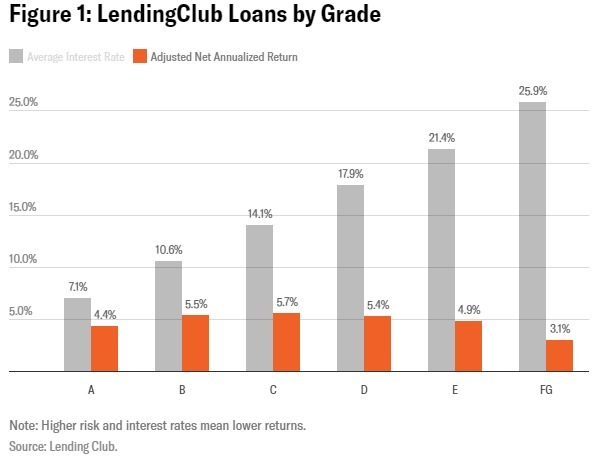

It’s been about six years since I began tracking the fintech space through my market research role at a couple of different firms. Fads have come and gone, a few have stayed. For instance, in the United States, P2P lending was all the rage in the early part of the last decade but has wasted away, despite a growing economy. In China, P2P lending became intertwined with the informal ‘shadow’ banking sector which not only blew up, but led to now notorious multi-billion dollar Ponzi schemes.

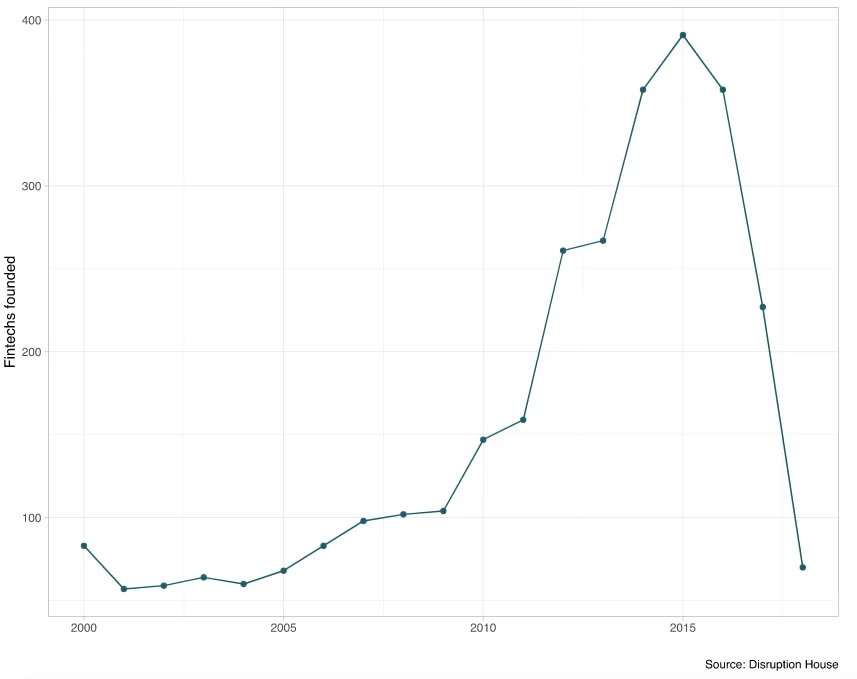

We can partially see this illustrated via The Disruption House (TDH), a data and benchmarking analytics firm focused on the financial sector, which found that some of the fintech exuberance peaked almost five years ago.

While this is not a fully comprehensive or exhaustive survey (TDH primarily focuses on wholesale capital markets), what has led to this particular decline? Part of it is unrealistic expectations that promoters failed to manage during the initial marketing phase… such as blockchains killing banks!

Another recurring issue is capital costs. Contrary to the narrative that a couple of bros with laptops in a Silicon Valley café can whip together an app that finally crushes too-big-to-fail banks, most, if not all of the fintech sectors require large capital investments to build out and eventually integrate Widget X, or Base Layer Y, into the existing financial infrastructure.

For example, last fall Apple humblebragged about its partnership with Goldman Sachs for the Apple Card, where on the one hand Apple tried to take credit for creating the product as a tech company but didn’t mention that Goldman also spent $300 million to develop it.

In response, Yakov Kofner, a managing partner at Gartner who focuses on payments and fintechs in general, mentioned last month that: “FSIs love to PR its Agile culture and open banking scale, but when it comes to launching a new product it somehow still requires hundreds-of-million budget and thousands of developers.”

Most startups, irrespective of geographic region, simply do not have the runway to build out these types of products, at least if we’re talking about apps with actual users and not mockups solely intended as Powerpoint viewership.

Another recurring issue is, even after launching a product, a lack of continued traction. Typically, a company that is actually experiencing real continual growth will boast specific metrics, milestones, and KPIs. But in the fintech world, we often see obfuscation:

In some corners of the financial press (like Alphaville), fintech became synonymous with simple user-interface facelifts, or at worst scams.

Despite this possibly cynical take, there are some bright spots of actual engagement. For instance, a couple weeks ago Zelle announced that it processed $56 billion in payments involving 230 million transactions during Q4 2019. This amounted to growth of 14% and 17%, quarter-over-quarter. Altogether they processed $187 billion in payments involving 743 million transactions in 2019. This amounted to growth of 57% and 72% year-over-year.

Yet according to a payments expert, Zelle may be double counting some send-receive volume and that growth is mostly legacy transfers moving to a new rail rather than some new payment use case or business model. In addition, in the United States, Venmo (and others including Square Cash) which is slowly catching up to Zelle in volume, arguably created a new use case, payment model, and improved customer experience (CX). Will these apps eventually vacuum in other features, pulling a reverse of what WeChat did over the years?

To be holistic, let’s look at some other relevant charts from other regions.

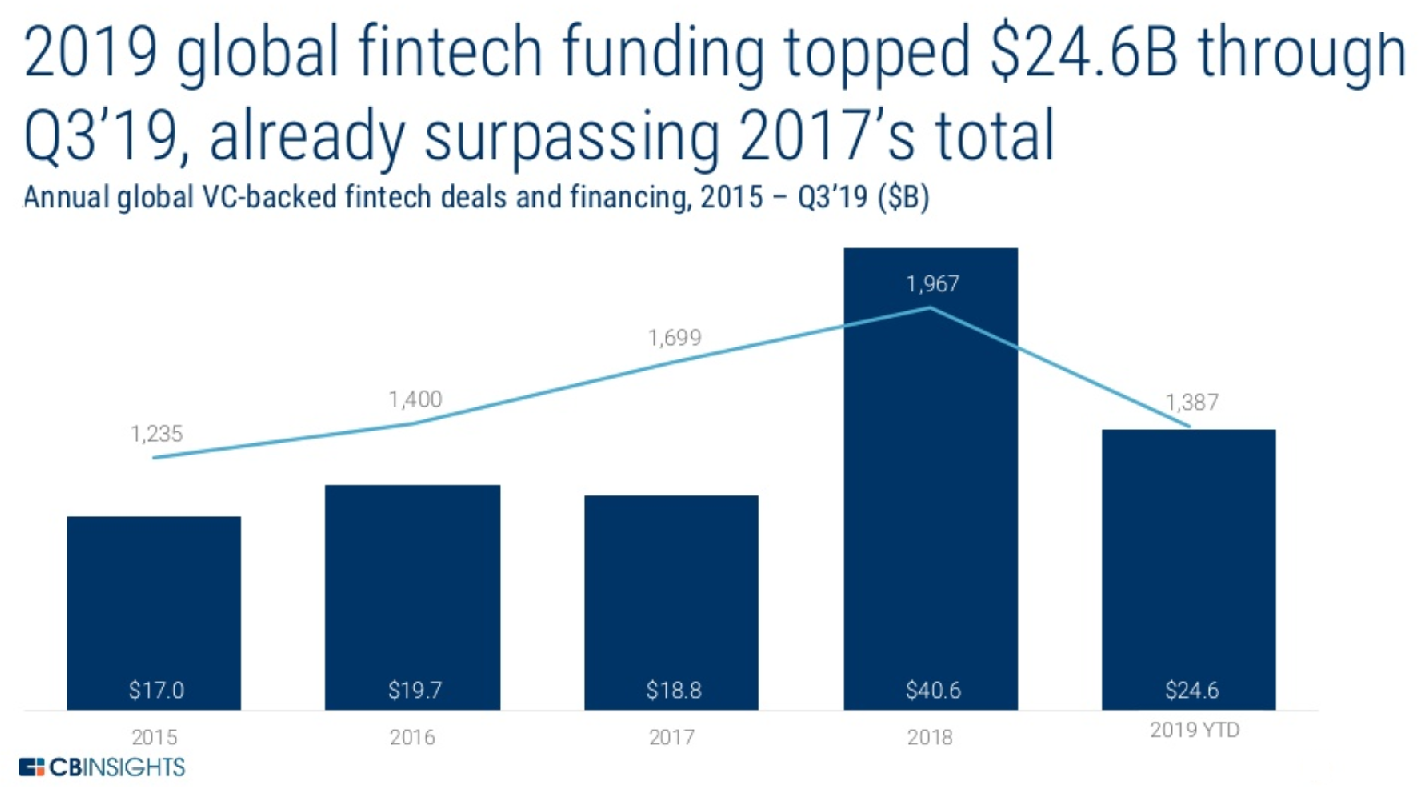

Source: CB Insights

CB Insights is an analytics company that, like TDH, tracks venture funding into startup ecosystems. In contrast to TDH, CBI saw increased activity globally in 2018, largely due to the Ant Financial raise. According to an analyst at CBI: “Fintech deals are down year over year, and the deals happening are at later stages.” Note: TDH looks narrowly at the European market whereas CBI’s remit is wider.

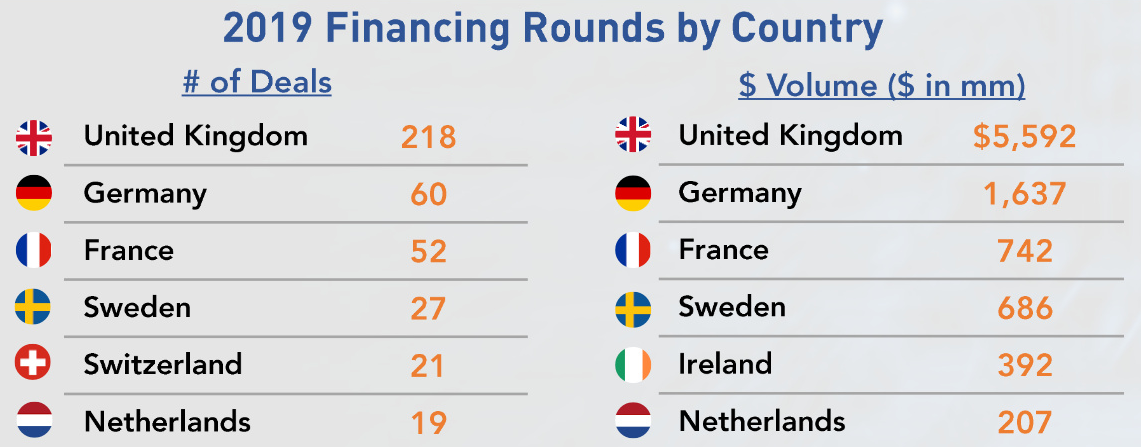

Lest we be accused of having an American-centric view (which obviously we do), FTPartners provided some already dated numbers… because the UK is no longer part of Europe as of a few days ago. Will Brexit impact local fundraising?

Source: FTPartners

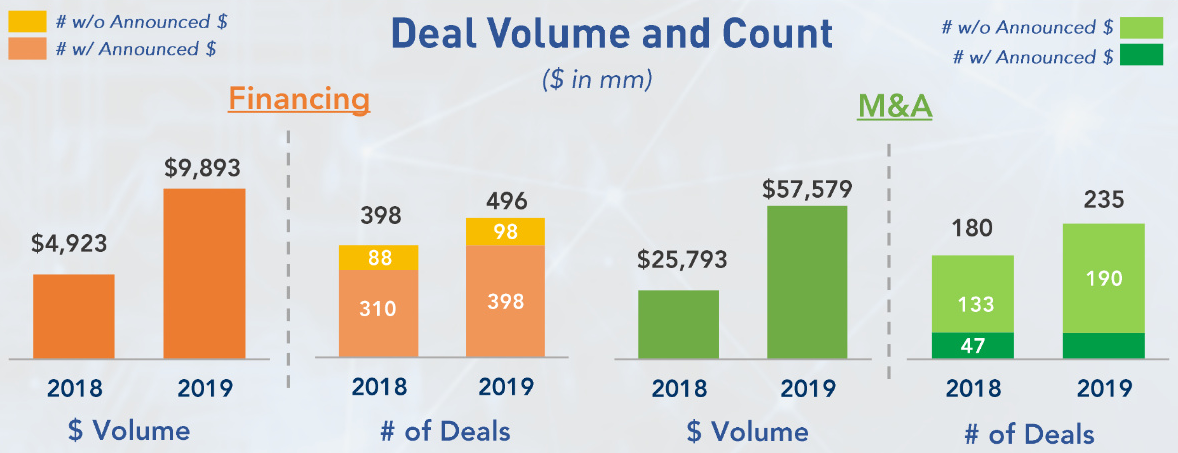

An easier way to visualize this is via colorized bar charts:

Source: FTPartners

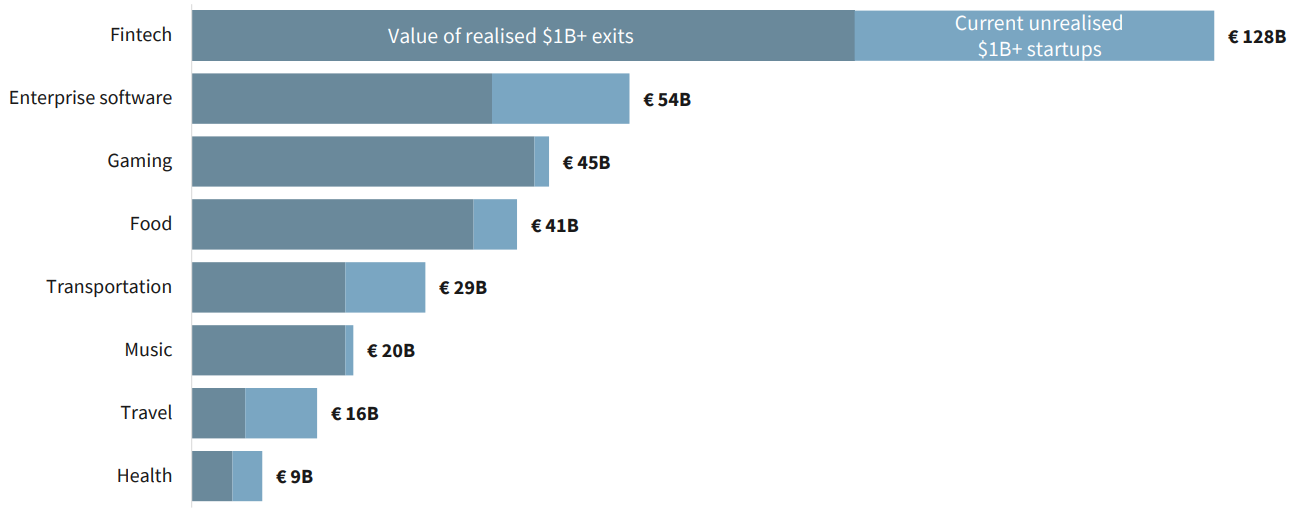

And how does European fintech deal activity compare to the rest of capital raises in other sectors throughout Europe?

Source: Dealroom

According to Dealroom, since 2013 fintech-related companies have “created over 2x more value than any tech sector in Europe.” That is interesting considering that venture rounds (and valuations) in Europe are often stereotyped as lagging their peers at the same stage in the United States.

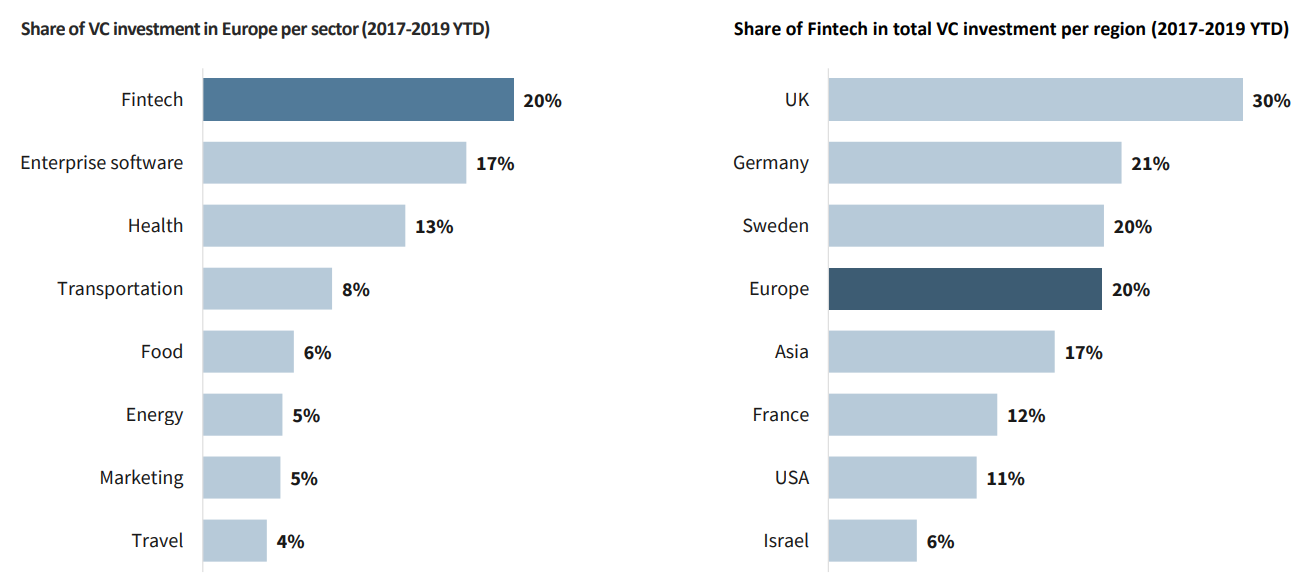

But as we see below, for the past few years, that stereotype appears incorrect.

Source: Dealroom

It bears mentioning that the Dealroom stats do not include biotech in health.

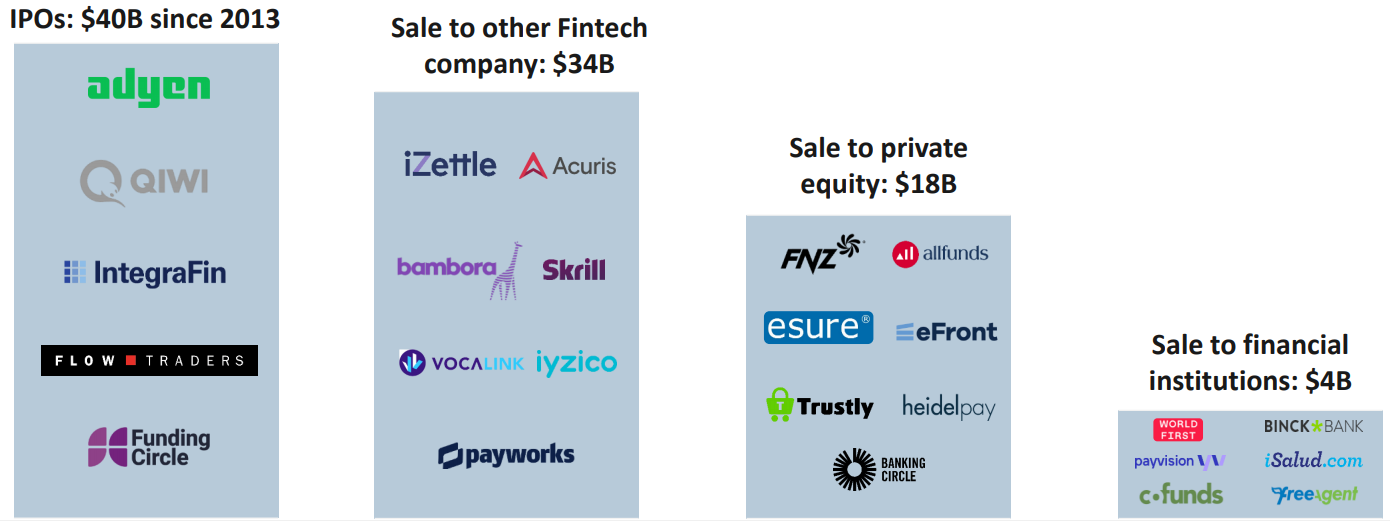

And what happens with these companies in the long-run? What’s the exit?

Source: Dealroom

According to Dealroom, traditional banks are not able to acquire their way into fintech because “they do not have the mandate as their valuation multiples are too low and synergies are likely limited. Instead, financial institutions and other corporates are more involved via partnerships or by investing in minority stakes.”

As someone who has previously worked for a company (R3) that became bank (majority) owned, I find it unusual that some of these companies aren’t fully acquired by a bank or two. But we’ve been told, especially in terms of lending platforms, that some banks – at least in the short run – have found it as an alternative source to try and generate revenue from. So maybe this is just an experimental era? It also bears mentioning that the track record of such acquisitions, or setting up captive fintech subsidiaries, is abysmal, with many ending up being shut down altogether.

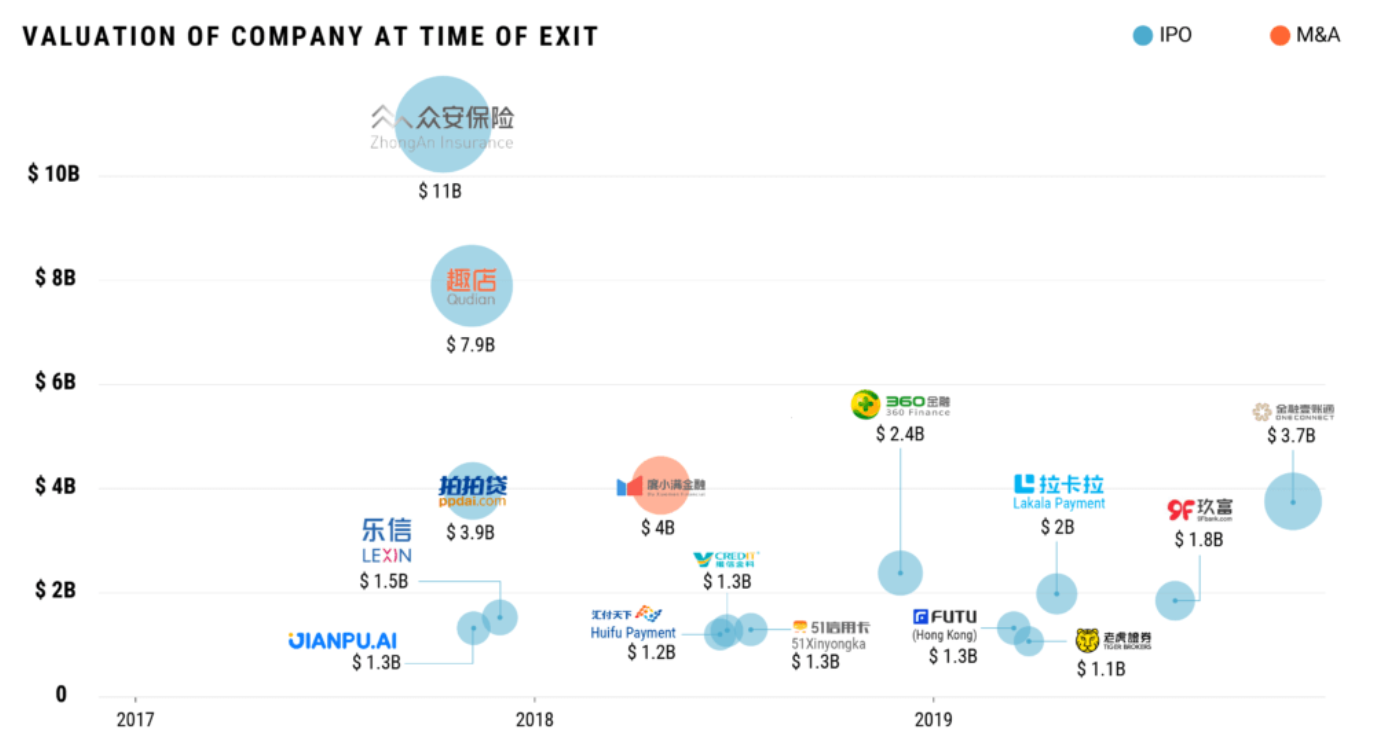

China is a touchstone today, more so than other times because of the ongoing coronavirus epidemic. This has also turned a bit personal as my wife is from northern China, as is our au pair. While we are all hoping for the best and for a speedy recovery, it is likely that deals and deal flow this year will look a lot different than they have in the past few years.

Source: CB Insights

Perhaps the most well known of the most recent exits (and coincidentally largest) is ZhongAn, an insurance company, who exited at an inflated valuation. How do we know? Because it has lost more than 60% from its peak after going public in late 2017.

We could, but won’t, go into the topic of P2P lending, but we’d like to give readers an idea of what happened aside from the aforementioned Ponzi schemes. According to the South China Morning Post: due to rampant fraud, all of China’s 427 remaining P2P lenders (from 6,000 back in 2015) will have to either close down within two years or become qualified small loan financial institutions.

Worth pointing out that this sector, P2P lending, meant the original fintechs before that word became popular. While they all started as P2P, they quickly pivoted to institutional capital. Many of them also promised incredible data insights by using social media feeds only to later default back to good old credit scores and cash flow analysis.

Does that mean all of the companies in the CBI chart above will suffer the same fate? No, but remaining grounded and realistic in the face of relentless positive press releases might be the balanced approach.

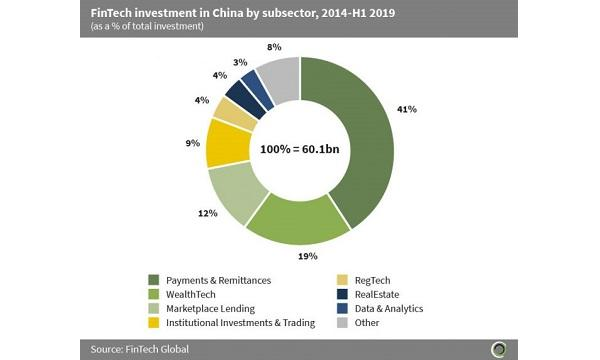

To round out this important region, let’s look at a larger breakdown.

Source: FinTech Global

According to FinTech Global, fintech investments between 2014-Q1 2019 in China reached a cumulative $60.1 billion. The largest aggregate was payment and remittances companies, which received $24.7 billion in funding. It’s also worth pointing out that one company, Ant Financial, distorts the overall number as it raised $14 billion in its series C and is currently valued in the private market at around $150 billion. Is this another WeWork valuation or a more legitimate Plaid valuation?

Conclusion

From the charts above it appears we are too early to say much other than the fintech world as a whole has a lot of work to do to deliver the claims it made to users. Capital seems ample but identifying legitimate operators, as in any sector, appears to be one of the largest ongoing challenges.

It is generally faux pas to add a new factoid in the conclusion of an article, but we’ll self-certify this exception.

Source: CBI

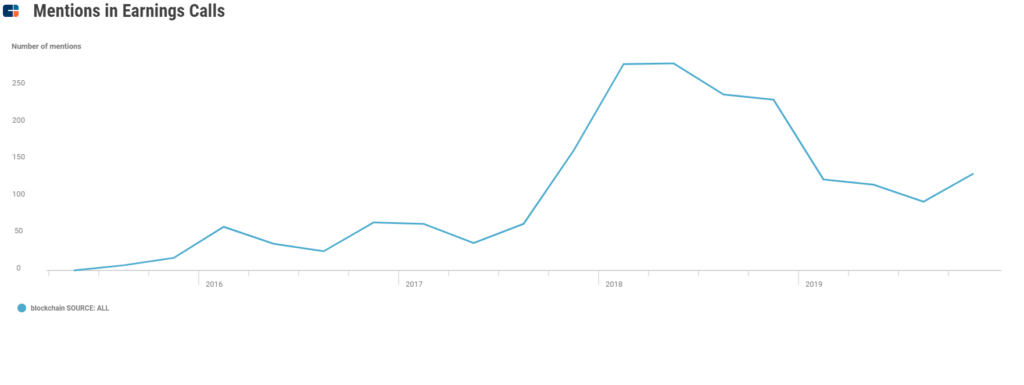

The spastic world of cryptocurrencies and blockchains arguably has yet to deliver on its ballyhooed promises beyond speculation, ransomware, and get-rich-quick schemes.

In aggregate, despite the billions in deals, as shown in the diagram above, there is a marked decrease in the word “blockchain” during earnings calls in 2019 compared to the previous year.

Why? Hype is subsiding. If we measure success based on user growth, increased revenue, and acquisitions (or public listings) we do not see much new activity outside the realm of mining, trading on exchanges, and throwing large conferences. And most activity targeting “the enterprise” is hovering around the relatively mundane documentation management and provenance arenas.

To be fair, there is a fundamental difference between conventional fintechs and the wild anarchic world of cryptocurrencies. There are definitely fintechs which brought massive value – and markedly improved CX – to businesses and consumers, including Lemonade, Next Insurance, and of course Ant Financial. Besides, valuations may not be the best measurement of the success of an industry.

Let’s follow-up in a couple of years to see what infrastructure is used and sustainable business models have silenced critics. Until then, a healthy dose of skepticism is warranted and seems justified in an era of anonymous twitter accounts reliably documenting… VCs congratulating themselves.