The past 6 months have seen an evolution of insanity to sanity. Just kidding!

One observation I have seen is that a few of the most vocal coin promoters have finally sat down and spoken with policy makers. Or rather, they finally started attending events in which policy makers, regulators, and decision makers at institutions speak at.

For those of us who have been attending and participating in regulatory-focused events for several years, the general messaging hasn’t changed that much: laws and regulations around financial market infrastructure and financial instruments exist for legitimately good reasons (e.g., systemic risks can be existential to society).

What has changed is that there are a few new faces from the coin world — most of which have previously pretended or perhaps did not even know that there is parallel world that can be engaged with.

It is still too early to see whether or not this governance education will be helpful in moderating their coin-focused excitement on social media but it seems to be the case that regulators and policy makers are still further ahead in their understanding of the coin world than vice versa. Maybe next year coin issuers and promoters will finally dive into the PFMIs which have been around since 2012.

Below are some of the activities I was involved and participated in.

[Note: this article was first published at FintechPolicy on November 2, 2018]

For self-serving reasons there has been an enormous amount of revisionism that Satoshi built Bitcoin in direct response to the Great Financial Crisis. But Satoshi explained that the coding for it began in mid-2007, which was months before any of the now notorious investment banks faced the brunt of the crisis or grappled with existential issues.

Either way, Bitcoin itself does not directly solve any problem that Lehman or Bear Sterns had, or for that matter, anything that mortgage loan originators had as well. The two behemoths did not collapse because of a payments (transactional) problem. Or a double-spending problem between pseudonymous participants. There wasn’t even a problem with digital signatures being reversed or some other strange technological edge case.

Instead it was a combination of many “off-chain” issues: lax lending standards, over leverage, unrealistic valuations, rubber stamp ratings, improperly assessed risk models, lack of proper documentation, special interests lobbying, imprudent oversight, and a laundry list of other culprits. None of those were things that Bitcoin itself could have fixed.

Perhaps hypothetically an industry-wide blockchain or some kind of commonly used distributed ledger could have maybe sorta helped with reducing reconciliations which could have maybe sorta lead to quicker identification of rehypothecation, but it is not accurate to say that a cryptocurrency like Bitcoin would have prevented the GFC. Let’s put that faux narrative to rest.

Garbage in, garbage out: blockchains cannot magically fix the underlying information — behind the representations — being inserted into blocks, that’s not what they are designed to ameliorate.

Pittsburgh

A year after Lehman collapsed, leaders from the G20 and several other international organizations met in Pittsburgh to reflect on and iron out additional methods of shoring up the decentralized yet highly concentrated and intermediated financial system. One of the decisions – potentially fatal in the long run – was to require that all standardized derivative contracts be cleared through what are known as central counterparties (CCPs), frequently referred to as clearing houses. Unlike exchanges, most CCPs are not common household names, but they are an order of magnitude systemically more important than even the largest of traditional exchanges.

Some of the older CCPs absorbed the additional derivative clearing routes and simultaneously new clearing houses were created around the world. Most legacy market infrastructure providers were welcoming to this new mandate as it meant additional business lines and fees. Regulators were also – at first – welcoming to this set of clearing requirements too because it meant that they could more easily observe and measure aggregate values and risks in just one or two physical places.

But being the bright reader you are, you are a step ahead and realize that the unseen consequence is that CCPs have actually created additional concentration of risk in a market with scarcely a few single points of trust. Some of these CCPs are to date, arguablyundercapitalized relative to the risks they bear. If even one of them collapsed, you probably would not have time to sell your magic internet coins on the KYC-less exchanges you love to use before the shockwaves reached it first.

But this article isn’t so much about traditional systemically important financial institutions and infrastructures so much as it is about the topic everyone reads fintech zines for: coin scuttlebutt.

Matryoshka Stablecoins

“Stablecoins” have become a catch-all term for a type of coin or token that is marketed as having parity with some kind of exogenous unit-of-account, typically the USD. In some cases the issuers are unlicensed e-money transmitters, although most market participants (traders) do not seem to care.

What problem are they solving and for whom? Is it for banks?

Probably not.

When speaking with banks about back-end payment issues, they do not lack general solutions either in-house or via 3rd party. From a compliance standpoint, some of their challenges are how to build solutions that satisfy AML regulations. One of the biggest unknowns about online-only money transmission businesses (e.g., PayPal, Transferwise) is whether they have not been in AML news because:

they are much better at building those solutions

because they are still small enough to stay under the radar

have been getting breaks by regulators and law enforcement

But regardless of fintech, the creation of a stablecoin doesn’t automatically improve AML surveillance by and for government agencies.

In fact, stablecoins as an aggregate may actually be expanding obfuscation of identity across borders because many exchanges, especially outside of the US, do not require stringent KYC, AML, and CTF checks.

The funny thing about the current mania around stablecoins is that a small group of us talked about and gestated their warts and all back in 2014 and 2015. For example, during that time Vitalik Buterin penned a comprehensive post on the topic and Robert Sams authored a short paper entitled “Seigniorage Shares” which a couple current stablecoin projects have unceremoniously cribbed on.

But the 50-odd proposals that are currently floating around in one form or fashion aren’t actual solutions to existential questions around intermediation and finality. At best, they are quick fixes to the desirability of reducing volatility whilst day trading in coin bucketshops. At worst, they create a new systemic risk to both cryptocurrency markets and traditional financial markets. And we know this because of who the credit risk is: commercial banks.

You see, contrary to the cartoonish explanations on cryptotwitter, today there is probably just one form of money: reserves sitting inside a central bank. Everything beyond coins and notes and money equivalents is arguably a credit risk.

Even a deposit made by companies into a commercial bank account ultimately bears the credit risk of that specific bank: it could collapse, force a haircut onto depositors, freeze assets at the request of the court, decide to shut down accounts, and at least a handful of other issues. We all witnessed the consequences of these risks first hand with the sorrowful collapse of retail and commercial banks during 2008 – 2009.

In contrast, the only potential stable form of currency within an economy is the one that a central bank issues and/or fully backs. But in order to access this today, you have to be an approved bank. On the wholesale side – with the advent of central bank digital currency (CBDC) and central bank digital account (CBDA) – who has access to these reserves could begin to include non-bank organizations and enterprises. It is unclear if or when a retail equivalent will exist, although several Narrow Bank proposals effectively provide roughly the same utility.

It is probably a little unfair to say that all cryptocurrency-focused venture funds would invest in a rope-making startup that could hang the entire economy so as long as they could get a quick exit. But it is clear that every VC firm that has invested in “stablecoins” is wanting to extract and privatize specific rents called seigniorage.

These VCs would like a healthy cut of the cash flow that a central bank would normally collect and remit to the national treasury which then pays for social services. In the case of VCs, it would flow through the management structure and then to the LPs who then would reinvest into increasingly cleverer sounding stablecoins. Just like Matryoshka dolls.

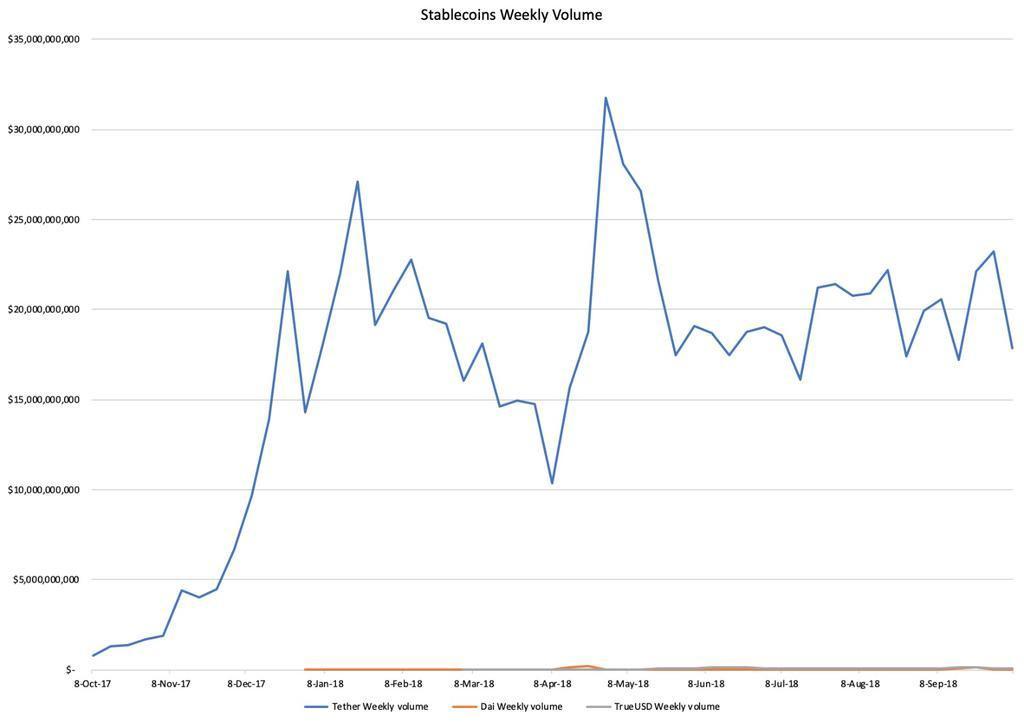

The line graph (above) represents a one year chart showing weekly exchange traded volume (measured in USD) of three stablecoins: Tether, Dai, and TrueUSD. Note: there are allegations that Tether’s volume are manipulated (e.g., trans-mining), but that is a conversation for a different article.

Too big to fail anarchic chains

If you are a developer or investor and you really wanted users to have access to stability without reintermediating the payment system, you should explore alternative platforms that have access to CBDCs, CBDAs, and Narrow Banks.

But that is annoyingly time consuming, right? Who wants to spend time sitting around with some fuddy duddy suits when you could be spinning up tokens with coinbros and “thought leaders” at coin festivals?

Last year I penned an accurate prediction of what would happen this year: the cryptocurrency world would become increasingly reliant on the unit-of-account of actual money, in this case, the USD.

We see this desirability for a stable U-o-A with the dozens of aforementioned stablecoins that have been concocted, some with the approval of state regulators. And all attempt to maintain parity of some kind relative to a traditional currency.

Consequently, we see the confluence of the problem highlighted in the section above, namely credit risk, with Tether (USDT). For those unfamiliar with Tether Ltd, it is a company that issues USDT which are – depending who you talk to at the company – supposedly pegged 1:1 to USD held in reserve somewhere. Ignoring the likelihood that they are not in full compliance with the BSA regime, Tether Ltd and its owner Bitfinex, keep losing access to commercial banks. Their accounts are shut down and as a result, the peg breaks because it is not a real peg.

While Tether currently trades at a credit discount arguably it still serves its original purposes (e.g., quasi-cash leg, tax free harbor for intra-day gains). But an ongoing issue is that the quality remains transparent to insiders and opaque to outsiders. Another issue is that aside from the lack of end-to-end KYC and AML surveillance, it really serves no purpose that couldn’t be better offered by collateral management solutions.

While everyone likes to claim that newer fully collateralized stablecoins that have been approved by state agencies are going to be better because they comply with BSA and BSA-equivalent surveillance requirements, this is untrue for at least two reasons:

The credit risk still involves commercial banks, not central banks (there is a difference).

If you have read my material in the past you probably think I sound like broken record. But consider that about half of the 50+ stablecoin proposals exist as ERC20 tokens on Ethereum. The remaining half piggy-back on top of Bitcoin or other anarchic cryptocurrency.

None of these chains are unforkable, by design. That is to say, they only provide probabilistic finality. And that presents an existential risk to not just the everyday user transmitting coins, but also any derivative – like stablecoins – that sits on top, reliant on a functioning unforked network below. This is not a new observation, I even wrote a lengthy paper about top-heavy issues three years ago. To put it another way: by design, block producers on these anarchic networks are rewarded an endogenous value (seigniorage) to secure the network. Adding ad hoc exogenous value atop of the network weakens and dilutes the overall security of a network which could lead to a compromise or fork.

At this point, if Bitcoin and other cryptocurrencies somehow disappeared, there will likely be no systemic impact because they do not yet have a large functioning ecosystem of derivative instruments and leverage behind it. So it is a bit of a moot point for now. But if the demand for stablecoins – which parasitically sit atop of anarchic chains – grew and expanded significantly to include credit, the chances of related 2008-like crisis within the cryptocurrency world would seem much higher. It is still a matter of debate as to how a cascading failure of these parasitic assets from a forked network would impact the traditional financial system.

Recall that for obvious reasons there is enormous amount of oversight for financial market infrastructures (FMI) like payment and clearing systems. If they ever achieve the critical size that VCs publicly claim they will, could cryptocurrencies such as Bitcoin that process and secure transactions for stablecoins eventually be considered systemically important and thus fall within that regulatory mandate?

According to the latest FSB report, Bitcoin and other “crypto-assets” do not pose risk to financial stability at this time. In the future, crypto-assets may pose risk to financial stability (see Appendix 1 of the report), but that would not, by itself, bring within scope of regulatory mandate. Obviously one critical issue with Bitcoin is – what jurisdiction does this fall within? ASIC in Australia is already developing an approach that touches on this.

In the event that occurs, this could turn these anarchic networks into expensive chimeras, permissioned-on-permissionless chains. But that is a topic for a different article.

Conclusions

Cryptocurrency promoters often speak nostalgically of how the Great Satoshi solved a sundry of computer science and economic problems on Halloween 2008. But on closer examination, Satoshi proposed one way of transmitting e-cash and bypass existing payment providers without having to comply with the BSA-regime.

When she disappeared in late 2010, the cryptocurrency world up to that point was still relatively disintermediated and decentralized. There were a couple of semi-pro mining pools and deposit-taking exchanges as well as a few custodial wallets, nearly all of which got hacked and pilfered.

Those first victims had no legal recourse and probably didn’t care enough at the time to sue anyone because just about everyone playing around with Bitcoin and its clones understood that there were no terms of service or end user licensing agreements, it was (and is) caveat emptor.

Fast forward 10 years and what is commonly referred to as the “cryptocurrency space” is heavily intermediated. The vast majority (80%) of all transactions last year flowed through some kind of third party. Nearly everyone hedges their trading positions in just a couple of underregulated exchanges. And it is rumored that the main reason the largest off-shore exchanges have not been shut down is because of the access they provide to certain law enforcement agencies regarding suspicious accounts involved in illicit activities.

In other words, while Satoshi had attempted to create an alternative payment system, her followers have not only recreated the same concentration of risk and intermediation as the financial world she apparently wasn’t a fan of, but this new one lacks nearly all of the safeguards, accountability, recourse, and broad oversight that civilization has collectively placed on SIFIs.

The Black Mirror episode we live in today is even more strange and perverse once you account for:

the environmental toll, the negative externality that proof-of-work mining creates… where seigniorage gains are privatized and the degradation is socialized

the same nouveau riche coinbros and broettes who enriched themselves off unsophisticated retail investors by publicly shilling and flipping ICOs last year are now funding more than a handful of coin lobbying organizations to convince regulators to keep their statist hands out of this highly centralized yet opaque market

Creating systemically important cryptocurrency networks is likely the most ironic phenomenon to have arisen from an anarchic experiment started on a mailing list ten years ago. Yet here we are.

If you are interested in participating in something that doesn’t merely enrich existing coin holders at the expense of society and the environment, highly recommend reading Ray Dillinger’s recent interview and also looking into dFMI. And then circle back to the CBDC report from the BIS this past March.