Recently the Museum of American Finance hosted an event covering Bitcoin. One of the panelists allegedly said: “we don’t think about infrastructure cost of VOIP because it’s approaching zero.”

I haven’t seen a video, so it’s unclear if this is a summation of their thoughts. But in terms of the infrastructure costs of Bitcoin, this is probably not comparing apples to apples because the incentives and costs to successfully attack the Skype network are very different than a network such as Bitcoin.

If the cost to maintain Bitcoin’s infrastructure is zero, so too is the cost to successfully attack and fork it. In fact, just about anyone motivated to do so could have successfully “attacked” (e.g., double spent or do a block reorg) the Bitcoin network in its first 18 months because the hashrate was relatively low because the value of the token was negligible (e.g., miners weren’t consuming additional units of capital because there was no financial incentive to do so).

For example, by the end of June 2010, the network strength (detailed here) was around 139 megahashes/second. To obtain half that hashrate, or 70 megahashes/second, an attacker would need to only spin up about 10 Xeon processors which could be obtained through AWS relatively cheaply (note: Satoshi probably used just one computer).

It was not until market participants increasingly valued the coin (vis-à-vis higher demand) which then in turn incentivized miners to destroy a corresponding amount of capital to protect the ledger. Or as one developer recently explained: the maximum cost to successfully attack Bitcoin’s network is directly proportional to the market value of the token. It is intentionally designed to be expensive to attack otherwise anyone could change the history. Or as Richard Brown has explained, proof of work as used in Bitcoin is “inefficient” on purpose.

The logistics of currency positions

In practice miners are taking one currency (USD, EUR, RMB), usually one denominated based on where the equipment is located, and through the process of destroying exergy (see Chapter 3), converting it into a foreign currency called bitcoin. Or in other words, miners are currency convertors. And irrespective of scale, “to mine” is effectively taking a long position on bitcoin versus a fiat currency (recall that the mining equipment and operating costs are paid for in foreign currency). For many actors, it is not just a forex bet but also a gamble on appreciation. As discussed in Chapter 3, there are at least two classes of actors willing and able to mine at losses, including some who hope that the token will appreciate in value.

I, along with several others, have written about this numerous times. In the long run, most miners, if not all, do not actually generate economic profit because of how the difficulty rating adjusts proportional to the amount of hashrate that is added to the network (e.g., the “Red Queen effect”). If it becomes cheaper to “mine” then the situation will simply incentivize more hashrate to be added resulting in a higher difficulty rating, negating the temporary advantage. In the short run, there are actual differences in margins due to differences in climate, electricity prices, administrative overhead, taxes, etc. Some, such as BitFury and a few in China, have better economies of scale and/or handsome land and energy deals due to guanxi (a few consequently have “cost of production” down to $80 per bitcoin and even lower as of this writing).

How the sausage is made

Unless you have mined some kind of coin before (see 12 Step Guide), in order to understand how mining actually works we must begin by noting that most miners are not actual miners, but rather hashers who effectively ‘rent’ their equipment to pools (pools charge a fee in exchange for this service). Miners, technically speaking, are the machines that actually select, process and validate a transaction. Hashing equipment does not do this.

For instance, CoinTelegraph recently ran a story on the new Raspberry Pi 2 Model B which costs $35.

This Pi computer (above) is effectively the only miner, the only “transaction processing” machine in an entire mining warehouse.

Since the entire Bitcoin blockchain can and is processed with something this cheap, why is mining so expensive then?

That is where Sybil protection and decentralization come into play. Recall that for the supply side of the equation, miners compete with one another to win the block reward (since it accounts for roughly 99.5% of their revenue, a figure which hasn’t changed much in a couple years, see below for more). Thus, rationally economic actors will strip a mining facility of anything that lacks utility (in some cases, even computer “cases” themselves). If it is not hashing, it is not helping to generate income. Thus in all warehouses today, they have row after row of specialized machines called ASICs to provide this spartan hashing function (recall this was all initially spurred on by ArtForz creativity). In practice, this hashing equipment actually just asks for a block header from the host node of a pool (such as the Pi Raspberry) and only “hashes” the “midstate” but that is another discussion entirely (see this excellent explanation from Vitalik Buterin). Thus, the only bona fide “mining” equipment in a facility is usually something akin to the Pi computer above.

[Sidebar: whenever someone claims that Bitcoin mining manufacturing pushed fabrication geometries to new limits, the reality is that designing a mining chip (or really, hashing chip) is actually, relatively simple: you only need a small handful of engineers to do it compared with say, a Xeon chip (which requires several hundred). In fact, most of the IP for SHA256 modules (or tiles) for “mining” equipment can be purchased from existing backend design companies.]

So what utility do those rows of ASICs provide then?

As shown in the video (above), the sole job of those single-use ASIC machines are to provide “proof of work” hashing power which thereupon provides Sybil protection for the blockchain. The video above was filmed in Liaoning province in China last fall by Vice magazine. Be sure to also read more details from Jake Smith’s article covering the same facility (he was also the laowai translating in the video).

The bigger picture

Recall that the estimated total deployed capital from VC firms over the past 18 months in the Bitcoin space is roughly $500 million into over 100 startups. And the direct financial rewards to miners over the same time frame has been roughly $780 million (3,600 bitcoins x 540 days x $400 weighted token price). This wealth transfer represents a large opportunity cost to the emerging economy that is Bitcoinland (one notable exception is BitFury, which invested in BitGo). Because instead of being able to hire software developers with that $780 million, it was used to fund exergy dissipation through:

- Semiconductor firms such as TSMC

- Utility companies (coal power plants in China, facilities in Washington, Finland and Ukraine)

- Property and real estate agencies

Or in short, in an alternate universe in which Satoshi had created a different distributed yet secure consensus protocol (one that may or may not exist) in which the infrastructure costs did not directly scale in proportion to the value of the token, $780 million could have been instead used to hire 7,800 full-time developers (based on SF Bay wages).

But the Bitcoin network doesn’t need those developers, the current network can do everything the incumbents provide right?

Based on at least one post, Satoshi may have hoped to compete with Visa but he/she could turn out to be empirically wrong, there are real costs to maintaining a decentralized network. As it stands today, the Bitcoin protocol does not offer any of the actual banking and credit services of existing financial institutions. Consequently, recall that the expenditure and threat models on ‘trusted’ centralized networks are different than ‘untrusted’ decentralized networks. As I and others have described elsewhere, Sybil protection and decentralization add costs to operating a network — they do not in fact, make it cheaper. There is no free lunch or “free energy” in the mining process, anyone claiming that proof-of-work-based “mining” will somehow become ‘cheaper’ in the future is in the same class as the perpetual motion salesman.

Why is this important?

Another way to think about it: the $500 million that VC’s have deployed to build Bitcoinland are effectively a foreign exchange currency play (because it is a virtual-only foreign country that can only be accessed with a pre-paid card, bitcoin). This money is being paid to effectively leverage one economy, or rather one unit-of-account (namely USD, EUR, RMB) to build a virtual unit-of-account called BTC (see more from Robert Sams). But, and this is important for international adoption: there are no real corresponding exports from that economy (yet). Furthermore, there are several reasons why the narrative of social media enthusiasts will likely not go according to plan.

Bitcoinland – a large, virtual retirement facility

From a network sustainability perspective, Bitcoinland is a senior citizen and its trust fund (revenue base) is no longer in the “early days.”

From a network sustainability perspective, Bitcoinland is a senior citizen and its trust fund (revenue base) is no longer in the “early days.”

Investor and entrepreneur interest may still be in the “early days,” but the asymptotical reward structure rapidly aged this economy into its twilight years much like early stars.

As of this writing, approximately 13.8 million bitcoins have been divvied out to miners over the past 6 years. This represents roughly 2/3 of the internal income the Bitcoin trust fund had at the beginning. More than half of the remaining will be apportioned in the next five and half years.

One common refrain is that at some unknown date and time, transaction fees will somehow increase and/or more users will collectively pay more fees. This is a possibility but is unlikely for the reasons discussed on numerous occasions for reasons described in this working paper (it is a type of collective action problem).

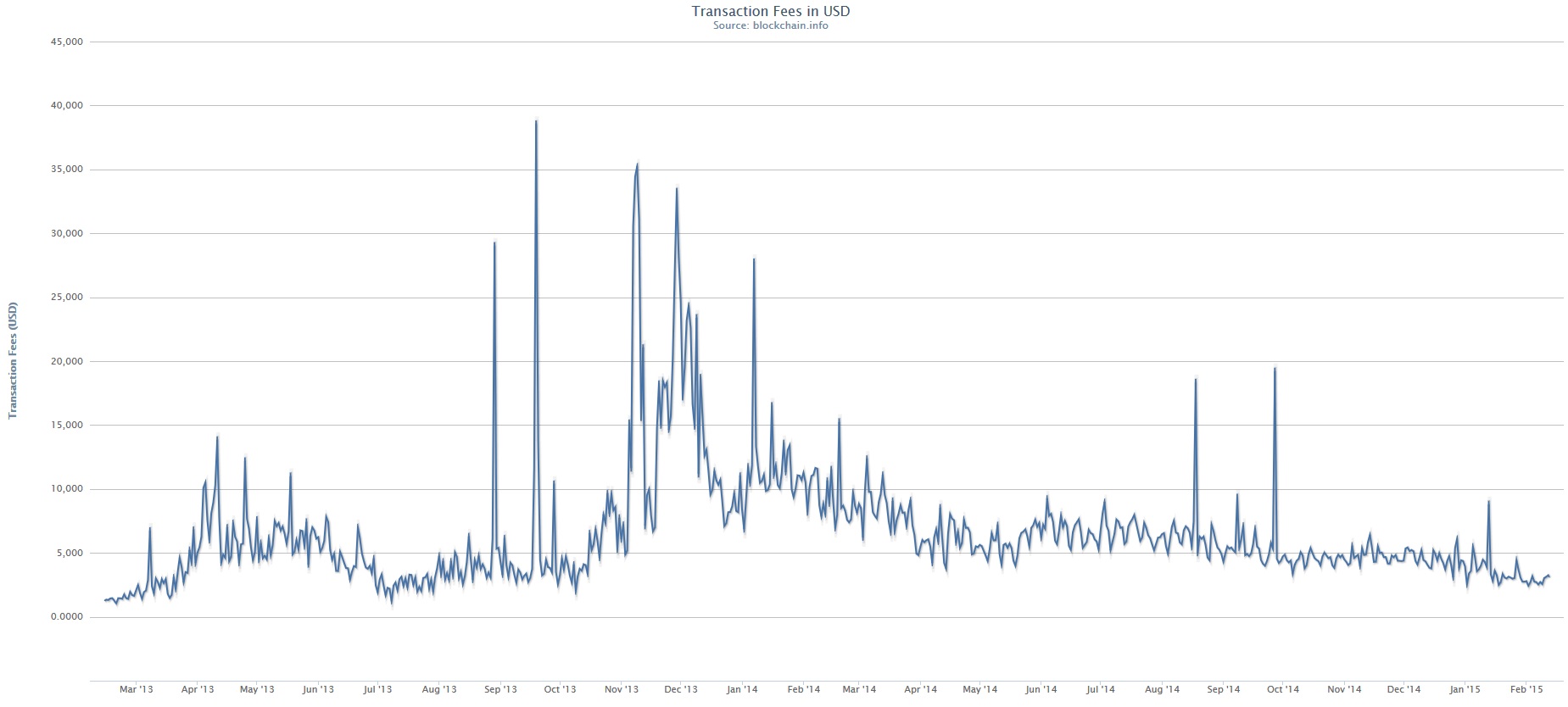

In fact, the biggest counterpoint to this is that we have direct evidence to the contrary.

The chart (above) illustrates the total transaction fees to miners (denominated in USD) over the past 2 years. Denominated in BTC, the 2 year chart shows the same trend line.

{kind=link}

Fees to miners is actually at a 2 year low (in BTC) and not increasing despite the fact that there are now more than 100,000 merchants that accept bitcoin for payments (up from 20,000 last year).

Why is merchant adoption far outpacing consumer adoption? Well there are multiple reasons which I and others have discussed before. More on that later.

Perhaps there is another way to visualize this historically, from the beginning?

The chart (above) is from Organ of Corti and illustrates what I mentioned at the start of this post: that roughly 0.5% of a miner’s revenue comes from transactions (effectively, user donations), the vast majority still comes from the block reward.

But isn’t the retail economy booming and will balance this out? No.

As shown from Jorge Stolfi (and Coinbase’s own chart), on-chain retail growth is stagnant (in fact, it is one of the glaring omissions in Bitpay’s new infographic).

Why? Because most consumers are, in practice, not incentivized or otherwise interested in converting their local currency into a foreign currency for goods or services they can already buy with their existing currency. Endless threads on social media have proposed solutions to this inertia, but the fact of the matter is in practice, consumers are only willing to change if and when the alternative is not just as useful, but significantly so (there is an entire segment of economics that studies consumer choice and indifference curves). And they are only going to use something if it provides them more utility. Thus to them, entering Bitcoinland (and current cryptocurrencies in general) is a friction they have preferred to avoid. Perhaps that will change, but then again, maybe not.

Again, recall that the primary utility provided by the Bitcoin blockchain was to circumvent trusted third parties (TTP), which in practice, the average consumer are okay with having to deal with (the tradeoff between less privacy for more insurance, etc.). For instance, in terms of demographics, the vast majority of gamblers that use bitcoin are based in the US because online gambling is illegal here. European gamblers typically use bank transfers. When SatoshiDice blocked US-based IPs, gambling volume dropped significantly for them (and flowed to other similar sites). Maybe there will be another “killer app” but then again, maybe blockchains in general attract illicit activities because their decentralized nature enables routing around TTP, which some bitcoin holders find useful and attractive.

Circular flow of income

One last issue that intersects with miners and the Bitcoinland consumer economy is that of volatility. This is a topic that generates enormous reaction and I am aware of companies such as Bitwage, Hedgy, Teraexchange that are attempting to create either hedging mechanisms against volatility and/or bridges between two different unit-of-accounts.

Ignoring the impact of the Poisson process, there is never a dull moment for being a cryptocurrency miner (professional or otherwise) as you never have a really good idea of how much capital to deploy in the future due largely to the continuous uncertainty over what the future market price of a coin is and what the difficulty rating may adjust to. Or as Robert Sams aptly noted:

It is the nature of markets to push expectations about the future into current prices. Deterministic money supply combined with uncertain future money demand conspire to make the market price of a coin a sort of prediction market on its own future adoption. Since rates of future adoption are highly uncertain, high volatility is inevitable, as expectations wax and wane with coin-related news, and the coin market rationalises high expected returns with high volatility (no free lunch).

Yanis Varoufakis, the new finance minister for Greece, has written about the monetary supply schedule challenges within Bitcoin several times. One notable quote he had last year involved how speculative demand for bitcoin outstrips transactional demand:

“By a long mile. Bitcoin transactions don’t go beyond the first transaction. The people who have accepted bitcoins don’t use them to buy something else. It gets back to the circular flow of income. When Starbucks not only accepts bitcoins but pays their workers in bitcoins and pays their suppliers in bitcoins, when you go back four of five stages of productions using bitcoin, then bitcoin will have made it. But that isn’t happening now and I don’t think that will happen.” Because it isn’t happening now, he continues, and because so many more people are speculating on bitcoin rather than transacting with it, “Volatility will remain huge and will deter those who might have wanted to enter the bitcoin economy as users, as opposed to speculators. Thus, just as bad money drives out good money, Gresham’s famous law, speculative demand for bitcoins drives out transactional demand for it.”

What this has looked like in practice is that miners themselves are creating a currency with which they are not necessarily able to pay their electricity bills or leases with. They have to convert it. Perhaps this will change, but since the bulk of this virtual currency has to be converted into a foreign currency (USD, EUR, RMB), it creates continuous sell-side pressure on the market (see How do Bitcoin payment processors work?). And without a corresponding increase in demand from those holding foreign currency, the market price declines.

Hedging may help mitigate some losses for a few of the merchants that choose to keep and not convert bitcoin payments they receive, but again, hedging isn’t free. It also costs someone something to do — hedging can be expensive, this is why corporates do not typically hedge against ongoing foreign revenue but they only hedge against large one-off items (such as acquisitions, or large shipments / purchases). Just ask the airline industry about its fuel hedging strategies. Recall again that consumers in general prefer stable purchasing power for medium’s-of-exchange (no one is trying to directly use petroleum as a currency).

Without a circular flow of income, this is unlikely to change and this is something that requires years, perhaps even decades to build even with dynamically adjusted, elastic money supplies. For instance, recall even with its $9.5 trillion economy and its $2 trillion in exports, the RMB only represents 2.17% of all international trade settlements (for comparison, the Greeks exported €27 billion in goods and services in 2013). Perhaps indeed, Bitcoinland is still in the “early days” — or maybe its fixed monetary supply has inflicted it with incurable progeria (i.e., few want to spend it, so not enough fees to replace the block reward). And thus its main exports will continue to be ways to distribute exergy via currency conversion processes and illicit trade.

Is all lost?

Earlier this week William Mougayar encouraged advocates in this nascent space to basically chill out with the moon rhetoric. Again, it is impossible to know what consumers will eventually adopt. Anyone claiming that there will just be “one winner” that encompasses all use-cases is probably wrong in the short run (note that Richard Brown and Meher Roy have suggested that there may be some kind of “Grand Unified Theory” of cryptofinance but that is a topic for another post).

Earlier this week William Mougayar encouraged advocates in this nascent space to basically chill out with the moon rhetoric. Again, it is impossible to know what consumers will eventually adopt. Anyone claiming that there will just be “one winner” that encompasses all use-cases is probably wrong in the short run (note that Richard Brown and Meher Roy have suggested that there may be some kind of “Grand Unified Theory” of cryptofinance but that is a topic for another post).

Every business, institution and customer has different wants and needs that will dictate actual adoption of technology and not the other way around. Entrepreneurs, developers and investors cannot assume a market will adopt their own narrative any more than shipwreck survivors can “assume a boat” — thus as Mougayar has touched on: blockchains and consensus ledgers may find traction outside of niches only if they satiate mass consumer appeal, not just hobbyist interest.

To the chagrin of the heavily invested, Bitcoin may prove to be the vehicle that will spawn a variety of useful mainstream tech but that will never actually go mainstream itself. In that respect, perhaps Bitcoinland is essentially a huge R&D program. Perhaps this is a modern facsimile of The Rise of ‘Worse Is Better.’ Bitcoin enthusiasts believe that they are the “New Jersey” crowd in this particular story but in truth they may be taking the “MIT” approach, where they are seeking to build a perfect new financial platform. The lesson of the story is that the MIT approach almost always fails because it is incredibly hard to do and relies on perfect up-front understanding, while the New Jersey approach favors incremental discovery and evolving things towards something that works well enough.

Or maybe, conversely, some black swan event such as a large hedge fund publicly announces major buys or an ETF is approved or large-scale regulatory clarity occurs (see also: the Bitcoin Bingo card); we can only know in retrospect.

In the meantime, other mental models are being discussed including a separation of specialized distributed ledger systems (via consensus-as-a-service) from the current crop of cryptocurrency systems as well as proposed a dual-currency solution (such as Seigniorage Shares) that could end up implemented in other projects such as Augur’s prediction market: it could also be used for CFDs, it does no one any good if the underlying currency is too volatile to price contracts in — even if you “win” you could still lose due to currency depreciation (this is not an endorsement).

Other ideas such as the new replace-by-fee patch targeted at providing a mechanism for miners to prioritize transactions or metacoin censoring tools to allow mining pools to filter out watermarked coins (colored coins, Counterparty, etc.), will undoubtedly provide empirical feedback to future ledger designers on what to do and not to do.

Welcome to Bitcoinland, a virtual world whose artificial age is more akin to Sumter County than Madison County and whose primary export is currency conversion via exergetic displacement. On-chain population: roughly 380,000.

Share the post "The myth of a cheaper Bitcoin network: a note about transaction processing, currency conversion and Bitcoinland"

Send to Kindle

Send to Kindle

I usually use the military as an analogy for describing the (in)efficiency of the Bitcoin network. If technology improves to make cars 10x cheaper, then great, transportation costs go way down and we’re all happy. But if someone makes a new design for a gun that is 10x better, then everyone gets 10x more firepower, cancelling each other out, and we are right back where we started.

How does this analogy relate to the blockchain?

There is a fallacy here based on over-simplistic modelling. If there are only 2 opponents in a closed system, then yes, both sides engaging in an arms-race is a lose-lose. But in the real world, the enemies are various and more importantly, unknown in advance. In that situation, an arms-race can be a win-win, since it creates a more stable equilibrium and a smaller chance of needing to use the weapons. The equilibrium will be less challenged by random fluctuations.

This is, I suppose, one of a set of possible arguments against superrrationality a la Hofstadter – without clearly defined opponents in a game, there is never going to be a strategy everyone can agree on. Reminds me a bit of Taleb’s “ludic fallacy” concept.

So we are *not* right back where we started if we have 10 times as much power doing the same work, whether we speak of tanks or ASICs. That is by far the most important job the Bitcoin network has to perform – to prevent attacks, or let’s say, sudden and dramatic changes in power.

This is why i think bitcoin will eventually need a constant inflation model in order to maintain a secure network. Say 1-4% inflation per year depending on growth rates etc.

http://www.reddit.com/r/Bitcoin/comments/2tb3r0/why_bitcoin_will_eventually_need_a_constant/

A couple of notes:

“Cost of maintaining of network” (with fiat) also includes the costs of the state (regulators, courts, police), banking policies other of regulation, cash registers, and many other transaction costs that occur during the conduct of any business. These costs are not needed with a cryptocurrency, and present an comparative advantage in particular in countries with poor contract enforcement.

“Circular flow of income” is emergergent behaviour that we observe at higher levels of liquidity. If that really ever happens with Bitcoin, that basically means that fiat money has already collapsed or is about to collapse. In other words, “circular flow” is the consequence, rather than a prerequisite, for monetisation. Hoarding, not spending, is what gives money its moneyness. If not all users hoard a good, it means that it has lower liquidity than money. If everyone hoards it, it means it’s money, and then you’ll also observe a circular flow.

You focus on the empirical, and neglect the theory.