[Note: opinions expressed below are solely my own and do not represent the views of my employer or any company I advise. Today is the 7th anniversary of the Genesis block.]

With over $900 million invested in cryptocurrency startups over the past couple of years, what does adoption and usage numbers look like?

Unfortunately very few of the companies that have received funding have publicly divulged actual numbers, primarily because consumer uptake has been lower than expected (or promised).

For instance, Coinbase recently published five charts it says reflect growth.

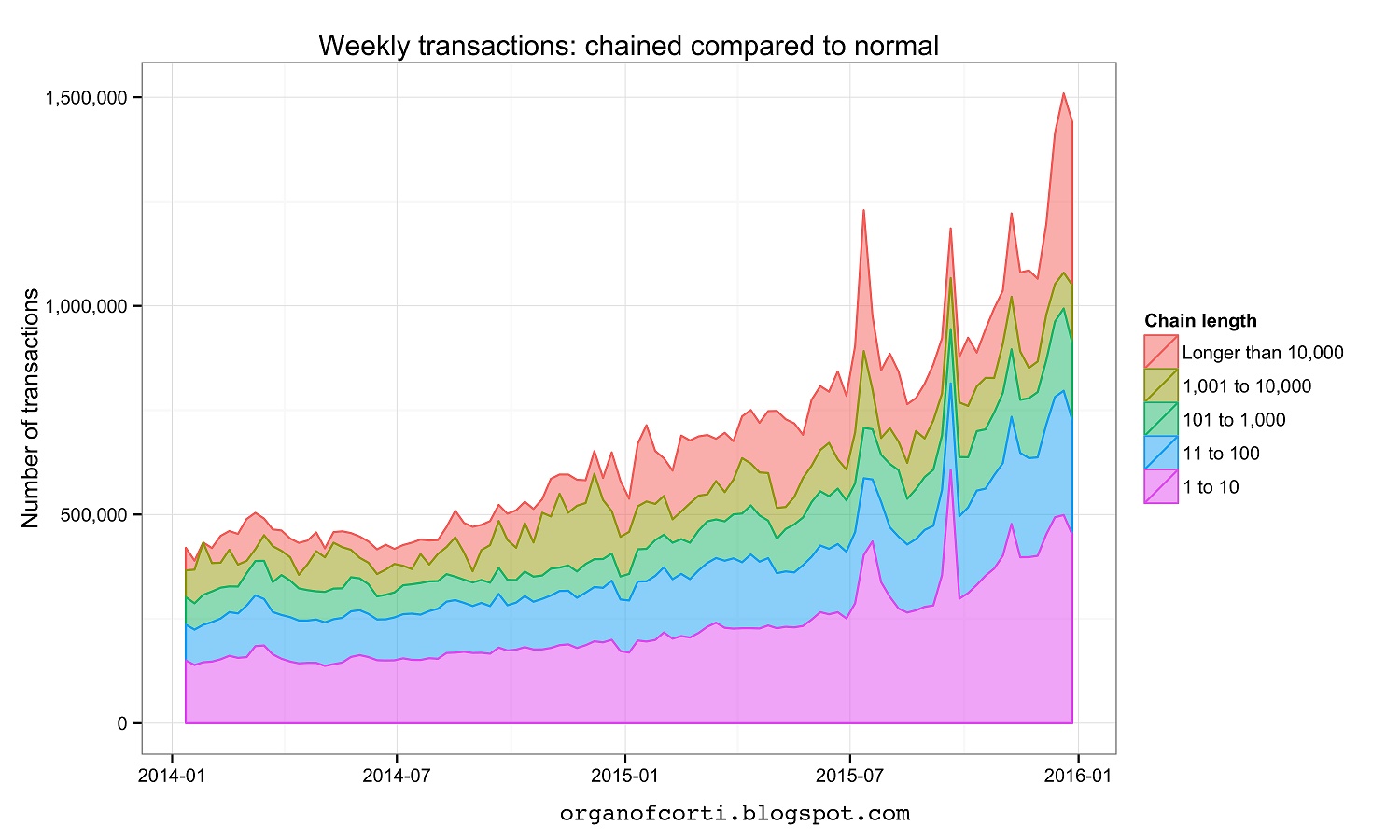

The first chart they show is transactions per day.

However, since we know that most transactions are “long-chain” transactions (comprised of spam, wallet shuffling, coin mixing, mining payouts, faucets, etc.), this is a poor indicator of actual on-chain trade and commerce or adoption.

As illustrated in the chart above, once long-chains are removed, growth (as highlighted in the pink region) is roughly linear since 2014, at ~0.5x per year.

As illustrated in the chart above, once long-chains are removed, growth (as highlighted in the pink region) is roughly linear since 2014, at ~0.5x per year.

What about Coinbase itself?

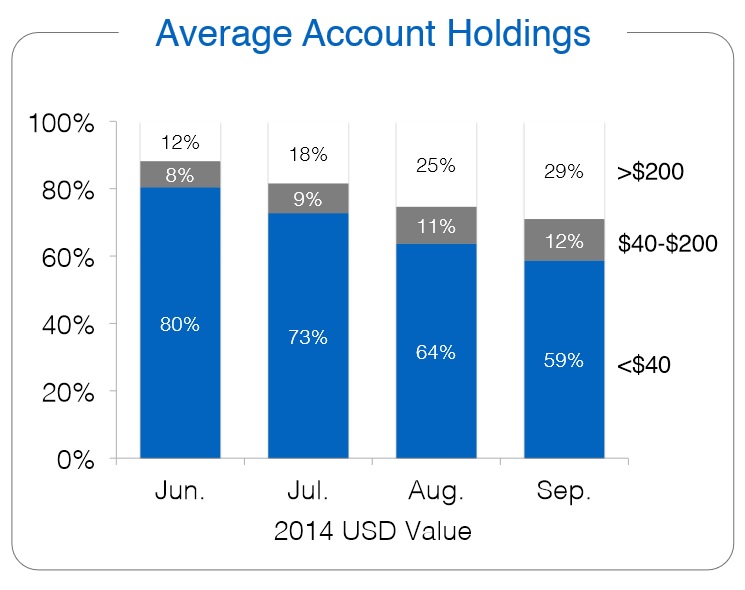

Coinbase doesn’t typically divulge much about specifics, however it’s older pitch deck (from September 2014) does give a few details about its users, such as 40% of all Coinbase users are from three states: California, New York and Texas; as well as the amount of deposits that Coinbase holds for each customer.

Slide 14, Coinbase pitch deck

While this number likely has changed in the past 15 months, ignoring the fluctuation in token prices it may be the case that the average deposit per customer has not increased significantly. Why might that be?

Source: Coinbase charts

Above is a 1-year chart produced by Coinbase showing the daily amount of off-chain transactions. Or rather, transactions that take place on their own internal system. As we can see, the volume is roughly the same across all of 2015. If usage actually was increasing or user numbers were growing substantially, then we should be able to see some visible changes upward. This has not occurred.

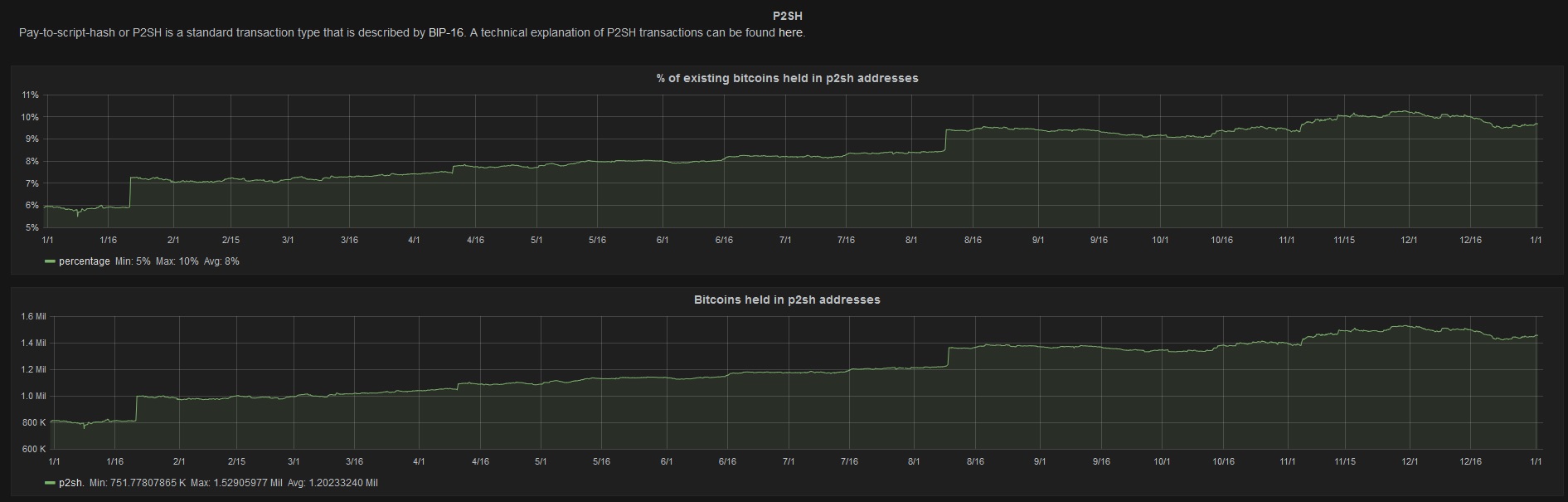

P2SH

Source: P2SH.info

P2SH, or pay to script hash, is probably the most common method for securing bitcoins (or UTXOs) via multisig. As shown in the two charts above, over the course of 2015 the percentage of existing bitcoins held in P2SH addresses increased from 6% to around 10% today. Though over the past 5 months the amount has effectively plateaued.

According to marketing material, BitGo processes more than 50% of all P2SH transactions (more than all other service providers combined). So this may also be an upward bound indicator of people who are savvy enough to secure their bitcoins via multisig (note: many custodial wallets such as Coinbase and Xapo purportedly secure certain layers of “cold wallets” via multisig and P2SH is just one method of doing so).

Multisig and Top Rich List

Source: Bitcoin Richlist

The chart above visualizes the percent of bitcoins owned by each address balance range.

As of block height 390,000 approximately 98.16% of all bitcoins reside on 513,648 addresses. This is not to say there are only half a million bitcoin users on the planet, as some of the addresses are owned or controlled by multiple people (such as a custodial wallet or exchange). But it is probably a pretty good proxy of on-chain users — users who actually control the private key and do not use an intermediary.

This is roughly twice as many on-chain users as twenty-one months ago (in April 2014) — at block height 295,000 — when I first started looking at this source.1

One interesting trend that ties in with the multisig window above is that at one point as recently as April 2014, none of the Top 500 addresses were using multisig. But over the past year, as seen by the “3” prefix at the start of addresses, we can visibly see several dozen Top 500 addresses that now use multisig (note: some of the other addresses may use hardware wallets such as Trezor, Ledger or Case and not use multisig).

ATMs

Source: CoinATMRadar

I once heard a Bitcoin reporter tell me in the August 2014 that BitAccess was on track to be the first billion dollar Bitcoin company. Whoops!

As we know empirically, the ATM industry in general is very low margin; companies make it up on volume which none of these startups have been able to thus far. Despite the hype, over the past a grand total of 536 Bitcoin ATMs have been installed, roughly 275 per year.

For comparison, according to the ATM Association there are roughly 3 million ATMs globally.

Can’t this change in the future? Perhaps, but recall that the average two-way (roundtrip) Bitcoin ATM fee is ~11% and there are only a handful located in emerging markets. Why is the fee relatively high? Because ATM owners are not operating charities and want to turn a profit. If Bitcoin adoption truly was going gang busters you would expect this number to be growing exponentially and not linearly.

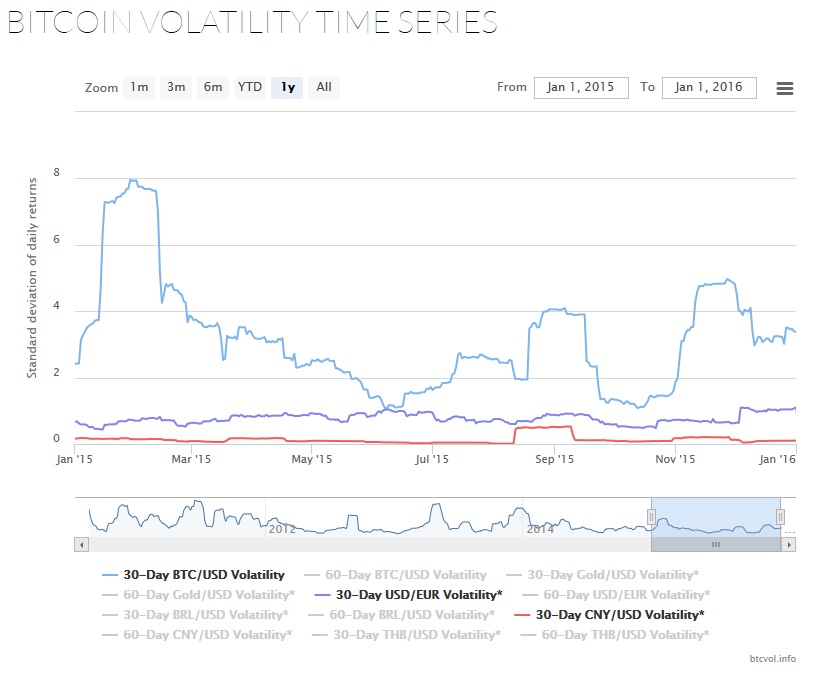

Bitcoin volatility

Admittedly this chart doesn’t have to deal with adoption. There is no scientific correlation between the amount of usage or users of cryptocurrencies and the volatility of its trading pairs.

Admittedly this chart doesn’t have to deal with adoption. There is no scientific correlation between the amount of usage or users of cryptocurrencies and the volatility of its trading pairs.

The reason I have included this is because in the Coinbase post above they state that bitcoin volatility is decreasing… relative to the Russian ruble and Brazilian real. Yet from the volatility chart above, it is clear that volatility has not really decreased. The BTC/USD volatility may be less than what it was in 2012, but on any given day it is still 10x more volatile than CNY/USD and 6x more volatile than USD/EUR — trading pairs that represent the real lionshare of global economic activity.

VC Funding

Source: btcuestion / Coindesk

The chart above was created by user “btcuestion” and is based on data in the Coindesk venture investment spreadsheet. It is a month by month bar chart over the course of the past two years.

What it shows is that VC investment in cryptocurrency-related startups peaked in Q1 2015. Yet, the bulk of the Q1 investments came from the 21inc announcement which itself was an aggregation of its previous rounds that had taken place over the previous 18 months. So funding may have actually peaked in Q4 2014.2

What this probably illustrates is that aside from a couple of permabull investors (such as Boost and Pantera), most serious venture capital has decided to wait and see how the dust settles before investing anything in this space. Why? Basically there has been no product market fit and few viable business models.3 Sure there has been a lot of publicity, but as Kevin Collier recently explored, there does not appear to be any permanent impact of say: Bitpay sponsoring a college bowl game last year.4

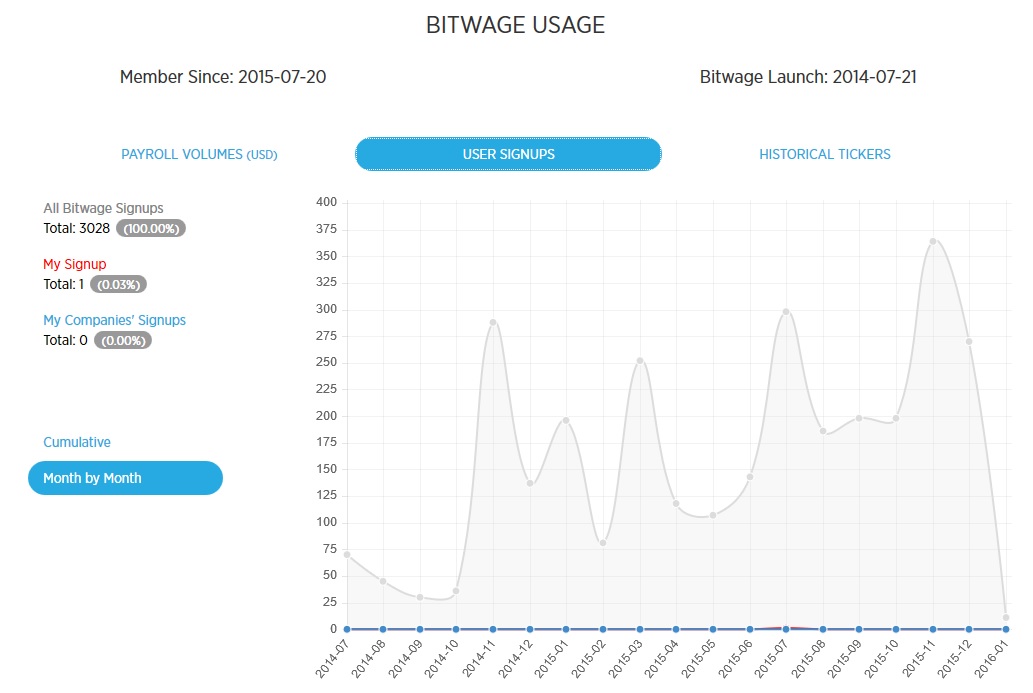

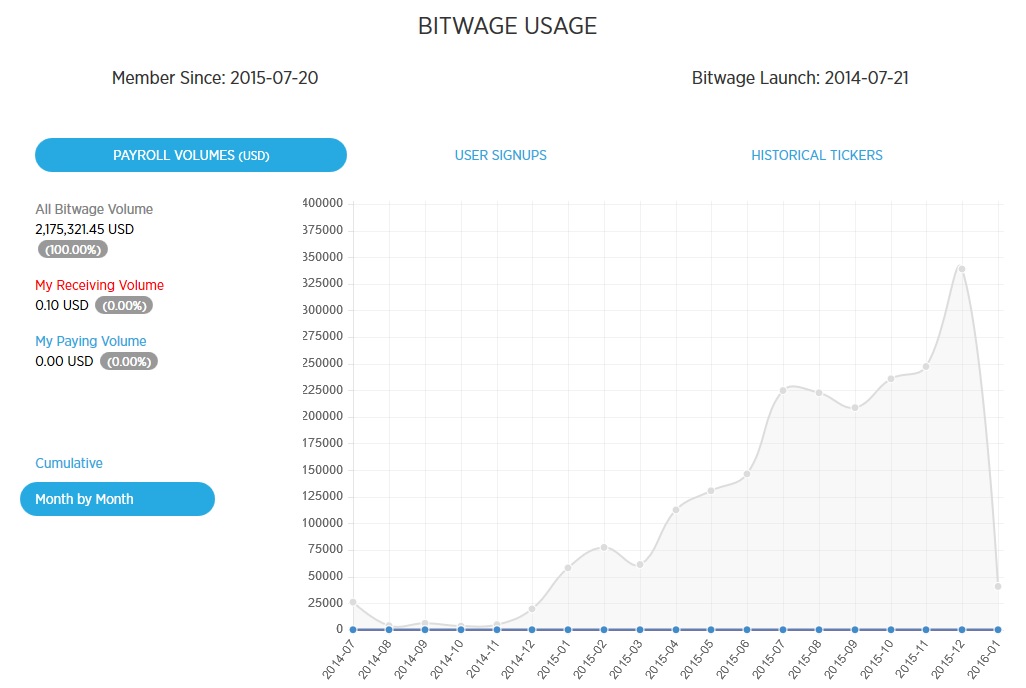

Bitwage activity

Source: Bitwage

Source: Bitwage

The two charts above both come from Bitwage, a startup that converts payrolls into bitcoins. Ignoring the drop-off in January 2016 (it is the beginning of a new month), for most of 2015 there were roughly 200-300 new user signups each month and about $250,000 in salaries converted as well.

Again, this is not to say that Bitwage’s service is not useful, rather that if there was increased bitcoin growth and adoption, then one proxy could be through payroll conversion. However, as shown above, growth is linear not exponential.

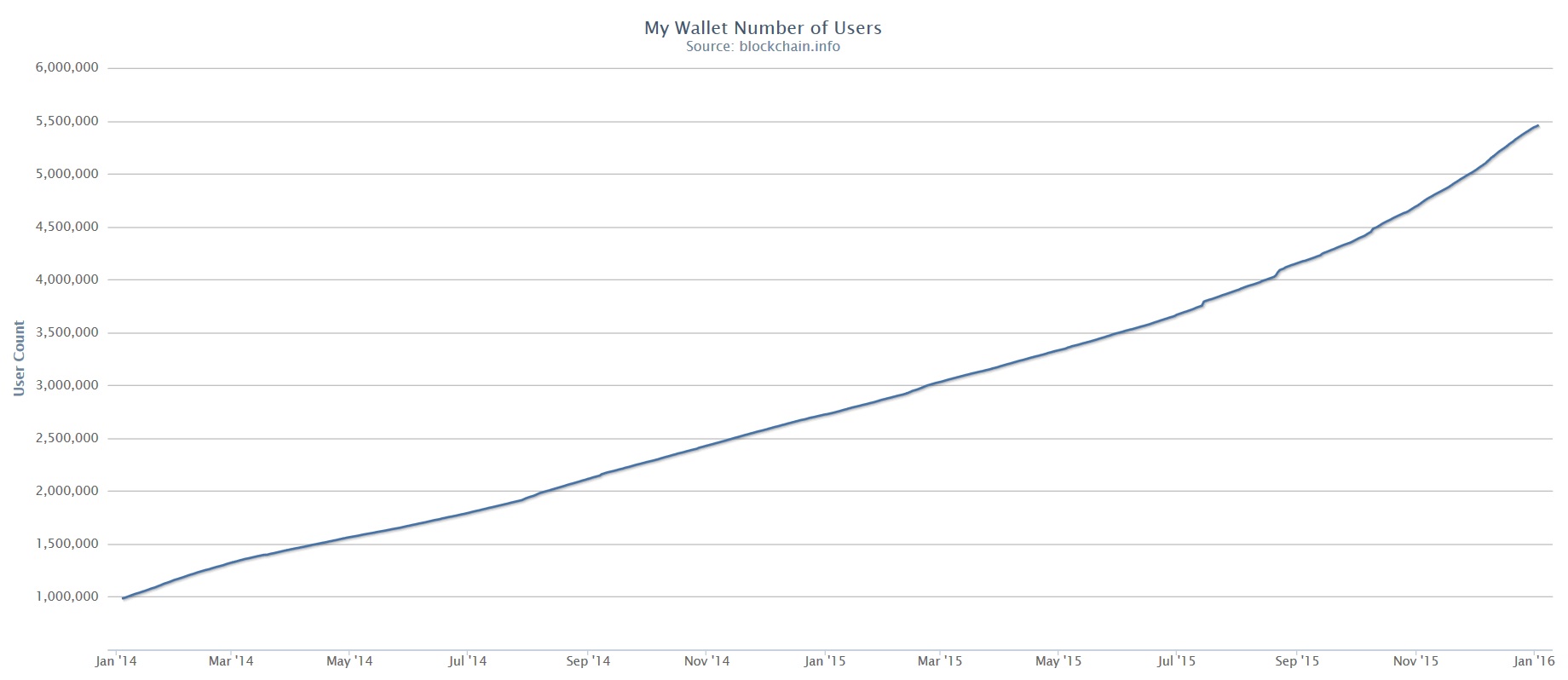

Blockchain.info wallets

Source: Blockchain.info

Above is a 2-year, nearly linear line chart from Blockchain.info depicting the “My Wallet” Number of Users. It bears mentioning that many people still use Blockchain.info wallets like a “temporary” wallet (or burner wallet) for coin mixing, yet despite the rapid creation rate for this purpose even if we look just at the last 6 months, it is not close to being exponential.

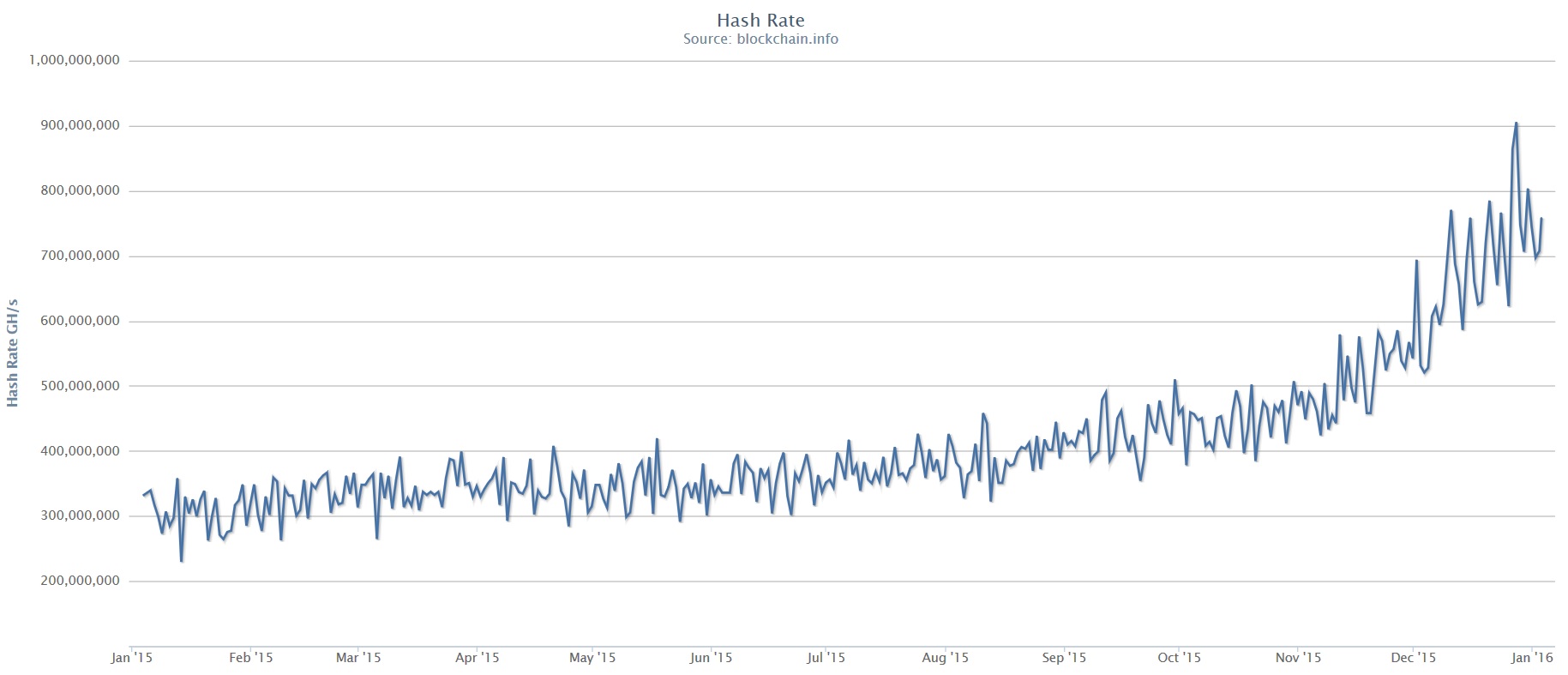

Hash rate

Source: Blockchain.info

But what about hash rate? It has continually gone up and to the right the last few months, surely this is an indicator of mass adoption?

All hash rate is measuring is the amount of work being generated by an unknown amount of computers (typically ASICs) somewhere on the planet. Hash rate typically rises when the price of bitcoins rise and falls when the price of bitcoins fall (see Appendix B). Since prices have nearly doubled over the past four months then it stands to reason that hash rate would correspondingly increase as hashing farms deploy new capital.5

Unless each site is inspected, it’s difficult to tell if there are more hashing farms and equipment and therefore “more users.” However, what we do know is that there are roughly the same amount of pools today (~20) as there were three years ago.6

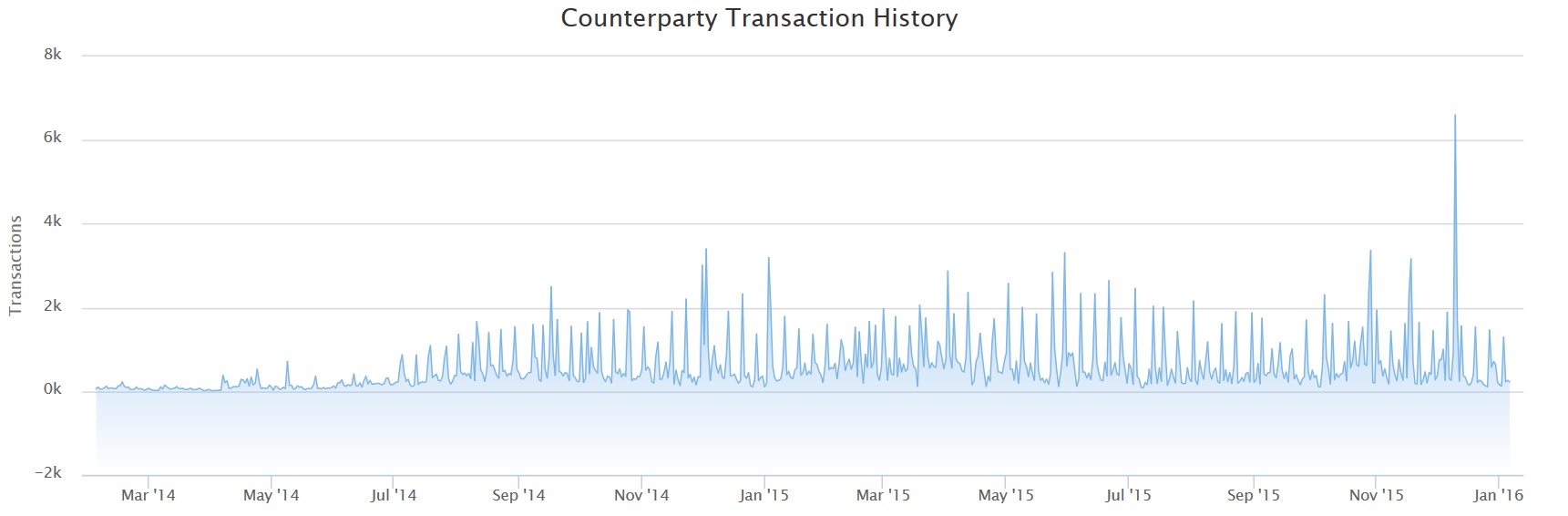

Counterparty

Source: Blockscan

Counterparty is an embedded consensus system (see section 1): an asset issuance platform that effectively staples itself onto the Bitcoin blockchain.

As shown above, on a given day roughly 500-1000 transactions take place through the platform. According to Laurent MT, the spikes may be related to the weekly distribution of LTBCoins. And again, despite turnkey services and vending machines such as Tokenly and CoinDaddy (and CounterpartyChain), overall growth on the ECS has effectively plateaued over the past year.

Conclusion

Bitcoin is a solution and service provider for those who hold bitcoins. Despite the fanfare, the conferences and the perpetual feel-good op-eds in Techcrunch, the only people who seem to use it regularly seven years later are a niche demographic group: young, white, tech-savvy men in North America and Western Europe. Many of whom have access to multiple other payment networks and asset classes for investment.

As a result, it is probably not a surprise that instead of using bitcoins to pay for coffee on-chain each day, most private key owners prefer to “hodl” or use intermediaries. This may make sense for those with low time preferences, but it shouldn’t then come as a surprise that there are few, if any metrics that show wide-scale adoption beyond this core demographic. Will this change in 2016 or will the “great pivot” continue?

- Spam and dust (such as “tips”) likely represents the remaining 1.84% of all bitcoins (located on 99% of all addresses). [↩]

- Funding has instead switched over to the fledgling non-cryptocurrency distributed ledger industry. [↩]

- Anecdotally, it appears that Coins.ph, BitX and Align Commerce have each gained actual traction in their respective regions. [↩]

- Stephen Pair provided a new chart for Forbes which purportedly shows a large uptick in transactions processed. This “surge” occurred during the same month as Bitcoin Black Friday and should be looked at again in the following months to see if it was a one-off event. [↩]

- There are also stories of new chips supposedly being deployed. In practice hashing farms do the Red Queen race: replace a machine… with another machine that uses the same amount of energy. [↩]

- The claim that 21inc or other mining chip manufacturers will “redecentralize mining” is a misnomer. Mining and hashing are not the same thing. Unless a hashing operator also runs a fully validating node, then they are part of the outsourcing process. More people may be hashing as part of the 21inc botnet, but not mining (mining is defined as selecting transactions to include in blocks; hashers do not do this activity, pools do). [↩]

No question, user adoption is disappointing. But user adoption of Linux / Unix was disappointing as well … until there was OSX, iOS, Android, Cloud Services.

For bitcoin (NXT, Monero, …) NIRP (negative interest rate policy), further financial repression and the next financial crisis will help with adoption.

And Bitcoin Maximalists are not the only ones that are concerned:

Bank for International Settlements:

An experiment is under way in continental Europe to test the “boundaries of the unthinkable” in monetary policy.

http://www.bis.org/speeches/sp150424.pdf

Currency is probably the most powerful application of the blockchain but will take the longest to have real utility. This is because ordinary people are required to pay their taxes in Fiat and exchanging Fiat for crypto-currency is still far from being a trustless and frictionless process. Therefore bitcoin, ether, etc will, for the medium term, have little utility as currencies for ordinary people. They will however, have real utility to financial institutions that wish to serve these people as they massively reduce their overheads and capital requirements. They will also naturally be essential to the thousands of projects in the pipeline that will require the blockchain for its timestamping or smart contracting abilities. Crypto-currencies are therefore largely not distinct from the crypto-ledger industry. They are the fuel that will power it. This great pivot you speak of is not so much a pivot but rather an expansion into a plethora of areas that will eventually indirectly unleash the ‘currency’ app to the masses.

I’m going to check my Dogecoin prices in 2020…

Pingback: Relax, The Slowdown In Bitcoin Investment Isn't As Bad As It Looks | Mattermark