Back in May I published a blockchain analysis piece on Coindesk that utilized graphs created by John Ratcliff. Ratcliff published several new charts yesterday that provide a fuller picture of this overall movement.

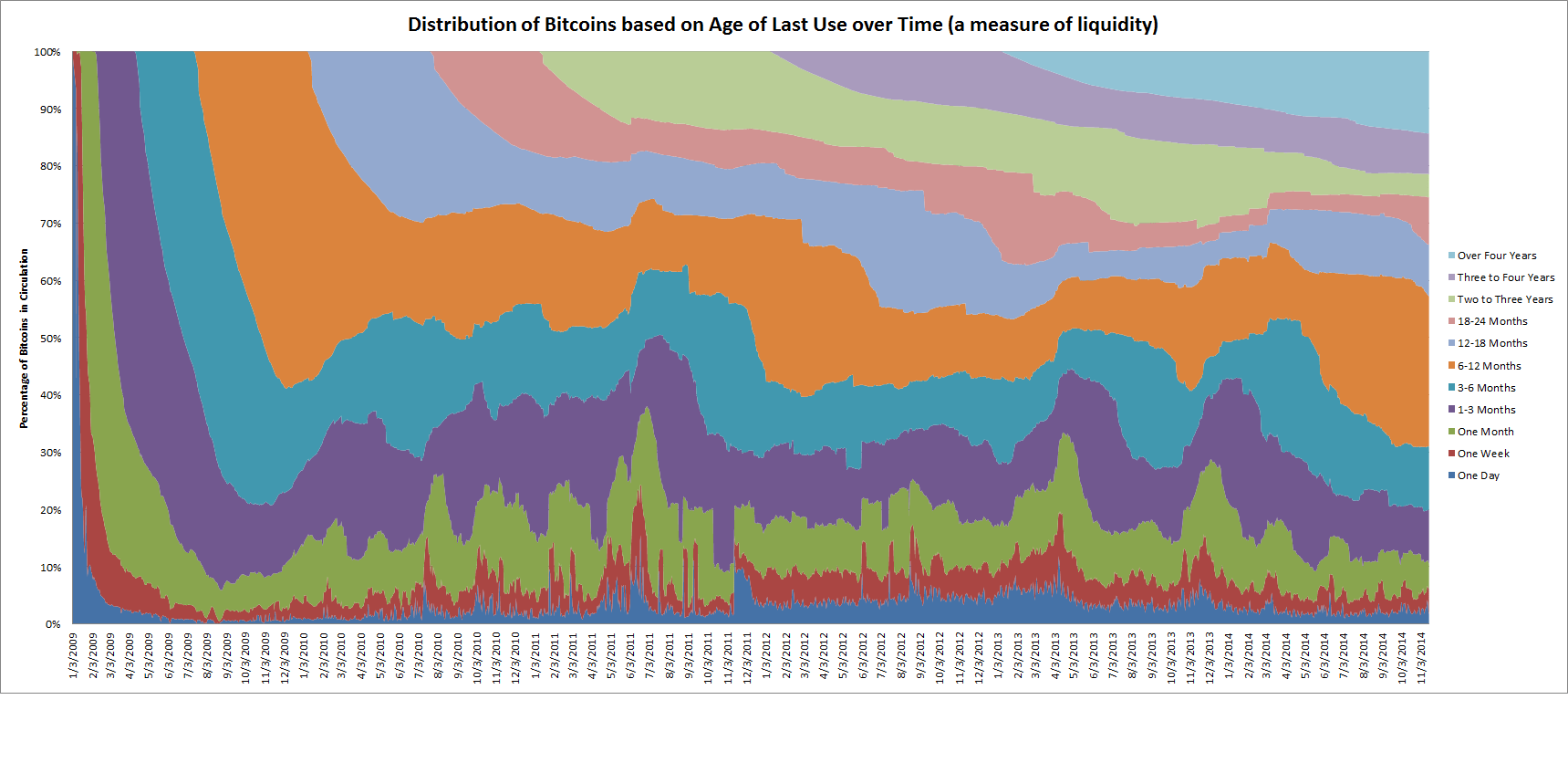

The chart above visualizes nearly 6 years of token movements.

Is there a way to isolate the past year and if so, what does the past year look like? That’s what the next chart illustrates:

What conclusions can be drawn from these charts?

1) that token movement (velocity) strongly correlates with a rapid increase in market prices (e.g., more velocity during the bull runs, less during price decreases); you can see that in the first chart with large bumps in April 2013 and then again in November 2013

2) because of the large dip in prices over the past year, most tokens are inactive in part because the owners are still “underwater”

3) that monthly liquidity is still only around 10% (more on consumption below)

4) the “tx volume” chart on Blockchain.info is no longer entirely valid due to a combination of the usual mixing and mining rewards but also because of increased advertisement spam (e.g., metadata within OP_RETURN), increase in P2SH and Counterparty tx’s. Only a full traffic analysis can provide a more accurate breakdown.

What is especially interesting is to see the “overhang” or rather the “underwater” coins that are moving from the 3 months to the 6-12 month band. What this effectively shows is that owners of those UTXOs purchased them during the bubble of November-December 2013 and are still willing to wait and hold onto these coins until the price rebounds. If there is no upward change in prices then some (or all) of these coins will eventually move into the next band sometime in the spring of 2015.

What other conclusions can be made?

This is a sobering chart for advocates or entrepreneurs within the merchant payment processing vertical. What this shows is that despite the near quadrupling of merchants that now accept bitcoin as payments (this past year increased from ~20k in January to ~76k through September), on-chain activity has not seen a corresponding increase by consumers. They are all effectively fighting for the same thin slice of liquid coins, a segment which empirically has not grown. This does not mean that there are no consumers, only that when paired with data from Bitcoin Day’s Destroyed, there probably hasn’t been any real on-chain growth beyond the exceptions in #4 above. Thus on any given day, payment processors (collectively) likely only process 5,000-6,000 bitcoins still. Other additional activity could be taking place off-chain in trusted third parties (like hosted wallets and exchanges such as Coinbase).

Too reuse an analogy from Chapter 14 (p. 224 and 230), that also means that since 3,600 bitcoins are created each day to pay for security, that with this ratio (3,600 : 6,000) every other mall patron is effectively being guarded by a mall cop which in laymens terms means there is massive security overkill still taking place. This is not a big deal today but when coupled with analysis from Dave Hudson, network transaction fees will have to increase by several orders of magnitude to replace the seigniorage that currently incentivizes miners. This is best illustrated in the cost per transaction metric on Blockchain.info.

As I mentioned on a panel on Tuesday this collective “hodling” (hoarding) behavior is understandable given the future expectations of price appreciation. Yet it is probably not a good characteristic for a modern “currency,” for reasons discussed in Chapter 9 and also Why Market Prices Do Not Double With a Block Reward Halving.

Isn’t it true that more.than 70% of all gold or even USD reserves in the world did not move during the same timeframe.

I look at the amount of value being transmitted on the network and think it is remarkable.

Bitcoin is both a currency and a store of value, so what is unusual about the store be that high? I find it remarkable how much of the market is liquid.

Hi John. So what happens with fiat is that almost all of it is essentially deposited (saved) in banks who then relend it out creating circulation. There is nothing within the current Bitcoin protocol that enables this type of “savings” or “lending” to happen with Bitcoin. Perhaps it will change (as shown by the services being built outside the network). But, bitcoin holders are not savers in the modern sense because the token sits entirely idle, divorced from any financial flow. That is not necessarily a bad thing, but I think the advocates at conferences are not technically advertising the protocol correctly the way economists or financial analysts do, the protocol does not offer any service a bank does beyond a lock-box at this time.

Plus it is unclear what value is actually being transmitted if any, it is impossible to know what each transaction represents. For all we know, it is largely dominated by mixing and mining (probably not). In the future perhaps other researchers will conduct traffic analysis along the lines of what Sarah Meiklejohn and her colleagues did: http://cseweb.ucsd.edu/~smeiklejohn/files/imc13.pdf

Whether the analysis Tim points out is a problem or not, really depends on the market Bitcoin is trying to target. Bitcoin is simultaneously targeting 3 markets:

1. As a form of “Gold 2.0” i.e. a value storage market. In this market, one would expect low movement and mentioned numbers are not problematic at all.

However, bitcoin the currency is noncompetitive as Gold 2.0 simply because the network needs much higher transaction volume to survive. Low volume coupled with declining block rewards will bludgeon bitcoin in a few years.

2. As a currency for low friction global transactions: This aim is much more compatible with bitcoin the network. Ideally, volume grows and balances out declining block rewards.

That the volume is not growing, and most bitcoins do not move is worrying. It is a bad sign because it indicates bitcoin is failing to take off as a transaction medium.

3. As a platform for other services like Counterparty: In this market, bitcoin purely serves as a foundation for other activities like decentralized dollar to apple shares trading.

The problem here is that one can build much better – cheaper, faster and more scalable – technology to do the same. Hyperledger project is the perfect example. Bitcoin will be out-competed in this ‘platform’ market.

So John, what market is bitcoin exactly targeting? And how do these numbers fit that market to make a coherent story?

Gold is MANY things in today’s world, but almost nowhere is it actually “money” in the sense of mediating ordinary transactions.

Any chance you could send me the raw data for this?

The raw data is public. It’s all in the bitcoin blockchain.

Transaction fees do not need to increase by a few orders of magnitude – transaction fee *revenue* needs to increase by a few orders of magnitude.

This can be accomplished if fees per transaction remains the same and the number of transactions increases by a few orders of magnitude.

Hi Justus, that scenario is not quite true. We know that in theory (as discussed in section 6 of the original white paper) an enormous — permanent — increase in tx volume coupled by some type of fee, could conceivably replace it. But empirically in practice, as more transactions occur off-chain, miners are not being rewarded for their services and continue to rely almost entirely (~99.7% as of this writing) on seigniorage. Could this change? Sure, but it would require a change in consume behavior away from free and towards either higher fees and/or more volume which simply may never germinate.

I explore this further in this post last month: http://blog.melotic.com/2014/10/07/the-collective-action-problem-of-mining-fees/

Dave Hudson also has some very good articles on this the past month as well: http://www.hashingit.com

Or course I mean higher transaction volume on-chain.

Right now it’s impossible for on-chain transaction volume to grow to high enough levels to replace seigniorage because the protocol contains a built-in production quota.

This is precisely why the production quote needs to be removed, in order to allow transaction volume to grow on chain to levels that support mining via transaction fee revenue.

The high-fee, low volume won’t work for Bitcoin precisely because the high fees are an artifact of a production quota. Anyone could start a competing cryptocurrency with no production quota and order-of-magnitude lower fees and overcome Bitcoin’s network effect.

The question is how will the low-fee high volume work when off-chain is / will prove to be more convenient?

Any on-chain fee will be out-competed by speed, lower fees and convenience of off-chain transactions. Why exactly are we sure on – chain transactions will rise 10000 fold that it needs to? How exactly does Bitcoin solve this collective action problem?

Hi, to bring home the point, miners are actually receiving less in revenue from fees than they were two years ago, this is very unsustainable: https://blockchain.info/charts/transaction-fees?timespan=2year&showDataPoints=false&daysAverageString=1&show_header=true&scale=0&address=

I think you would find these dual-currency protocol proposals of interest as they do discuss the seigniorage/rebasement issue in a trustless manner (in theory):

– “Hayek Money: The Cryptocurrency Price Stability Solution” by Ferdinand Ametrano

– “Investor/Saver Wallets and the Role of Financial Intermediaries in a Digital Currency” by Massimo Morini

– “A Note on Cryptocurrency Stabilisation: Seigniorage Shares” by Robert Sams

– Dominic Williams papers and documentation on Pebble

With respect to block sizes, if you do increase the block size to infinity (or some other arbitrarily large number above 1 MB), it doesn’t really change the fact that there is a scarce good that miners need to still ration. Gavin’s analysis is likely incorrect, I would stick with the work Dave Hudson and Jonathan Levin have begun looking at (here’s Jonathan’s thesis)

Neophyte stock investors often sell their winners (and incur capital gains tax, often at higher-rate short term rates) and hold on to their losers (tying up their money in dud stocks and forgoing tax losses). “Psychology” rather than “rationality” is usually cited.

Experienced investors—with either longer time horizons or after the hot-heads have been Darwined out of the market—may do it a bit less, and institutional investors supposedly invest with more modeling of the stocks’ underlying worth, (also) supposedly show even less of this financially-foolish behavior.

The fact that bitcoin transactions rise after the price has been rising suggests that the same n00b psych is at play here. The clear imputation is that no more than 30% of bitcoin is being used to facilitate transactions, while 70% is used speculatively or as a long-term investment.

Others here seem to suggest that BTC needs a rising price for mining, and hence, fast transactions, to be economical. This raises the concern of an excess supply of mining equipment, but a shortage of transactions that need it. Sure wish I could see how that ends well.

I’ve never bought Bitcoin for under 300 and yet I’m holding 60 bitcoins that cost me under 200 eachthe volatility of Bitcoin has been an easy living for me I don’t know what to make of the future of Bitcoin but it sure has been a fun ride

Pingback: Altcoin Today | Analysis: Around 70% of Bitcoins Dormant For At Least Six Months

Pingback: Bitcoin News for the week of 11/24/14 | Blockchain Blog

Pingback: Altcoin Today | Too Many Bitcoins: Making Sense of Exaggerated Inventory Claims

Pingback: Altcoin Today | 70% of Bitcoins Have Been Hoarded for Six Months or More

Pingback: Bitcoin Price Roundup: November 26, 2014

it would be great to see an updated version of the chart, given the recent mega sell off…

Can you do this analysis again?

Many would love to see the intriguing analysis you’ve provided